3 Reasons To Buy Before Spring

Comments (0)

Renters Missed Out on $51,500 This Past Year

Rents have increased significantly this year. The latest National Rent Report from Apartmentlist.com shows rents are rising at a rate much higher than the three years leading up to the pandemic:

“Since January of this year, the national median rent has increased by a staggering 16.4 percent. To put that in context, rent growth from January to September averaged just 3.4 percent in the pre-pandemic years from 2017-2019.”

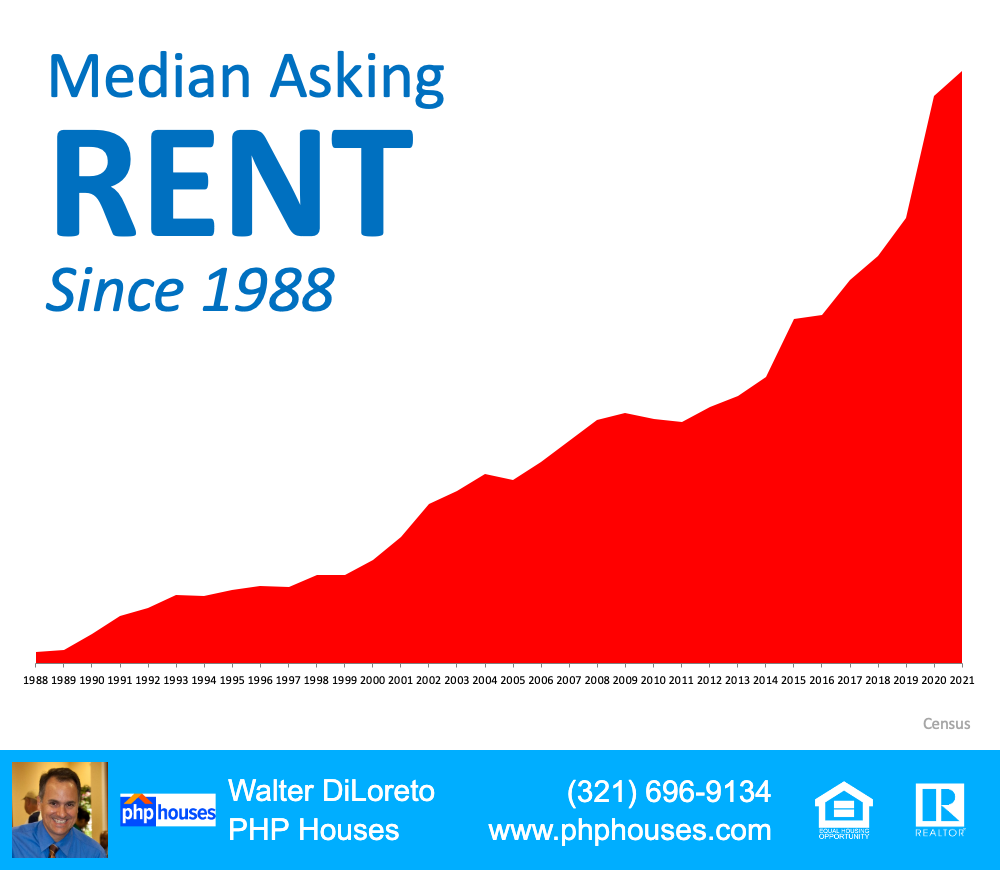

Looking back, we can see rents rising isn’t new. The median rental price has increased consistently over the past 33 years (see graph below):

Median Asking Rent Since 1988

If you’re thinking of renting for another year, consider that rents will likely be even higher next year. But that alone doesn’t paint the picture of the true cost of renting.

A homeowner’s monthly mortgage payment pays for their shelter, but it also acts as an investment. That investment grows in the form of equity as a homeowner makes their mortgage payment each month to pay down what they owe on their home loan. Their equity gets an additional boost from home price appreciation, which is at near-record levels this year.

The latest Homeowner Equity Insights report from CoreLogic found homeowners gained significant wealth through their home equity this past year. The research shows:

“. . . the average homeowner gained approximately $51,500 in equity during the past year.”

As a renter, you don’t get the same benefit. Your rent payment only covers the cost of shelter and any included amenities. None of your monthly rent payments come back to you as an investment. That means, by renting this year, you likely paid more in rent than you did in the previous year, and you also missed out on the potential wealth gain of $51,500 you could have had by owning your own home.

