Today’s Real Estate Market Explained Through 4 Key Trends

Today’s Real Estate Market Explained Through 4 Key Trends

As we move into the second half of the year, one thing is clear: the current real estate market is one for the record books. The exact mix of conditions we have today creates opportunities for both buyers and sellers. Here’s a look at four key components that are shaping this unprecedented market.

A Shortage of Homes for Sale

Earlier this year, the number of homes available for sale fell to an all-time low. In recent months, however, inventory levels are starting to trend up. The latest Monthly Housing Market Trends Report from realtor.com says:

“In June, newly listed homes grew by 5.5% on a year-over-year basis, and by 10.9% on a month-over-month basis. Typically, fewer newly listed homes appear on the market in the month of June compared to May. This year, growth in new listings is continuing later into the summer season, a welcome sign for a tight housing market.”

This is good news for buyers who crave more options. But even though we’re experiencing small gains in the number of available homes for sale, inventory remains a challenge in most states. That’s why it’s still a sellers’ market, giving homeowners immense leverage when they decide to make a move.

Buyer Competition and Bidding Wars

Today’s ongoing low supply, coupled with high demand, creates a market characterized by high buyer competition and bidding wars. Buyers are going above and beyond to make sure their offer stands out from the crowd by offering over the asking price, all cash, or waiving some contingencies. The number of offers on the average house for sale broke records this year – and that’s great news for sellers.

The latest Confidence Index from the National Association of Realtors (NAR) says the average home for sale receives five offers (see graph below):

Average Number of Offers

For buyers, the best way to put a compelling offer together is by working with a local real estate professional. That agent can act as your trusted advisor on what terms are best for you and what’s most appealing to the seller.

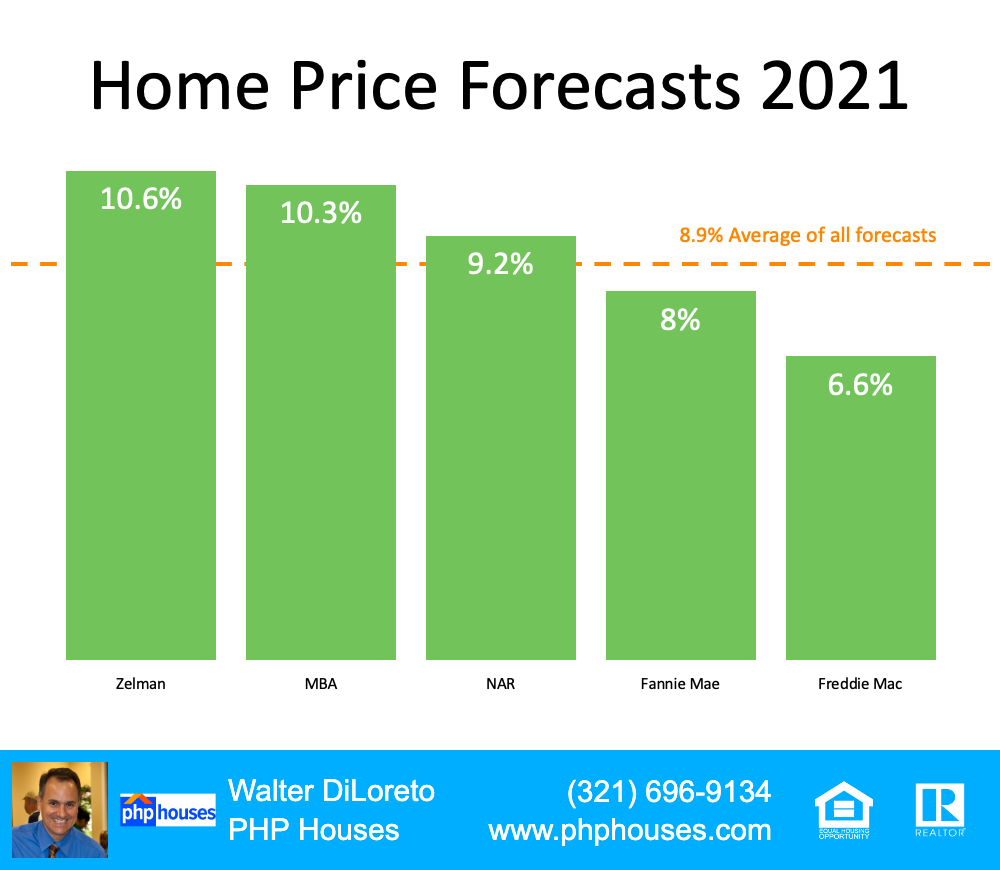

Home Price Appreciation

The competition among buyers is driving prices up. Over the past year, we’ve seen home price appreciation rise across the country. According to the most recent Home Price Index (HPI) from CoreLogic, national home prices increased 15.4% year-over-year in May:

“The May 2021 HPI gain was up from the May 2020 gain of 4.2% and was the highest year-over-year gain since November 2005. Low mortgage rates and low for-sale inventory drove the increase in home prices.”

