3 Reasons To Buy Before Spring

Comments (0)

The baby boomers are coming of age and many are finding themselves in situations where they are taking care of their elderly parents. It can be difficult to decide parents are in need of alternate or extra care. But after that decision is made, there are many others to be made. For instance, what is going to happen to their possessions if they go into a care facility or community living? You may wonder if you can sell parents house if you can offer it for sale by owner, or about many other options. You may ask, “can I sell my parents house to cash buyers?” Here are a few tips if you are planning to sell your elderly parents home.

When you put a house on the market it can seem like an eternity before it actually sells. Trying to sell your elderly parents home can take a long time too. Each situation has different factors that vary how long it takes to sign the final document to close the deal. On average, it takes about 110 days. That’s if everything goes smoothly and without any hitches. In some instances, it can take considerably less time depending on how complicated the paperwork is. If you are selling your parents house and using a traditional real estate agency, be prepared to wait.

Selling a house can be a difficult decision for senior citizens, especially if they have lived in the home for many years. Making the decision is one thing, but it can be the process that gets complicated. And if a child needs to sell parents house there can be numerous roadblocks, even if they have power of attorney. Typically, springtime is the best time to list a house with a real estate broker, but there’s no guarantee. Fortunately, there are several options available for children who need to sell parents house, or for the elderly who need to do so. The answer to the question of “when should seniors sell their homes?” is an individual one. But it is typically once they can no longer care for the home properly or take care of themselves alone.

Do you need help selling your elderly parents home? There are several ways to find help. First off, ask family for help. They can oftentimes help answer the question, “when should seniors sell their homes?” And sometimes they can help with the actual selling process. Some of this may depend on who has full power of attorney. Here are a few tips for selling your parents house.

Some people have the question, “can I sell my parents house to siblings?” Because every situation is unique and has different circumstances, this is a difficult question to answer. In some cases, it might be possible. However, if they could qualify for a mortgage, it might be possible. This could take months at best because of the paperwork and making sure everything is handled appropriately.

Having power of attorney is useful if you want to sell their house. However, you do need to check what type of POA you were granted. Read over the documents carefully to ensure it gives you the authority to sell their real property.

If you want to advertise your parents house as “for sale by owner” it’s best to have POA. If you are on the deed it can help too, or have your parent’s consent if you are selling it on their behalf. For sale by owner transactions can be very tricky and you need to know exactly what you are doing, especially when it comes to the paperwork. Is it possible? Yes, but it’s probably not best to advertise the house as for sale by owner.

If you are looking for the easiest, least stressful way to sell the property, a cash buyer is your best option. Look at all the options and you’ll realize they all take a long time and can be very complicated. If you’ve been asking the question, “should I sell my parents house to cash buyers?” then the answer is, yes. If you have the legal right to sell your parents house, selling to an investor is often the simplest and quickest answer. If you are saying, “I am ready to sell my parents house to cash buyers!” Then it is time. A cash buyer can have the paperwork done quickly and securely. The property will be sold, and you will have cash in your hands.

If you are ready you just need to contact an investor who buys houses for cash. Explain your situation. Just simply tell them you “want to sell my parents house to cash buyers.” And they will help you complete the paperwork. The first thing they will do is an informal inspection of the property, then they will make an offer. If you accept the cash offer, they will have the paperwork done in just a few days. You won’t have to worry anymore about your questions, “can I sell my parents house to cash buyers?”

Selling your parents house is stressful. Although there are lots of ways to do it, using power of attorney takes time and money. Don’t wait for the house to get sold. If you need your parents house sold ASAP then selling to a cash buyer is your best option.

Do you have a question about the house selling process? Do you want to get your no obligation cash offer for your parents house? Even if you don’t decide to sell, we’d love to answer any questions you might have. Give us a call today at 407-641-1531.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 641-1531