When deciding whether you should rent or buy in the future, keep in mind how much renting can cost you. Another year of renting is another year you’ll pay rising rents and miss out on building your wealth through home equity. Let’s connect today to talk more about the benefits of buying over renting.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

There Are More Homes Available Now than There Were This Spring

There’s a lot of talk lately about how challenging it can be to find a home to buy. While housing inventory is still low, there are a few important things to understand about the supply of homes for sale as we move into the end of the year.

In the residential real estate market, trends generally follow a predictable and seasonal pattern. Typically, the number of homes available for sale (or active monthly listings) peaks in the fall. But in a chapter where so little feels normal, the question becomes: should we expect a fall peak this year?

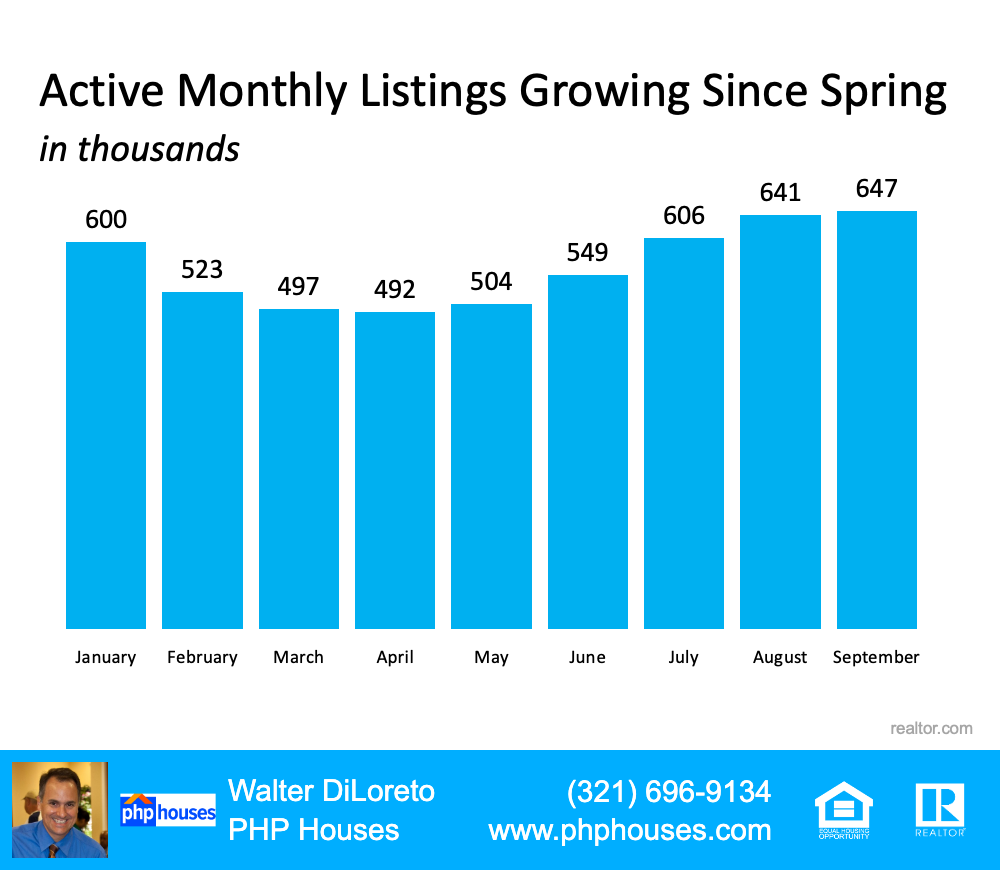

If we look at the active monthly listings for 2021 (shown in the chart below), we’ll see that the number of homes on the market has increased fairly steadily since spring this year. The realtor.com data shows we’re still seeing an increase in active inventory month-over-month. While that gain is a bit smaller month-to-month (see August to September in the chart), September numbers are still up from the month prior.

Active Monthly Listings Growing Since Spring (In Thousands)

The important takeaway here is the latest monthly numbers show growth. At the end of September, buyers had more options to pick from than they did this spring. That’s encouraging for buyers who may have paused their search months ago because they had trouble finding a home. Danielle Hale, Chief Economist at realtor.com, sums this up nicely:

“Put simply, this September buyers had more options than they’ve had all year and while that’s typical of early fall, that’s not what happened in 2020. Still, it’s important to remember that while buyers may have an easier time this fall than they did in the spring, the market remains more competitive than it has been historically at this time of year.”

