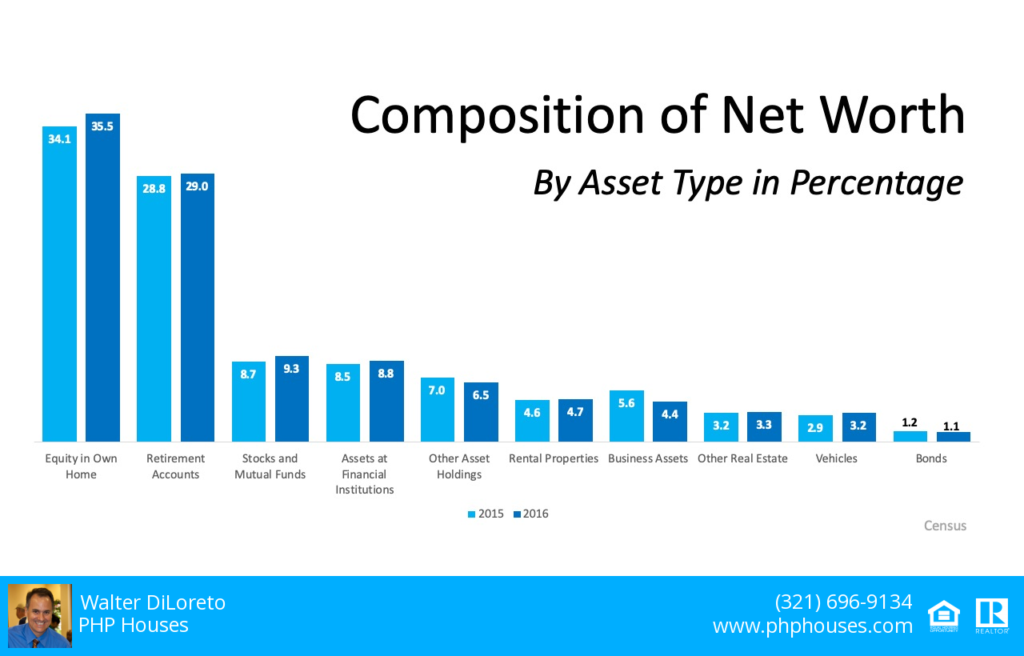

Many people plan to build their net worth by buying CDs or stocks, or just having a savings account. Recently, however, Economist Jonathan Eggleston and Survey Statistician Donald Hays, both of the U.S. Census Bureau,shared the biggest determinants of wealth,

“The biggest determinants of household wealth [are] owning a home and having a retirement account.” (Shown in the graph above).

This does not come as a surprise, as we often mention that homeownership can help you to increase your family’s wealth. This study reinforces that idea,

“Net worth is an important indicator of economic well-being and provides insights into a household’s economic health.”