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

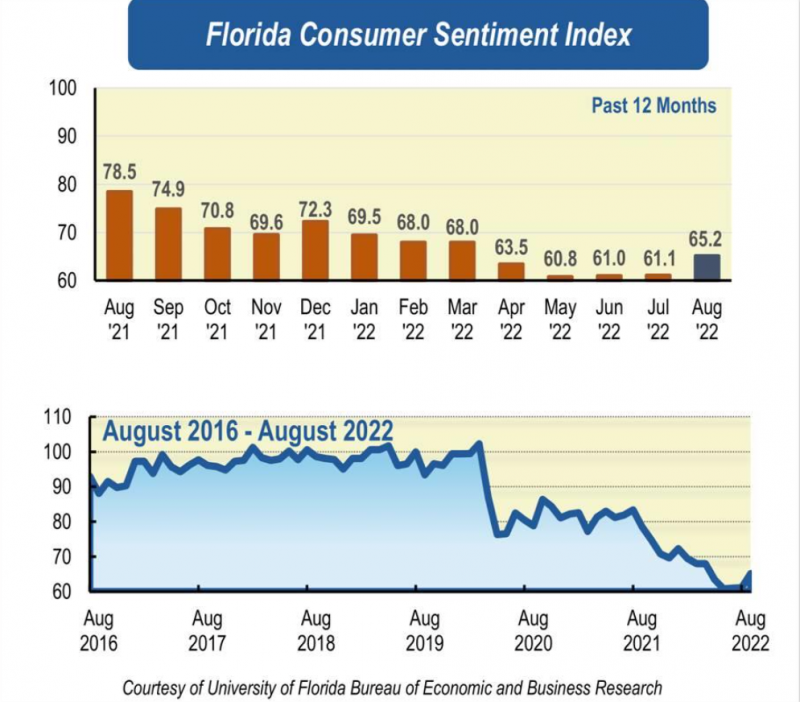

Florida Consumer Confidence Up for Second Month

By Kerry Smith.

The August index from UF rose 4.1 points to 65.2. All five components in the larger index moved higher, with a notable rise in future expectations.

Floridians’ consumer attitudes increased for a second month in a row. In August, the University of Florida’s consumer sentiment index rose to 65.2, up 4.1 points from a revised figure of 61.1 in July – and all five components that make up the total index increased.

Floridians’ perceptions of their personal financial situations now compared with a year ago increased 2.7 points from 52.5 to 55.2.

And attitudes about buying a major household item, such as an appliance, rose in tandem with that increase, also rose 2.7 points, from 52.5 to 55.2.

The boost in attitudes was almost universal among Floridians, though a bit less among lower-income (less than $50,000 per year) households.

Outlooks about expected economic conditions one year from now were also positive. Attitudes about personal finances increased 4 points from 75.1 to 79.1.

Expectations for U.S. economic conditions one year from now increased a notable 7.4 points from 58 to 65.4 – the highest increase in August. And attitudes about U.S. economic conditions over the next five years increased 3.8 points from 67.3 to 71.1.

“Most of the optimism stems from Floridian’s expectations about future economic outlooks, particularly from expectations about the national economy over the next year,” says Hector Sandoval, director of the Economic Analysis Program at UF’s Bureau of Economic and Business Research. “These opinions are consistent with the strong labor market, along with falling energy prices, such as gasoline, and the overall slowdown in the pace of inflation from a four-decade high.”

Sandoval says gas prices play an outsized role in attitudes because Floridians see them “every day while traveling to and from work, (and) gas prices in Florida have declined consistently since mid-June, not only improving Floridians’ perception of the economy but also releasing pressure from their budgets.”

The Florida labor market has continued to strengthen with more jobs being added statewide in July. Florida’s unemployment rate ticked down by 0.1 percentage point in July, reaching 2.7% and matching the rate observed in February 2020, right before the pandemic hit. Moreover, newly filed unemployment claims have hovered around pre- pandemic levels.

Sandoval isn’t sure if improving attitudes are a trend or not yet.

“Although consumer confidence has increased for two consecutive months, it’s difficult to interpret this as an overall change … especially since the Fed will keep rising interest rate until there is evidence that inflation pressures and the economy are cooling, thus possibly pushing the economy into a recession.”

UF consumer sentiment time chart

The index used by UF researchers is benchmarked to 1966, which means a value of 100 represents the same level of confidence for that year. The lowest index possible is a 2, the highest is 150.

By Kerry Smith

Source: © 2022 Florida Realtors®

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

You may be looking at selling your parents house. If so, you may need to rely on your power of attorney sell property option. If you are using this authority to do this you need to make sure it is correct. Meaning that the power of attorney sell property authority is legal. If you parents are mentally incapacitated the power of authority may need professional backing. It means that one or maybe two doctors are required to certify the incapacitation. You may want to have a lawyer help you with getting the power of attorney sell property authority. Once done in a legal manner then you can go about selling your parents house.

There will be some challenges. Even though you have the authority to sell your elderly parents home. They may not understand why you are doing this. If they are still living in the home you will need to prepare them. Too much upset for them will make them unsettled. By discussing with that the house needs selling in a positive way it will help. If they have something to look forward to it will be easier for them. When selling your parents house you want it to be as least disruptive as possible.

When you are selling your parents house you have some work ahead of you. You will need to get a house ready to sell by getting it so it will show in a positive way. How much work this will take will depend on the circumstances. If your parents have gathered a lot of things over the years you will need to declutter.

Then you will have to do a house inspection. Doing to will help you determine if there are repairs. There may be some things that need doing when selling your parents house. Prospective buyers may want a house inspection. You do not want to lose a sale because it didn’t pass inspection.