As Hale says, a fall peak in inventory is in line with typical seasonal trends. While it’s impossible to say for certain what the future holds for housing inventory, we do know both buyers and sellers have opportunities this season based on the latest data.

If you’re thinking of buying a home, rest assured you do have more options now than you did earlier this year – and that’s a welcome relief. That said, today’s market is still highly competitive. This isn’t the time to slow your search. It’s actually the season when the number of homes available for sale tends to peak. Focus on the additional options with renewed energy this season and be prepared for ongoing competition from other buyers.

If you’re considering selling your house, realize that while growing, inventory is still low. Selling now means you’ll be in a great position to negotiate with buyers – and competition among buyers is good news for your bottom line. Eager buyers will likely be motivated to act before the holidays, giving you the benefit of a fast sale.

Whether you’re buying or selling, there’s still a chance to make your goals a reality this season. Let’s connect so we can discuss what’s going on with the local market and current trends and what they mean for you.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

What’s the Difference between an Appraisal and a Home Inspection?

If you’re planning to buy a home, an appraisal is an important step in the process. It’s a professional evaluation of the market value of the home you’d like to buy. In most cases, an appraisal is ordered by the lender to confirm or verify the value of the home prior to lending a buyer money for the purchase. It’s also a different step in the process from a home inspection, which assesses the condition of the home before you finalize the transaction. Here’s the breakdown of each one and why they’re both important when buying a home.

The National Association of Realtors (NAR) explains:

“A home purchase is typically the largest investment someone will make. Protect yourself by getting your investment appraised! An appraiser will observe the property, analyze the data, and report their findings to their client. For the typical home purchase transaction, the lender usually orders the appraisal to assist in the lender’s decision to provide funds for a mortgage.”

When you apply for a mortgage, an unbiased appraisal (which is required by the lender) is the best way to confirm the value of the home based on the sale price. Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal will help make sure the bank doesn’t loan you more than what the home is worth.

This is especially critical in today’s sellers’ market where low inventory is driving an increase in bidding wars, which can push home prices upward. When sellers are in a strong position like this, they tend to believe they can set whatever price they want for their house under the assumption that competing buyers will be willing to pay more.

However, the lender will only allow the buyer to borrow based on the value of the home. This is what helps keep home prices in check. If there’s ever any confusion or discrepancy between the appraisal and the sale price, your trusted real estate professional will help you navigate any additional negotiations in the buying process.

Here’s the key difference between an appraisal and an inspection. MSN explains:

“In simplest terms, a home appraisal determines the value of a home, while a home inspection determines the condition of a home.”

The home inspection is a way to determine the current state, safety, and condition of the home before you finalize the sale. If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you as a buyer have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. Your real estate agent is a key expert to help you through this part of the process.

The appraisal and the inspection are critical steps when buying a home, and you don’t need to manage them by yourself. Let’s connect today so you have the expert guidance you need to navigate through the entire homebuying process.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

Not All Agents Are Created Equal

In today’s fast-paced world where answers are just a Google search away, there are some who may question the benefits of hiring a real estate professional when selling a house. The reality is, the addition of more information can lead to more confusion. A real estate agent can be your essential guide, but truth be told, not all agents are created equal. Finding the right agent for you and your family should be your top priority when you’re ready to sell your house.

The right agent is the person who can truly walk you through the whole process, look out for your best interest, and seamlessly lead you through all the steps along the way. In today’s complex market, the way we execute real estate transactions is changing constantly, especially as more elements can be done virtually. Making sure you have the best advice on your side is more important than ever.

It starts with trust. You must trust the advice this person is going to give you, and you’ll want to begin by making sure you’re connected to a true professional. An agent can’t give you perfect advice because it’s impossible to know exactly what’s going to happen at every turn – especially in this unique market. A true professional agent can, however, give you the best advice possible based on the information and situation at hand, helping you make the necessary adjustments and best decisions along the way. The right agent – the professional – will get you the best offer available. That’s exactly what you want and deserve.

