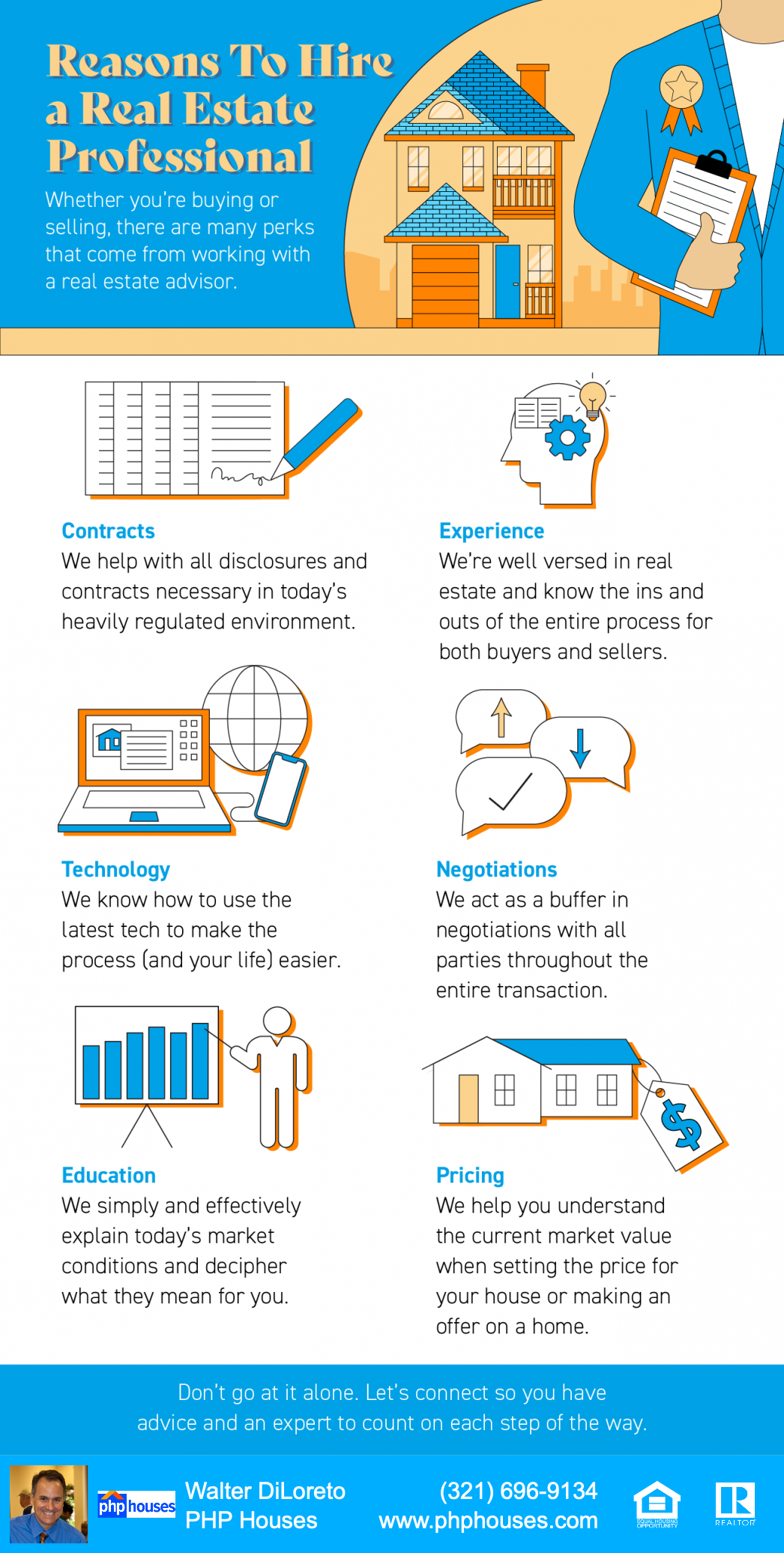

Work With a Real Estate Professional if You Want the Best Advice

Work With a Real Estate Professional if You Want the Best Advice

Because buying or selling a home is such a big decision in our lives, the need for clear, trustworthy information and guidance is crucial. And while no one can give you perfect advice, when you align yourself with an expert, you’ll get the best advice for your situation.

An Expert Will Give You the Best Advice Possible

Let’s say you need an attorney, so you seek out an expert in the type of law required for your case. When you go to their office, they won’t immediately tell you how the case is going to end or how the judge or jury will rule. What a good attorney can do, though, is discuss the most effective strategies you can take. They may recommend one or two approaches they believe will work well for your case.

Then, they’ll leave you to make the decision on which option you want to pursue. Once you decide, they can help you put a plan together based on the facts at hand. They’ll use their expert knowledge to work toward the resolution you want and make whatever modifications in the strategy necessary to try and achieve that outcome.

Similarly, the job of a trusted real estate professional is to give you the best advice for your situation. Just like you can’t find a lawyer to give you perfect advice, you won’t find a real estate professional who can either. They can’t because it’s impossible to know exactly what’s going to happen throughout your transaction. They also can’t predict exactly what will happen with conditions in today’s housing market.

But an expert real estate advisor is knowledgeable about market trends and the ins and outs of the homebuying and selling process. With that knowledge, they can anticipate what could happen based on your situation and help you put together a solid plan. And they’ll guide you through the process, helping you make decisions along the way.

That’s the very definition of getting the best – not perfect – advice. And that’s the power of working with an expert real estate advisor.

Bottom Line

If you want trustworthy advice when buying or selling a home, let’s connect so you have an expert real estate advisor on your side.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. The author does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. The author will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.