As you go through the sell parents house process it may be upsetting for your parents. You may have to go slower than you wanted to. Otherwise it will be overwhelming for them. The sell parents house task requires a lot of patience.

You may be asking yourself should seniors sell their home. After all this is your parents home. You may be feeling guilty about selling your parents house. As parents age taking care of a home can become too much for them. Small repairs left unattended to can turn into big problems. Plus be expensive to do. Many seniors are living on a fixed income. They no longer can handle the financial obligations that comes with home ownership. In these cases the answer to should seniors sell their home most likely is yes. Then there are some seniors whose health is failing. Being in their home may no longer be safe for them. When you are selling your parents house these are all things you need to consider.

You want to get as much money as possible from the sale of the house. It is one of the things to think about when get a house ready to sell. But you don’t want to be paying a lot of money for repairs either. When selling your parents house you may think about the for sale by owner option. Aside from saving money you may think it will be easier on your parents.

You will save on real estate fees with the sale by owner option. But you may end up still spending a lot of money to get a house ready to sell.

The sale by owner can be difficult on your parents and you. Potential buyers will want to see the house. It still means bringing strangers into your parents home. It could be stressful for them. Then you have the hassle of being there for the showings. Plus, you have all the advertising and marketing to take care of.

A for sale by owner can be a slow process. Most likely you want a quick sale.

When selling your parents house you want to do it as quick as possible. When selling in a traditional manner you have to depend on the realtor for this. If you go for sale by owner it can take even longer. There is a way for selling your parents house fast.

Everything that you are hoping to do with selling your parents house is possible. It is possible through a sell a house for cash opportunity. There are trustworthy and experienced investors that are willing to buy your parents house. They will do so in a fair manner.

These investors will give you the total amount of cash for the house that has been agreed upon. It means your parents will have the extra money they may need. Perhaps they need to pay to go into a retirement home. With the extra cash from the sale they will have more options.

The sell house for cash means you are not going to be upsetting your parents. They don’t have to put up with strangers coming through their home to see it. They are not going to be living in a home that is going through the packing process.

There is not going to be any of the hassles of repairs. The sell house for cash buyers will buy the house as is. It means that there will be no need for a house inspection. The sell house for cash is fast. Your parents can get settled into their new living quarters much faster. It will give them stability once again. For you the hassles of selling your parents house will come to an end. The sale is simple and quick.

You will save money from not having to pay realtor fees. Plus, you won’t have the expenses that come with selling the house by owner. The legal fees will be minimal as it is a straightforward sale. If you have the task of selling your parents home then the sell a house fast for cash is the ideal option for you.

At PHP Houses we specialize in a quick sale so that you can get on with the more important things in life. Don’t stress out about selling your parents’ house. In the event you need to sell your parents house before death, give us a call at 407-641-1531. We would love to answer any questions about the house selling process that you might have.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

Nobody likes to think about having to take on the role of caring for their parents. Instead of their parents caring for them. Parents do age and they often need the help of their children. Many times they are still house owners when this happens. Now it may mean you need to sell your elderly parents home. If so you may ask can I sell my parents house to siblings?

It may be that your parents have given you the responsibility for their decision making. Now you are responsible to sell your elderly parents home. You may have other siblings that want to keep the home. The question you now need answers to is can I sell my parents house to siblings? The answer is yes you can. But it could come with a lot of challenges. Especially if there is more than one sibling.

Most often siblings want to buy the parents house because of emotional attachment. A challenge may be that they are not in a financial position to buy the house. It may be difficult on you that has the sell my parents house to siblings option. You may have to be the one that tells them no. It can cause problems in the family when you do this.

It may well be that you need to sell parents house to pay for care that they will need. The sibling who wants to buy the house does not understand this. They will not understand that you cannot give them the house without proper cash. You need to sell parents house to pay for care.

The sell my parents house to siblings challenges can include several siblings. They each may want to buy the house. Then when selling your parents house you have to deal with trying to decide which sibling to sell to. Any decision made to sell to one would be unfair to the others.

The best way to avoid the sell my parents house to siblings is to make the decision to put the house on the market. Which now when selling your parents houses creates new challenges. Chances are you are going to want to consider fast ways to sell parents house options.

Once you have decided the sell my parents house to siblings won’t work there are other options. One of these that many consider first is the for sale by owner. They think that this is one of the fast ways to sell my parents house options. Often they end up disappointed. The house may not sell fast. Then the sell my parents house to siblings question may get raised again.

There are a lot of challenges that come with the for sale by owner options. It can be difficult to determine what houses like your parents house are selling for. You need to do a lot of research for what is selling in the area.

Then you have to decide how you are going to list it. This means you need to find good venues for doing this. You can use the internet for this. But this comes with some extra challenges. It can be hard finding the right spots on the internet to get the exposure that you need.