1. Navigate the Process

There are over 230 possible steps that take place during a successful real estate transaction. Don’t you want someone who has been there before, someone who knows what these actions are, to ensure you have a positive selling experience?

2. Negotiate on Your Behalf

Today, hiring a trusted and talented negotiator could save you thousands, perhaps tens of thousands of dollars. Each step – from the buyer submitting an original offer, to the possible renegotiation of that offer after a home inspection, to the potential cancelation of the deal based on a troubled appraisal – you need someone who can keep the deal together until it closes.

3. Price Your House Competitively

There’s so much information in the news and on the Internet about home sales, prices, and mortgage rates. How do you know what’s going on in our local area? Who do you turn to in order to competitively and correctly price your home at the beginning of the selling process?

Dave Ramsey, known as the financial guru, advises:

“When getting help with money, whether it’s insurance, real estate or investments, you should always look for someone with the heart of a teacher, not the heart of a salesman.”

Hiring a trusted professional who has a finger on the pulse of the market and is eager to help you learn will make your experience an informed and educated one. You need someone who’s going to tell you the truth, not just what they think you want to hear.

Today’s real estate market is highly competitive. Having a trusted professional who’s been there before to guide you through the process is a simple step that will give you a huge advantage when you’re ready to sell your house. Let’s make it happen together.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

We Remember & Honor Those Who Gave All

We remember, today and always.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

Are We About to See a New Wave of Foreclosures?

With all of the havoc being caused by COVID-19, many are concerned we may see a new wave of foreclosures. Restaurants, airlines, hotels, and many other industries are furloughing workers or dramatically cutting their hours. Without a job, many homeowners are wondering how they’ll be able to afford their mortgage payments.

In spite of this, there are actually many reasons we won’t see a surge in the number of foreclosures like we did during the housing crash over ten years ago. Here are just a few of those reasons:

During the previous housing crash, the government was slow to recognize the challenges homeowners were having and waited too long to grant relief. Today, action is being taken swiftly. Just this week:

When the housing market was going strong in the early 2000s, homeowners gained a tremendous amount of equity in their homes. Many began to tap into that equity. Some started to use their homes as ATM machines to purchase luxury items like cars, jet-skis, and lavish vacations. When prices dipped, many found themselves in a negative equity situation (where the mortgage was greater than the value of their homes). Some just walked away, leaving the banks with no other option but to foreclose on their properties.

Today, the home equity situation in America is vastly different. From 2005-2007, homeowners cashed out $824 billion worth of home equity by refinancing. In the last three years, they cashed out only $232 billion, less than one-third of that amount. That has led to:

Even if prices dip (and most experts are not predicting that they will), most homeowners will still have vast amounts of value in their homes and will not walk away from that money.

The government is aware of the financial pain this virus has caused and will continue to cause. Yesterday, the Associated Press reported:

“In a memorandum, Treasury proposed two $250 billion cash infusions to individuals: A first set of checks issued starting April 6, with a second wave in mid-May. The amounts would depend on income and family size.”

The plan also recommends $300 billion for small businesses.

These are not going to be easy times. However, the lessons learned from the last crisis have Americans better prepared to weather the financial storm. For those who can’t, help is on the way.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Three Reasons Why This Is Not a Housing Crisis

In times of uncertainty, one of the best things we can do to ease our fears is to educate ourselves with research, facts, and data. Digging into past experiences by reviewing historical trends and understanding the peaks and valleys of what’s come before us is one of the many ways we can confidently evaluate any situation. With concerns of a global recession on everyone’s minds today, it’s important to take an objective look at what has transpired over the years and how the housing market has successfully weathered these storms.

We all remember 2008. This is not 2008. Today’s market conditions are far from the time when housing was a key factor that triggered a recession. From easy-to-access mortgages to skyrocketing home price appreciation, a surplus of inventory, excessive equity-tapping, and more – we’re not where we were 12 years ago. None of those factors are in play today. Rest assured, housing is not a catalyst that could spiral us back to that time or place.

According to Danielle Hale, Chief Economist at Realtor.com, if there is a recession:

“It will be different than the Great Recession. Things unraveled pretty quickly, and then the recovery was pretty slow. I would expect this to be milder. There’s no dysfunction in the banking system, we don’t have many households who are overleveraged with their mortgage payments and are potentially in trouble.”