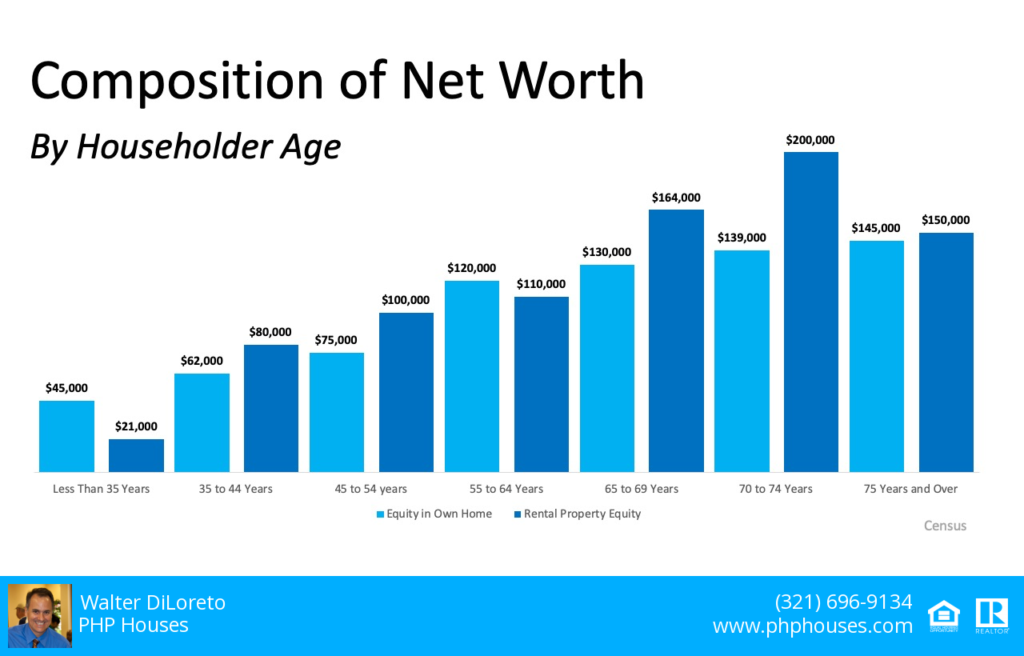

Having equity in your home can help your family move in that direction, building toward substantial financial growth. According to the report noted above, people are not only creating net worth in the homes they live in, but many are also earning equity in rental property investments too. (See below):

“If you don’t own a home, buy one. If you own one home, buy another one, and if you own two homes buy a third and lend your relatives the money to buy a home.”

Bottom Line

There are financial and non-financial benefits to owning a home. If you would like to increase your net worth, let’s get together so you can learn all the benefits of becoming a homeowner.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

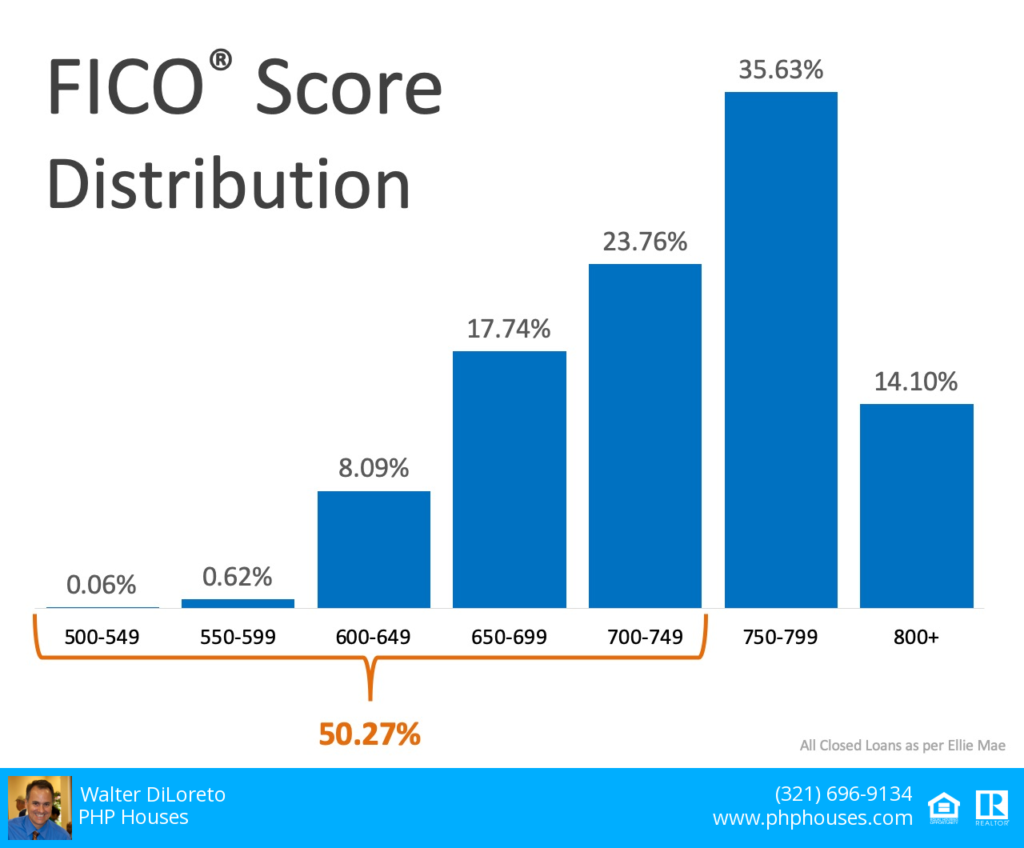

While a recent announcement from CNBC shares that the average national FICO® score has reached an all-time high of 706, the good news for potential buyers is that you don’t need a score that high to qualify for a mortgage. Let’s unpack the credit score myth so you can to become a homeowner sooner than you may think.