Along with this it will be time consuming for you. If you are not considering the sell my parents house to siblings. The siblings may not be willing to help you sell your elderly parents home.

There may be a problem with your parents home. It may need repairs. Quite often the elderly are not able to handle the upkeep of the home. As a result it gets run down. Prospective buys may want a home inspection. The home may not pass. You will then have to deal with repairs. These can be time consuming and costly. Not to mention its hard on your parents.

You may need to look at other options besides the sell my parents house to siblings. Or to go with a sale by owner. You will not likely want to go the traditional method which is selling through a real estate agency. It can take time. Plus, it will present some of the same problems. The problems that come with the sale by owner.

All this may seem discouraging. But there is a great solution.

The sell my parents house to siblings may not be workable. You may need to sell parents house to pay for care. It means you need cash. You can use the sell house for cash option. This is a total problem solver.

There are trustworthy buyers who buy houses for cash. It means that your parents will have the funds they need. They will get this cash fast. It can then go towards their new accommodation. Or any special care that they need. It is going to be a big time saver. The deal can close immediately. It means cash is on hand much faster.

Plus the sell house for cash deal can save your parents money. There is no need to generate money for house repairs. The sell house for cash deals don’t need home inspections. That means the parents don’t go through the hassles of putting up with repairs. For you it means a lot less stress. You no longer have to look for fast ways to sell parents house options. You don’t have to deal with the sell my parents house to siblings problem.

There is no tasks of having to list and show the house. You can now focus on the care that your parents need. You will have the money in hand to get them settled in a new environment. An added bonus is there are no realtor fees to deal with. Also, no worries about having people come through the house for showings.

All the decision between siblings will be over with. The sell house for cash option is a great alternative for selling your parents house.

You don’t need to stress about how to sell your parents house. If you need to sell it today, don’t jump through the hoops of selling it to your siblings. We understand that you need to sell your parents house as soon as possible, and that the house selling process is stressful. At PHP Houses we specialize in closing on houses quickly so that you can move on to the other more important things in life.

Do you have a question about the house selling process? Do you want to get your no obligation cash offer for your parents house? Even if you don’t decide to sell, we’d love to answer any questions you might have. Give us a call today at 407-641-1531.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

3 Tips for Buying a Home Today

If you put off your home search at any point over the past two years, you may want to consider picking it back up based on today’s housing market conditions. Recent data shows the supply of homes for sale is increasing, giving buyers like you additional options.

But it’s important to keep in mind that while inventory is improving, it’s still a sellers’ market. And that means you need to be prepared as you set out on your home search. Here are three tips for buying the home of your dreams today.