Rising home values are a big part of why real estate remains one of the top sought-after investments for Americans. For potential sellers, it also means it’s a great time to list your house to maximize the return on your investment.

A Rise in Home Values and Equity

The equity in a home doesn’t just grow when a homeowner pays their mortgage – it also grows as the home’s value appreciates. Thanks to the jump in price appreciation, homeowners across the country are seeing record-breaking gains in home equity. CoreLogic recently reported:

“…homeowners with mortgages (which account for roughly 62% of all properties) have seen their equity increase by 19.6% year over year, representing a collective equity gain of over $1.9 trillion, and an average gain of $33,400 per borrower, since the first quarter of 2020.”

That’s a major perk for households to leverage. Homeowners can use that equity to accomplish major life goals or move into their dream homes.

Bottom Line

If you’re thinking about buying or selling, there’s no time like the present. Let’s connect to talk about how you can take advantage of the conditions we’re seeing today to meet your homeownership goals.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

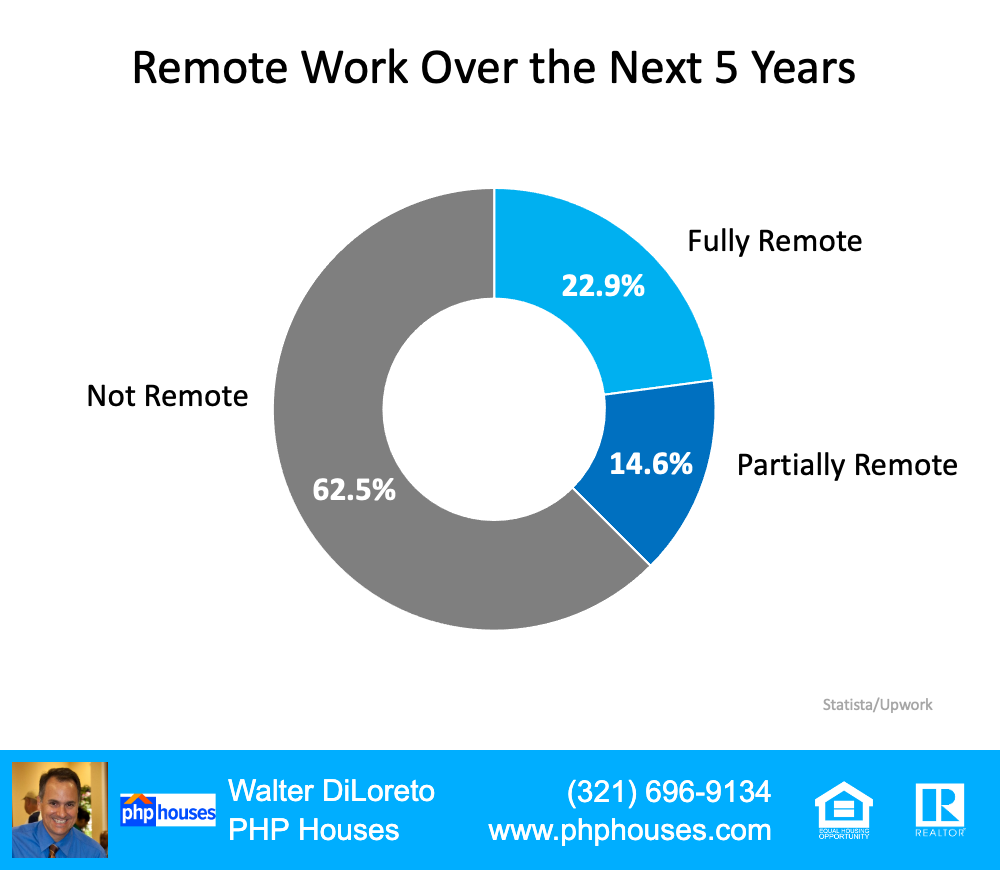

Over the past year, many homeowners realized what they need in a home is changing, especially with the rise in remote work. If you’re longing for a dedicated home office or a change in scenery, now may be the

Over the past year, many homeowners realized what they need in a home is changing, especially with the rise in remote work. If you’re longing for a dedicated home office or a change in scenery, now may be the