With today’s low interest rates, many believe now is a great time to buy – and rightfully so! Fannie Mae recently noted that 58% of Americans surveyed say it is a good time to buy. Similarly, the Q3 2019 HOME Survey by the National Association of Realtors said 63% of people believe now is a good time to buy a home. Unfortunately, fear and misinformation often hold qualified and motivated buyers back from taking the leap into homeownership.

“For the first time, the average national credit score has reached 706, according to FICO®, the developer of one of the most commonly used scores by lenders.”

This is great news, as it means Americans are improving their credit scores and building toward a stronger financial future, especially after the market tumbled during the previous decade. With today’s strong economy and increasing wages, many Americans have had the opportunity to improve their credit over the past few years, driving this national average up.

Since Americans with stronger credit are now entering the housing market, we are seeing an increase in the FICO® Score Distribution of Closed Loans (see graph above).

But hang on – don’t forget that this does not mean you need a FICO® score over 700 to qualify for a mortgage. Here’s what Experian, the global leader in consumer and business credit reporting, says:

FHA Loan:“FHA loans are ideal for those who have less-than-perfect credit and may not be able to qualify for a conventional mortgage loan. The size of your required down payment for an FHA loan depends on the state of your credit score: If your credit score is between 500 and 579, you must put 10% down. If your credit score is 580 or above, you can put as little as 3.5% down (but you can put down more if you want to).”

Conventional Loan:“It’s possible to get approved for a conforming conventional loan with a credit score as low as 620, although some lenders may look for a score of 660 or better.”

USDA Loan: “While the USDA doesn’t have a set credit score requirement, most lenders offering USDA-guaranteed mortgages require a score of at least 640.”

VA Loan:“As with income levels, lenders set their own minimum credit requirements for VA loanborrowers. Lenders are likely to check credit scores as part of their screening process, and most will set a minimum score, or cutoff, that loan applicants must exceed to be considered.”

Bottom Line

As you can see, plenty of loans are granted to buyers with a FICO® score that is lower than the national average. If you’d like to understand the next steps to take when determining your credit score, let’s get together so you can learn more.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