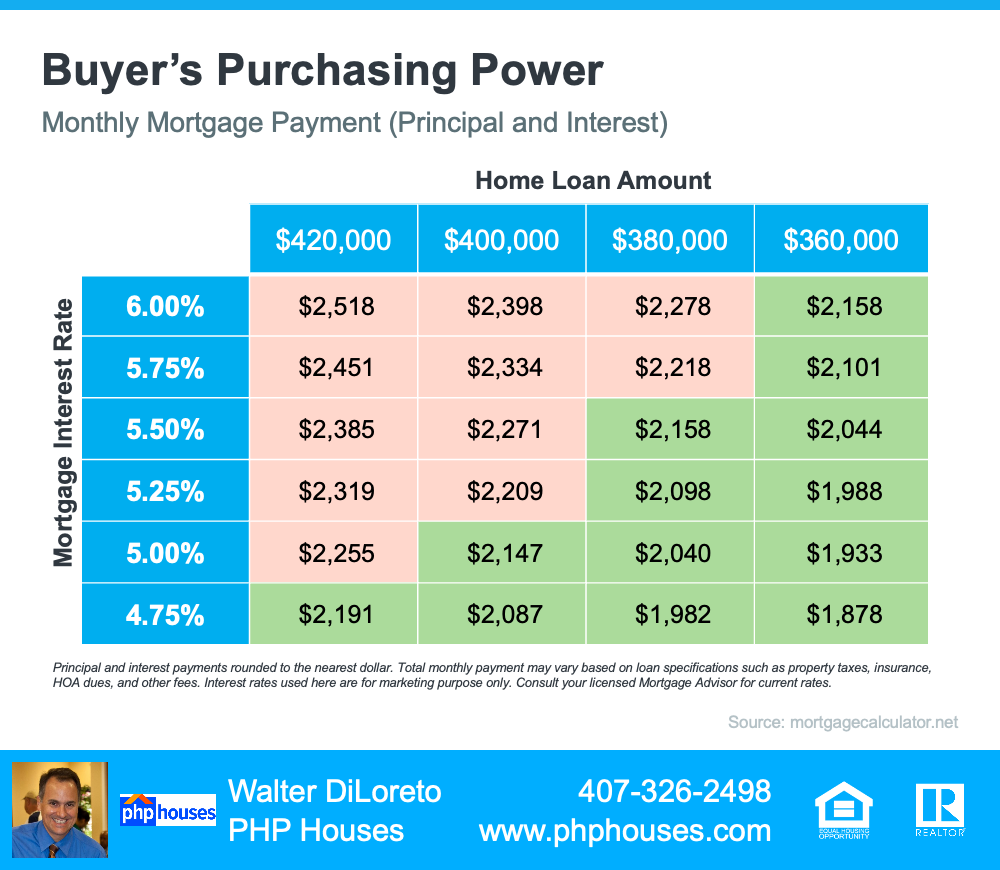

Mortgage rates have increased significantly this year, and over the past few weeks, they’ve been fluctuating quite a bit. It’s important to stay up to date on what’s happening with rates and understand how they can impact your purchasing power when you’re thinking of buying a home. The chart below can help.

Let’s say your budget allows for a monthly mortgage payment in the $2,100-$2,200 range. The green in the chart indicates a payment within or below that range, while the red is a payment that exceeds it.

Buyer’s Purchasing Power

As the chart shows, even a small change in mortgage rates can have a big impact on your monthly payments. If rates rise, you could exceed your budget unless you pursue a lower home loan amount. If rates fall, your purchasing power may increase, which could give you additional options for your search.

The supply of homes for sale is improving, which gives you more homes to choose from. But historically, supply is still low. That means as you search for homes, if you still don’t find something that meets your needs, it may be worth expanding your search.

A recent article from the Washington Post highlights a few things buyers can consider today. It encourages opening yourself up to more areas. For example, if there’s a location you’ve previously ruled out (like a particular town, for example) it may be worth taking another look.

And if you’re able to, opening your search up to include other housing types, like newly built homes, condominiums, or townhomes can further increase your pool of options. Even as the inventory of homes for sale improves today, finding ways to cast a wider net during your search could help you find a hidden gem.

Ultimately, you need to be prepared when you set out to buy a home. Jeff Ostrowski, Senior Mortgage Reporter for Bankrate, explains:

“Taking the leap to homeownership can provide a feeling of pride while boosting your long-term financial outlook, if you go in well-prepared and with your eyes open.”

No matter where you’re at in your homeownership journey, the best way to make sure you’re set up for success is to work with a real estate professional. If you’re just starting your search, a real estate professional can help you understand your local market and search for available homes. And when it’s time to make an offer, they’ll be an expert advisor and negotiator to help yours stand out above the rest.

Strategically planning your home search by understanding today’s mortgage rates, casting a wide net, and building a team of experts can be the keys to finding the home of your dreams. To make sure you have expert advice each step of the way, let’s connect.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 641-1531