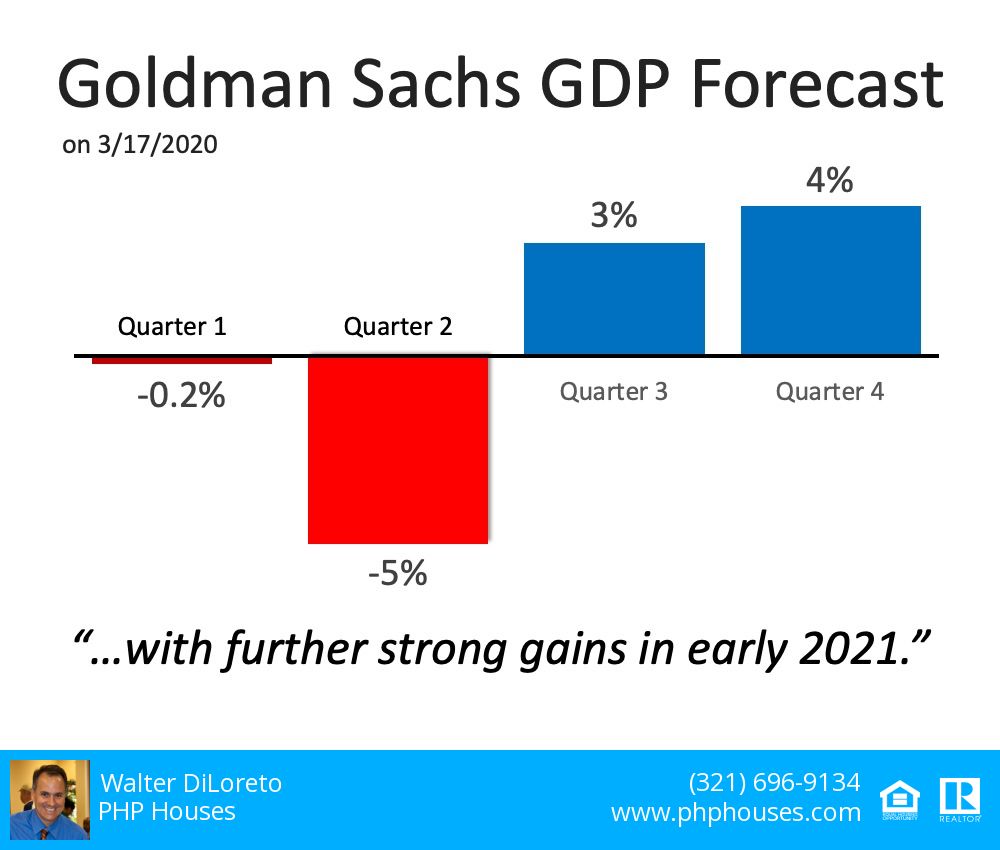

In addition, the Goldman Sachs GDP Forecast released this week indicates that although there is no growth anticipated immediately, gains are forecasted heading into the second half of this year and getting even stronger in early 2021.

Goldman Sachs GDP Forecast

Both of these expert sources indicate this is a momentary event in time, not a collapse of the financial industry. It is a drop that will rebound quickly, a stark difference to the crash of 2008 that failed to get back to a sense of normal for almost four years. Although it poses plenty of near-term financial challenges, a potential recession this year is not a repeat of the long-term housing market crash we remember all too well.