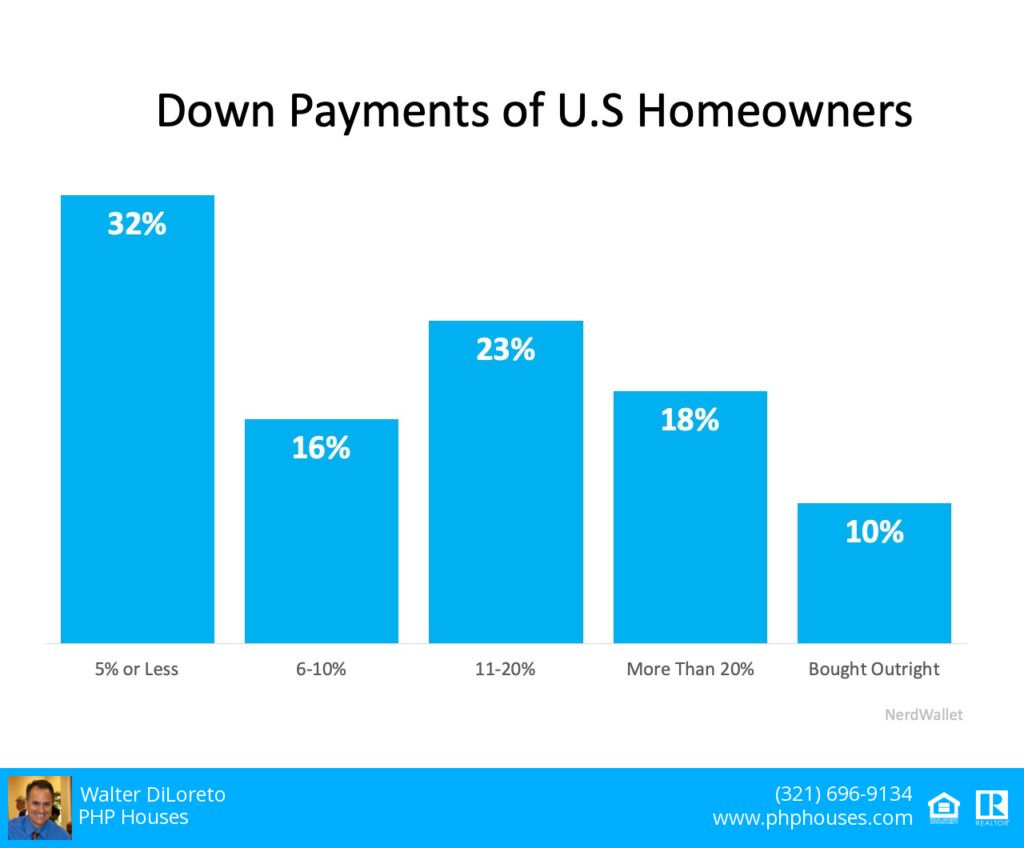

According to the ‘2019 Home Buyer Report’ conducted by Nerdwallet, many first-time buyers still believe they need a 20% down payment to buy a home in today’s market:

“More than 6 in 10 (62%) Americans believe you must put at least 20% down in order to purchase a home.”

When potential homebuyers think they need a 20% down payment to enter the market, they also tend to think they’ll have to wait several years (in some markets) to come up with the necessary funds to buy their dream homes. The report continues to say,

“The truth: 32% of current U.S. homeowners put 5% or less down on their home, according to census data.” (as shown above).

The lack of knowledge about the home-buying process is unfortunately keeping many motivated buyers on the sidelines.

Bottom Line

Don’t let a lack of understanding keep you and your family out of the housing market. Let’s get together to discuss your options today.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

According to CoreLogic, from 2006 to 2014 “there were 7.3 million housing foreclosures and 1.9 million short sales.” The hesitation some Americans feel after experiencing a foreclosure brings to mind the old saying: “Fool me once- shame on you. Fool me twice- shame on me.”

“Thirteen percent of Americans have lost a home due to a financial event such as foreclosure in the past 10 years. More than 6 in 10 of them (61%) have not bought a home since, and 20% of those who haven’t repurchased say they never plan to again.”

This makes sense. They don’t want to go through the same pain again. As a cornerstone of the American dream, nobody wants to lose homeownership. But let’s illustrate this simply: Recall learning to ride your first bike during your childhood. Did you stop riding it because you fell on the ground and scraped your knees? Or did you get back on and try again until you were able to ride without falling?

Purchasing a home is not as simple as learning to ride a bike, but the concept is the same! There are many things necessary to learn that affect the ability to get the financing needed to purchase a home. Past occurrences can determine if there is a waiting period. In other words, you need to let your knees heal before you try again!

As we’ve mentioned in the past, homeownership has many financial and non-financial benefits. Each person needs to go over the pros and cons, taking the time to figure out what is best for their family. Should they continue renting, or should they try to buy again?

The good news is that some “boomerang buyers” are getting back into the market. They’re getting back on their bike!

“Of 2.8 million former homeowners whose foreclosures, short sales or bankruptcies dropped off their credit reports from January 2016 to November 2018, 11.5% have obtained a new mortgage, according to a study by credit rating agency Experian for USA Today.”

NerdWallet’s report also mentioned:

6% plan to buy a house this year.

39% intend to buy over the next 3 years.

58% say they will purchase within 5 years.

Bottom Line

If you lost a home due to a financial event but would like to review your options, let’s get together to help you create a plan to obtain a home in the future!