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

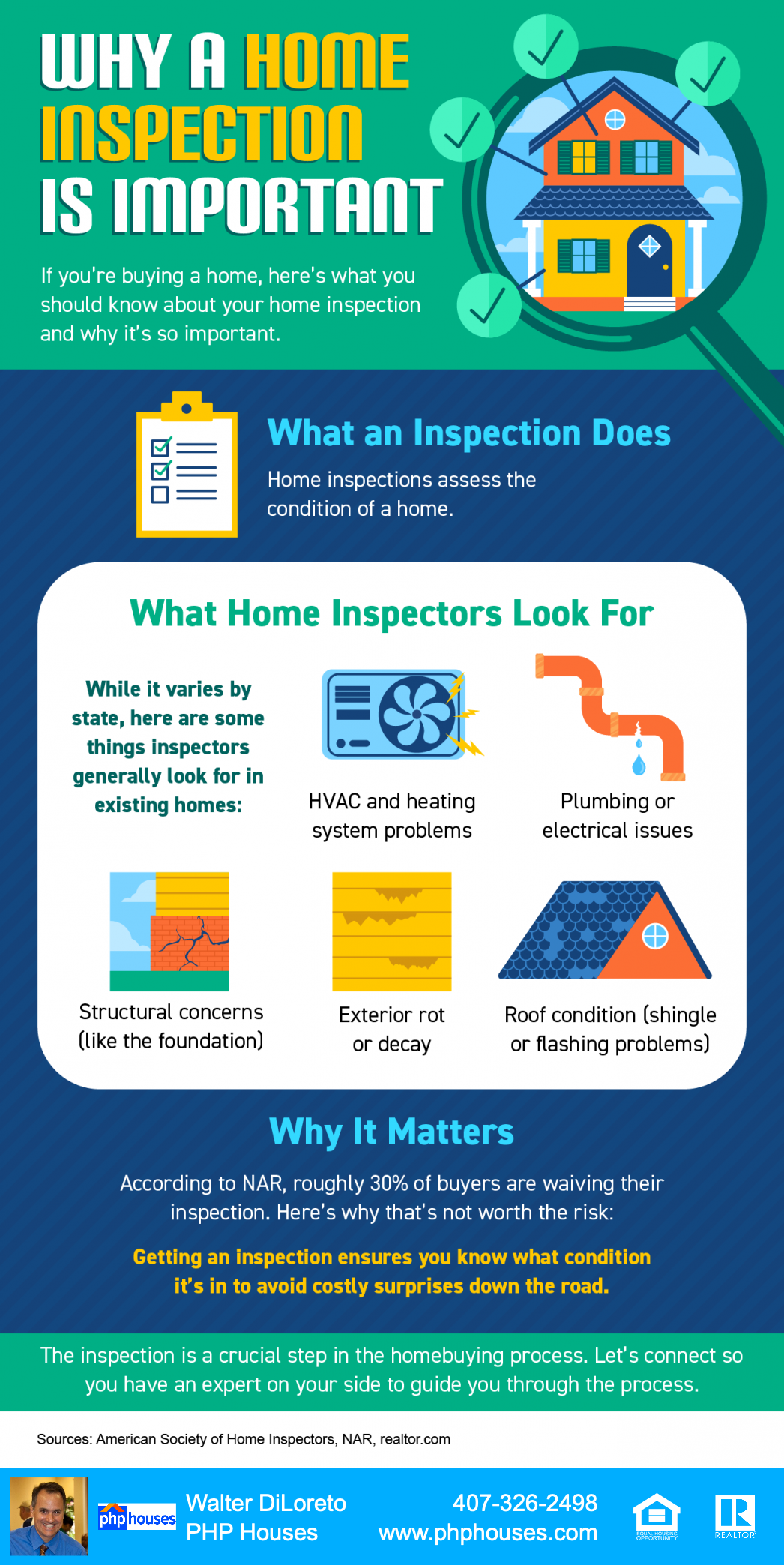

Why a Home Inspection Is Important [INFOGRAPHIC]

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 641-1531

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

Planning To Retire? Your Equity Can Help You Reach Your Goal.

Whether you’ve just retired or you’re thinking about retirement, you may be considering your options and trying to picture a whole new stage of your life. And you’re not alone. Research from the Retirement Industry Trust Association (RITA) shows 10,000 Baby Boomers reach the typical retirement age (65) every day, and only 47% of the people in that generation have already retired.

If this sounds like you, one thing worth considering is whether or not your current home will suit your new lifestyle. If your home doesn’t have the features or benefits you’re looking for, the good news is, you may be in a better position to move than you realize.

That’s because, if you already own a home, you’ve likely built-up significant equity, and that can help you fuel your next move. According to the National Association of Realtors (NAR):

“A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.”

In fact, over the last twelve months, CoreLogic reports the average homeowner in the United States gained roughly $64,000 in equity due to home price appreciation.

You can use your equity to help you achieve your homeownership goals. Whether you want to downsize, move closer to loved ones, or buy a home in a dream destination, your equity can help get you there. It may be some (if not all) of what you’d need as your down payment on a home that better fits your changing needs.

To find out how much equity to have in your home, reach out to a trusted real estate professional today.

Retirement is a big step and so is buying or selling a home. As you move into this new phase of life, let’s connect so you have an expert to guide you through the process as you sell your current home and give you expert advice as you buy one that’ll better suit your needs.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 641-1531

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

Selling one’s own house can be a big enough challenge. But when one has to take on the sell parents house task it becomes an even bigger job. There are some options to use to sell mom and dads house.

There are different options to sell mom and dad’s house. They are choices when taking on the task to sell parents house.

The traditional method of selling a house is by using the services of a real estate agent. Anyone that has bought or sold a house knows how this works. For those that haven’t there are some basic things to keep in mind.

The responsibilities that you will have will depend. If you are about to sell parents house after death, you may have more legal responsibilities. You may be about to sell parents house. It could be because they are moving. You are facing different challenges.

In either case you will have to work with the real estate agent. There are some things that you will need to do.

First you will want to pick a real estate agency that has a good track record for selling homes in your area. It will be important because most likely you will want to try for a quick sale. But, at the same time you want the home to sell for what it is worth.

Then you are going to have to make sure that you have time set aside. There should be showings and its likely you will want to be in the home during this. If your parents are elderly it can be upsetting for them to have strangers come through their home.

If the house sells then you have all the legal aspects of the sale to attend to. How much responsibility you will have to take on will depend on the age and stability of your parents. When one has the sell parents house responsibility they also have the legal responsibilities. There are some that have the sell parents house after death task. The legal responsibilities can be even greater.