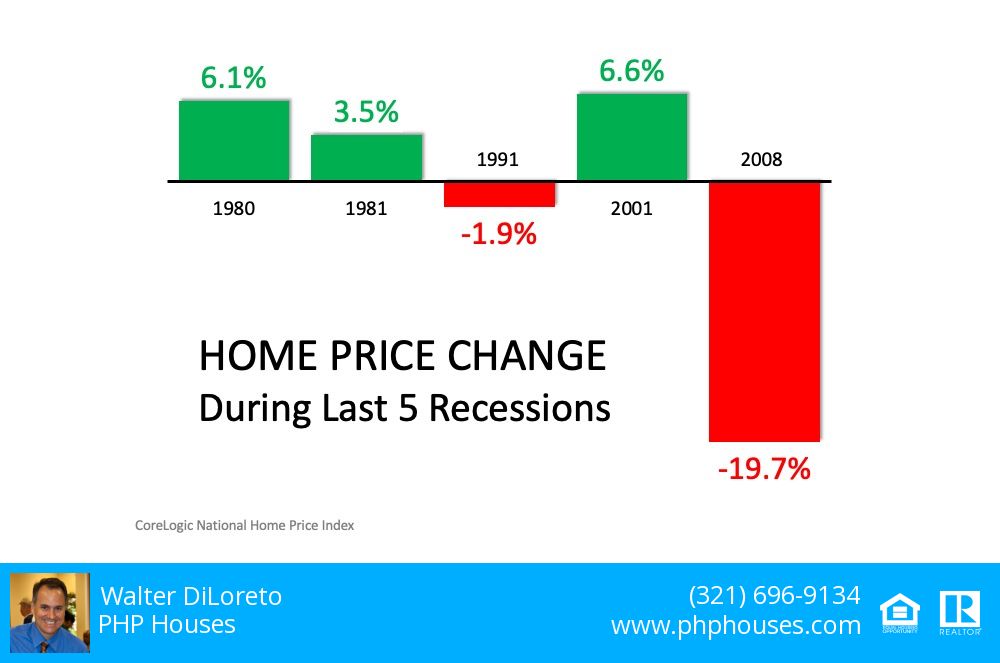

Next, take a look at the past five recessions in U.S. history. Home values actually appreciated in three of them. It is true that they sank by almost 20% during the last recession, but as we’ve identified above, 2008 presented different circumstances. In the four previous recessions, home values depreciated only once (by less than 2%). In the other three, residential real estate values increased by 3.5%, 6.1%, and 6.6% (see below):

Home Price Change During Last 5 Recessions

Concerns about the global impact COVID-19 will have on the economy are real. And they’re scary, as the health and wellness of our friends, families, and loved ones are high on everyone’s emotional radar.

According to Bloomberg,

“Several economists made clear that the extent of the economic wreckage will depend on factors such as how long the virus lasts, whether governments will loosen fiscal policy enough and can markets avoid freezing up.”

That said, we can be confident that, while we don’t know the exact impact the virus will have on the housing market, we do know that housing isn’t the driver.

The reasons we move – marriage, children, job changes, retirement, etc. – are steadfast parts of life. As noted in a recent piece in the New York Times, “Everyone needs someplace to live.” That won’t change.

Concerns about a recession are real, but housing isn’t the driver. If you have questions about what it means for your family’s homebuying or selling plans, let’s connect to discuss your needs.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