Contact us: PHP Houses 142 W Lake view Ave Unit 1030 Lake Mary FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

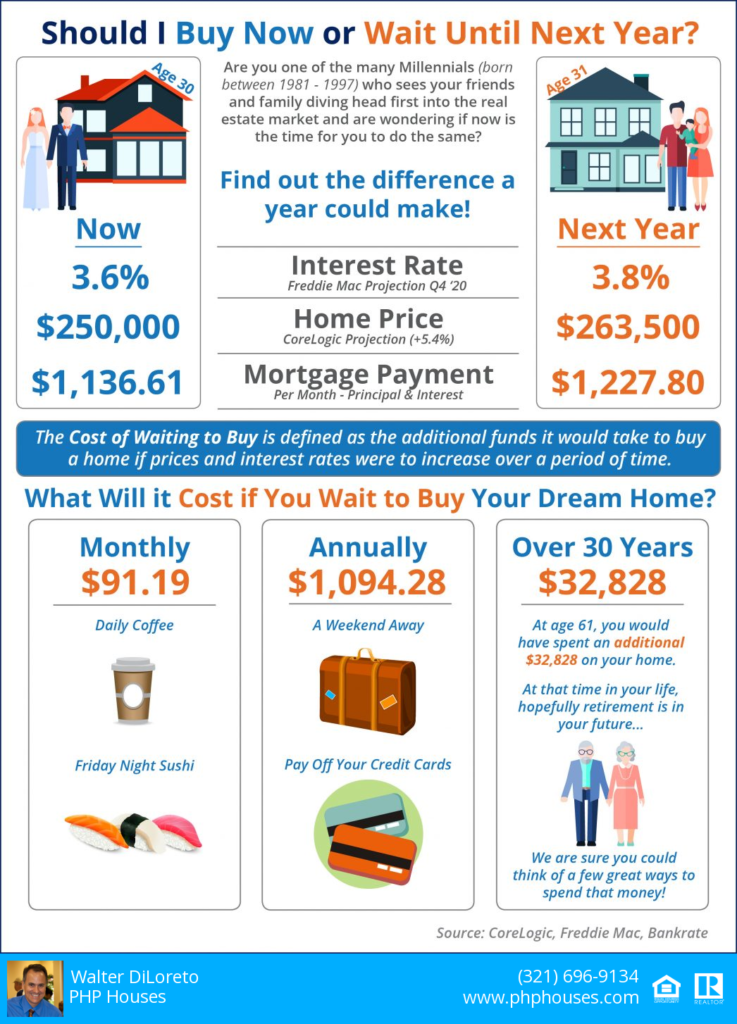

The “cost of waiting to buy” is defined as the additional funds necessary to buy a home if prices and interest rates were to increase over a period of time.

Freddie Macforecasts interest rates will rise to 3.8% by Q4 2020.

CoreLogicpredicts home prices will appreciate by 5.4% over the next 12 months.

If you’re ready and willing to buy your dream home, now is a great time to buy.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, Fl 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

Every year, ‘Black Friday’ is a highly anticipated event for eager shoppers. Some people prepare for weeks, crafting and refining a strategic shopping agenda, determining exactly when to arrive at each store, and capturing a wish list of discounted must-have items to purchase. But what about buying a home? Is there a ‘Black Friday’ for the home-buying process? Believe it or not, there is.

According to a new study from realtor.com, the week of September 22 is the best time of year to buy a home, making it ‘Black Friday’ for homebuyers.

After evaluating housing data in 53 metros from 2016 to 2018, realtor.com determined that the first week of fall is when buyers “tend to find less competition, more inventory, and the biggest reductions on list price.”

The report explains,

“During the first week of fall, buyers tend to face 26% less competition from other buyers, and they are likely to see 6.1% more homes available on the market compared to other weeks of the year…nearly 6% of homes on the market will also see price reductions, averaging 2.4% less than their peak.”

What’s so different about the first week of fall?

George Ratiu, Senior Economist with realtor.com says,

“As summer winds down and kids return to school, many families hit pause on their home search and wait until the next season to start again…as seasonal inventory builds up and restores itself to more buyer-friendly levels, fall buyers will be in a better position to take advantage of today’s low mortgage rates and increased purchasing power.”

Learn more about how prices, listings, and buyer competition stack up during the first week of fall in your metro area.

Bottom Line

If you want to take advantage of the ‘Black Friday’ of home buying, let’s get together to discuss the benefits of making your next move this fall.

Contact us: PHP Houses 142 W Lake Mary Ave Unit 1030 Lake Mary FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com