When you go to sell mom and dads house it may be confusing. Most often confusing for them. It is easier if you brush up on the how to sell a house by owner tactics. It means one less person to deal with. It may be more comforting for your parents. But, it will create even greater responsibility for you. Some individuals try this method at first to sell parents house after death. There are a lot more steps to go through to sell parents house by owner.

The first step will be to determine what the houses in the area are selling for. This takes some time to do the research. It can be a daunting task because you won’t have the resources that the realtor will have. It will mean checking out the local listings. It will help to see what the houses are listed for. But, it won’t tell you what they sold for.

The next step will be at least taking a few images. You may be going to try to use the internet as it is one of the how to sell a house by owner tactics. The sell parents house procedure using this method can be frustrating.

Then you are going to want to find as many resources as you can to market the house. You shouldn’t rely on just one resource. At least not if you want to sell the house as quick as possible. Other resources include using local newspapers. Then putting a private sale sign on the property is another option.

Beprepared for the showings. It is going to be the next task. You do not want interested buyers coming to the door. It can be disturbing your parents. If you are about to sell prarents house after death, then the house might be empty. You will need to be available to show the house.

Finally if the house does sell you are going to be responsible for all the legalities. You have the extra burden of knowing how to draft the sale papers. Then you will need a lawyer to ensure these get done right. Plus, the lawyer will have to look after the closing.

Another huge task that comes when you go to sell parents house is getting it ready for sale. This is required no matter which option you choose. It means doing an inspection of the home to see what repairs you will need to do. Most likely a home inspection is conducted at the request of the potential buyers. You need to be sure to take care of any issue they may have. Otherwise most likely a proposed sale will not go through

While the first two options are available there is a third option. For those that have the sell parents house this option often proves to be the most viable. It is to sell to a cash buyer. All one has to do is look at the advantages of doing it this way, so you know it’s the right way.

Then there are extra important benefits. This sell parents house option to a cash buyer means that the house is bought for in cash. There are no real estate commissions. For those whose parents are still living they now have fast cash to help them get settled in a new place. For those that have to sell parents house after death there is the cash available. Cash to be able to handle all the expenses that may have occurred because of this. Out of all the options to sell parents home, this one is by far the quickest, easiest and hassle free method.

At PHP Houses we specialize in a quick sale so that you can get on with the more important things in life. Don’t stress out about selling your parents’ house. In the event you need to sell your parents’ house before death, give us a call at 407-641-1531. We would love to answer any questions about the house selling process that you might have.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

What Would a Recession Mean for the Housing Market?

According to a recent survey from the Wall Street Journal, the percentage of economists who believe we’ll see a recession in the next 12 months is growing. When surveyed in July 2021, only 12% of economists consulted thought there’d be a recession by now. But this July, when polled, 49% believe we will see a recession in the coming 12 months.

And as more recession talk fills the air, one concern many people have is: should I delay my homeownership plans if there’s a recession?