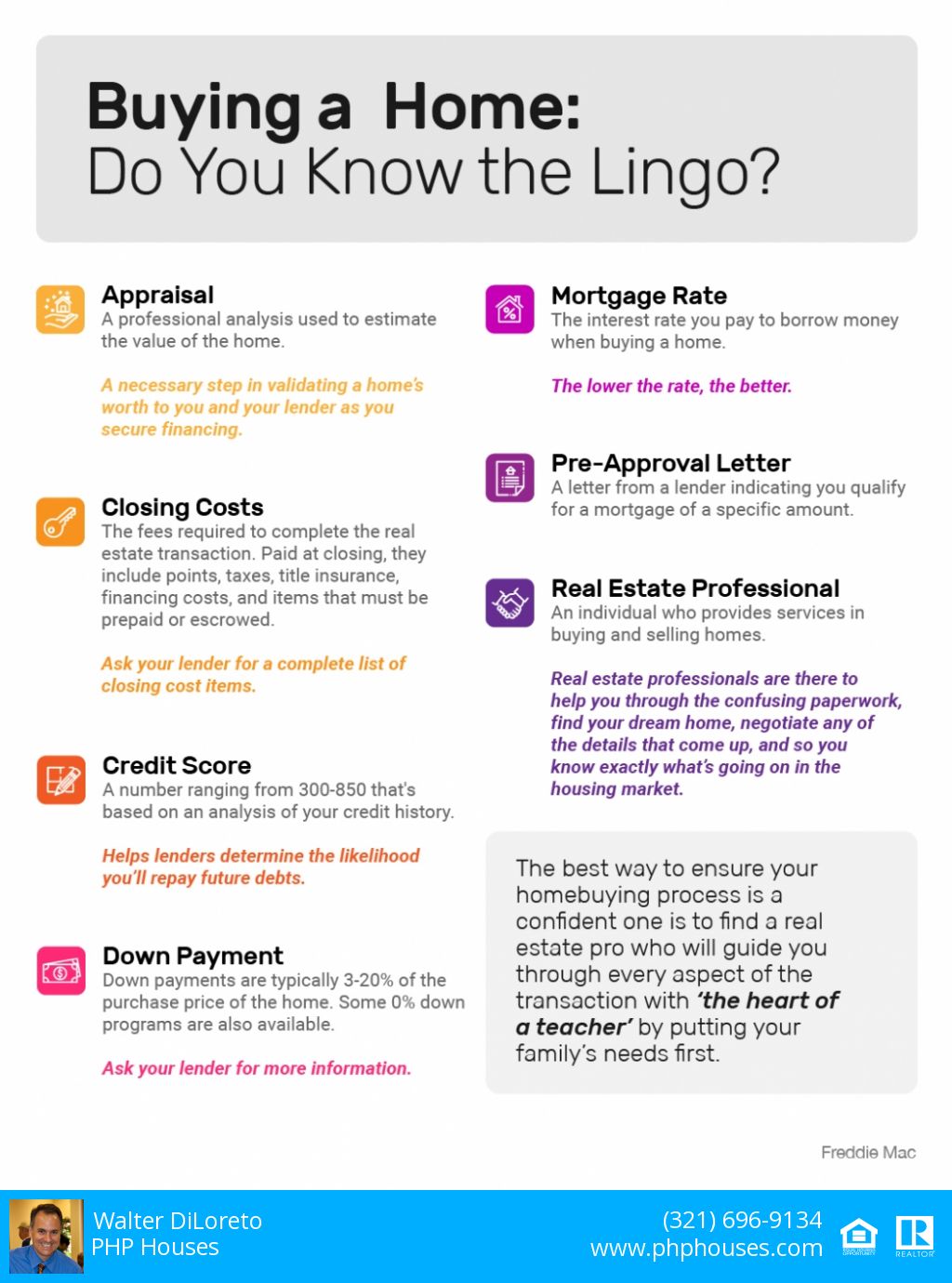

Buying a Home: Do You Know the Lingo?

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Homes priced in the top 25% of a price range for a particular area of the country are considered “premium homes.” At the start of last year, many of the more expensive homes listed for sale hadn’t seen as much interest, since much of the demand for housing over the past few years has come from first-time buyers looking for starter homes. It looks like buyer activity, however, is starting to show a shift in this segment.

According to the January Luxury Report from the Institute for Luxury Home Marketing (ILHM):

“In a snapshot of 2019, despite pessimism at the start of the year, the last quarter showcased a strengthening, with an upswing in the luxury market for sales in both the single family and condo markets.”

Momentum is growing, and those looking to enter the luxury market are poised for success in 2020 as well. With more inventory available at the upper-end, historically low interest rates, and increasing average wages, the stage is set for buyers with an interest in this tier to embrace the perfect move-up opportunity.

The report highlights the increase in buyer activity in this segment, resulting in growing sales toward the end of 2019:

“According to reports from many luxury real estate professionals, the significant increase in number of properties bought at the end of 2019 versus 2018 is reflective of an early 2019 holding pattern.

Many of early 2019’s prospective luxury buyers held off while waiting to see how prices would react to new tax regulations and other policy changes. Buyer confidence returned in late spring and compared to 2018, above average sales were reported in the final quarter of 2019.”

With evidence of strong buyer confidence, this is great news, as more homeowners are building equity and growing their net worth throughout the country:

“Many homeowners are now diversifying their wealth, owning several properties rather than a single mega mansion. In addition, there have been an increase number of home purchases taking place in smaller cities, reflecting the rising number of people relocating from major metropolises. Their property equity wealth or ability to pay high rental costs have afforded them the opportunity to purchase luxury properties in…secondary cities throughout North America.”

With a strong economy and a backdrop set for moving up this year, it’s a great time to explore the luxury market. Keep in mind, luxury can mean different things to different people, too. To one person, luxury is a secluded home with plenty of property and privacy. To another, it is a penthouse at the center of a bustling city. Knowing what characteristics mean luxury to you will help your agent understand what you’re after as you define the scope and location for the home of your dreams.

If you’re thinking about upgrading your current house to a luxury home, or adding an additional property to your portfolio, let’s get together to determine if you’re ready to make your move.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com