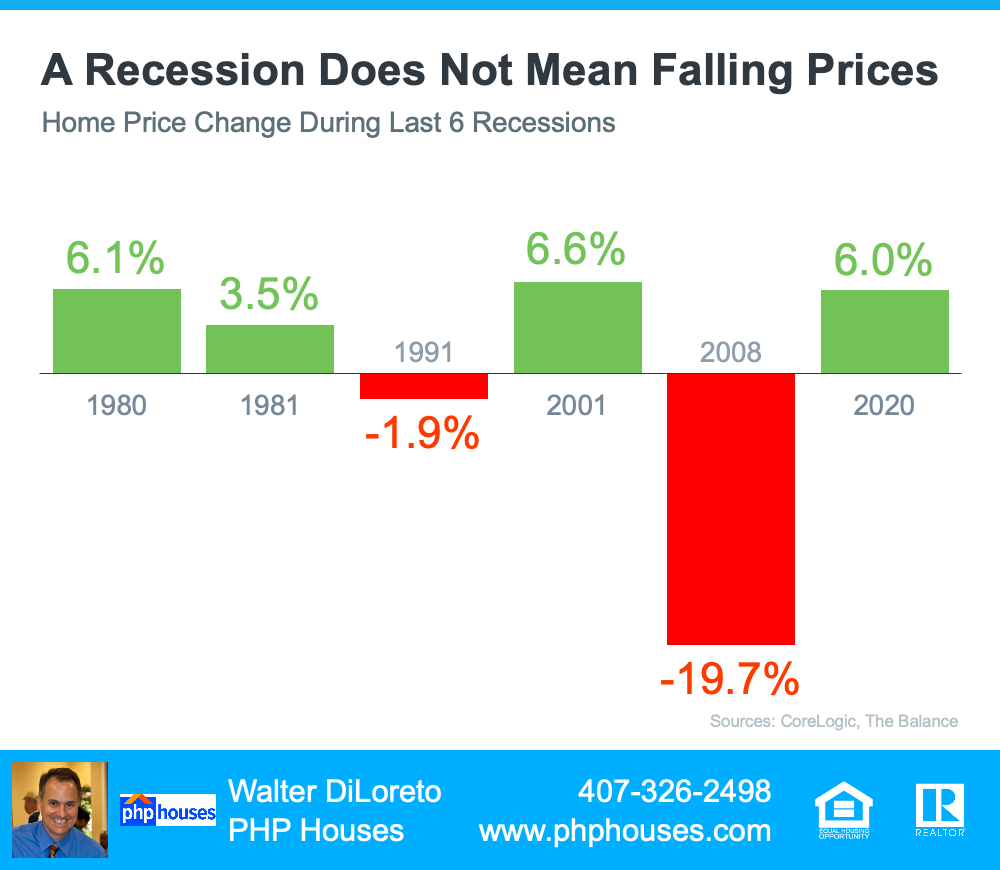

Here’s a look at historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession would mean for the housing market today.

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at the recessions going all the way back to 1980, home prices appreciated in four of the last six recessions. So, historically, when the economy slows down, it doesn’t mean home values will fall.

A Recession Does Not Mean Falling Prices

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would repeat what happened then. But this housing market isn’t about to crash. The fundamentals are very different today than they were in 2008. So, don’t assume we’re heading down the same path.

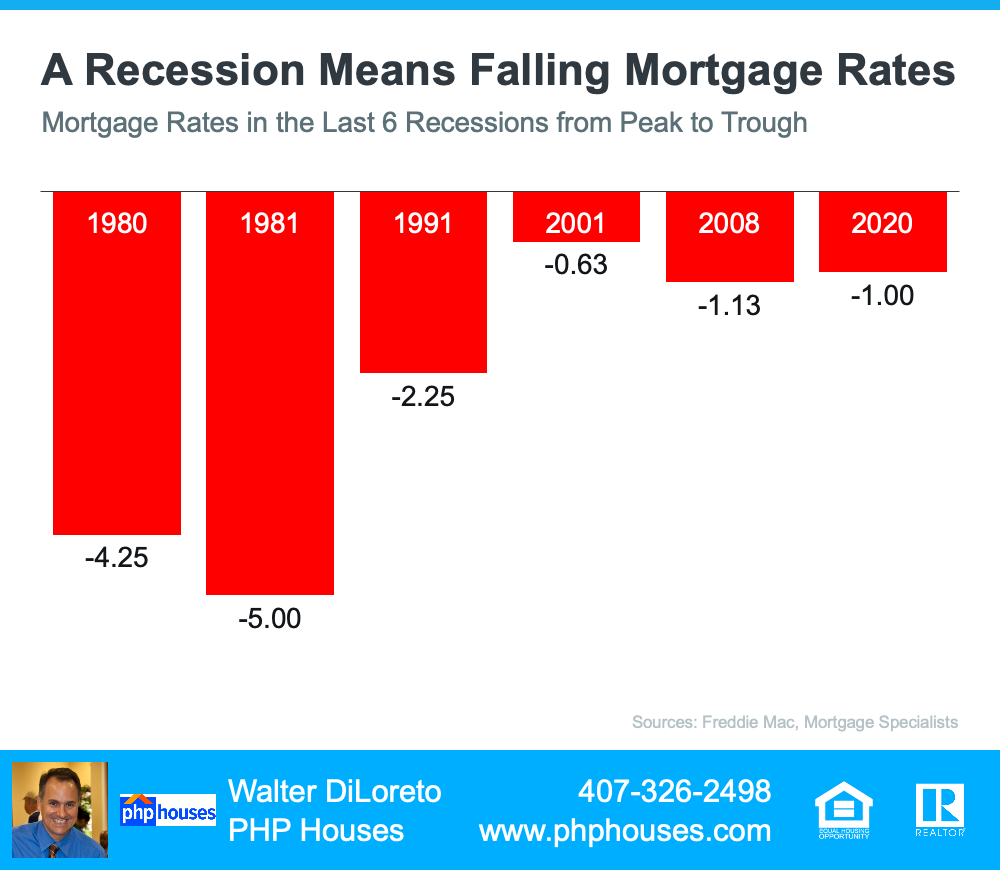

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the chart below shows, historically, each time the economy slowed down, mortgage rates decreased.

A Recession Means Falling Mortgage Rates

Fortune explains that mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

And while history doesn’t always repeat itself, we can learn from and find comfort in the historical data.

There’s no doubt everyone remembers what happened in the housing market in 2008. But you don’t need to fear the word recession if you’re planning to buy or sell a home. According to historical data, in most recessions, home price gains have stayed strong, and mortgage rates have declined.

If you’re thinking about buying or selling a home, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 641-1531

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram