There are great advantages to owning a home, yet many people continue to rent. The financial benefits are just some of the reasons why homeownership has been a part of the long-standing American dream.

Realtor.com reported that:

“Buying remains the more attractive option in the long term – that remains the American dream, and it’s true in many markets where renting has become really the shortsighted option…as people get more savings in their pockets, buying becomes the better option.”

Why is owning a home financially better than renting?

Here are the top 5 financial benefits of homeownership:

Homeownership is a form of forced savings.

Homeownership provides tax savings.

Homeownership allows you to lock in your monthly housing cost.

Buying a home is less expensive than renting.

No other investment lets you live inside of it.

Studies have also shown that a homeowner’s net worth is 44x greater than that of a renter.

A family that purchased a median-priced home at the start of 2019 would build more than $37,750 in family wealth over the next five years with projected price appreciation alone.

Some argue that renting eliminates the cost of taxes and home repairs, but every potential renter must realize that all the expenses the landlord incurs are already baked into the rent payment – along with a profit margin!

Bottom Line

Owning a home has many social and financial benefits that cannot be achieved by renting. Let’s connect to determine if buying a home is your best move.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

Success is something often worth repeating, and Brent Sutherland, a Certified Financial Planner and Real Estate Investor, has certainly made his way in a momentum-driving direction. Here are 3 tips he shares from a recent piece in Business Insider on the benefits of owning real estate:

1. Real estate diversifies your income

“While it is certainly important to be properly diversified with your investments, it is even more important to be diversified with your income. This is because the largest financial risk for most of you is the loss of your primary source of income, which is typically in the form of a day job.”

The article highlights how having multiple sources of income, such as those derived from real estate investments, can eventually lead to relying less and less on a day job. Sound dreamy? It can be. When done well, real estate investments may eventually open up your time and the financial freedom to explore other things, like travel and other aspirations you may have for the future, particularly in the golden years of retirement.

2. Real estate produces near-immediate results

“You can achieve and feel the results almost immediately. Property improvements are visible and tangible. You can cash, spend, and invest rent payments. Today! Not 30 years in the future.”

Currently, home prices are appreciating in all price ranges, and just last weekCoreLogic announced their 12-month home value projection at 5.6%, an increase from 4.5% noted earlier this summer. With that in mind, real estate today is definitely driving immediate results!

3. Passive income can help you become financially independent sooner

“If you need $40,000 a year to live, you could alternatively invest in assets that generate an 8% cash-on-cash return. This is a very reasonable assumption. And it means you would only need to save a total of $500,000 (instead of $1 million). Yet, your investments would still meet your annual household living needs.

While returns, taxes, and inflation can, of course, affect your timeline, cash-flowing real-estate is a clear asset.”

Homeownership is a form of ‘forced savings.’ Every time you pay your mortgage, you’re contributing to your net worth by increasing the equity in your home, bringing you one step closer to true financial independence.

Bottom Line

If you want to increase your savings and overall net worth, real estate is a great way to go. To learn how you can make it happen, let’s get together to discuss the process.

Who is Brent Sutherland?

Sutherland was 35 when he bought his first single home to rent out for income, less than five years later, he owns eight additional properties and part of a commercial real estate project.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

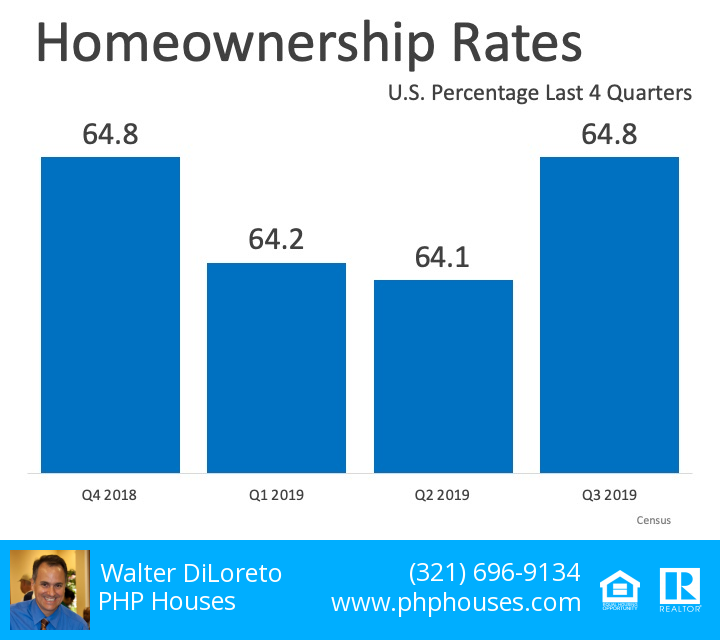

“The homeownership rate of 64.8 percent was not statistically different from the rate in the third quarter 2018 (64.4 percent), but was 0.7 percentage points higher than the rate in the second quarter 2019 (64.1 percent).”

Today there is still a lack of inventory, particularly at the entry and middle-level segments of the market, but that is not stopping buyers from making every effort to pursue homeownership. The many financial and non-financial benefits continue to drive the American Dream and will likely do so for generations to come.

Bottom Line

If you’re thinking of buying a home, let’s get together to make your dream a reality.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

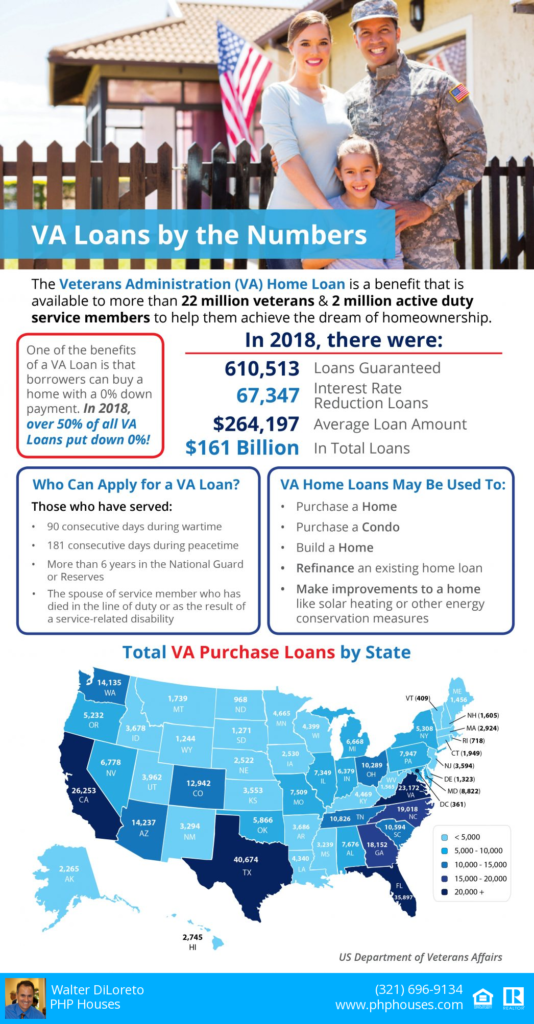

The Veterans Administration (VA) Home Loan is a benefit that is available to more than 22 million veterans and 2 million active duty service members to help them achieve the dream of homeownership.

In 2018, $161 billion was loaned to veterans and their families through the program.

In the same year, the average loan amount was $264,197 and 610,513 loans were guaranteed.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

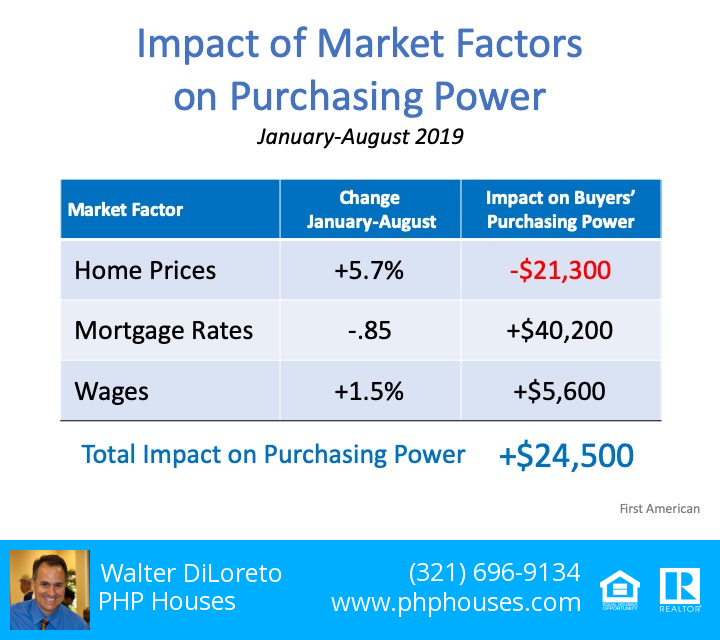

Home buying activity (demand) is up, and the number of available listings (supply) is down. When demand outpaces supply, prices appreciate. That’s why firms are beginning to increase their projections for home price appreciation going forward. As an example, CoreLogic increased their 12-month projection for home values from 4.5% to 5.6% over the last few months.

The reacceleration of home values will cause some to again voice concerns about affordability. Just last week, however, First American came out with a data analysis that explains how price is not the only market factor that impacts affordability. They studied prices, mortgage rates, and wages from January through August of this year. Here are their findings:

Home Prices

“In January 2019, a family with the median household income in the U.S. could afford to buy a $373,900 house. By August, that home had appreciated to $395,000, an increase of $21,100.”

Mortgage Interest Rates

“The 0.85 percentage point drop in mortgage rates from January 2019 through August 2019 increased affordability by 9.7%. That translates to a $40,200 improvement in house-buying power in just eight months.”

Wage Growth

“As rates have fallen in 2019, the economy has continued to perform well also, resulting in a tight labor market and wage growth. Wage growth pushes household incomes upward, which were 1.5% higher in August compared with January. The growth in household income increased consumer house-buying power by 1.5%, pushing house-buying power up an additional $5,600.”

When all three market factors are combined, purchasing power increasedby $24,500, thus making home buying more affordable, not less affordable. The table on top that simply shows the data.

Bottom Line

In the article, Mark Fleming, Chief Economist at First American, explained it best:

“Focusing on nominal house price changes alone as an indication of changing affordability, or even the relationship between nominal house price growth and income growth, overlooks what matters more to potential buyers – surging house-buying power driven by the dynamic duo of mortgage rates and income growth. And, we all know from experience, you buy what you can afford to pay per month.”

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

You’ve likely heard a ton about Millennials, but what about Gen Z? In the next 5 years, this generation will be between the ages of 23 and 28, and they’re eager to become homeowners faster than you may think.

According to realtor.com, “Nearly 80 percent of Generation Z members say they want to own a home before age 30,” and Concentrix Analytics said, “52% of prospective Gen Z buyers are already saving to buy a home.”

Wikipedia defines Generation Z (Gen Z) as “the demographic cohort after the Millennials. Demographers and researchers typically use the mid-1990s to mid-2000s as starting birth years.”

The report from Concentrix goes a little deeper on Gen Z, identifying the main reasons this cohort wants to own homes:

55% want to own a home because they want to start a family

47% want to build wealth over time

33% want to make their family proud

Although they’re eager to buy, this generation also perceives a few challenges ahead:

66% believe saving for a down payment and closing costs will be challenging

58% feel covering the monthly costs of owning may be difficult

52% perceive a lack of knowledge about where to start

It is also interesting to note that 21% of Gen Zers think their parents will provide financial help, 17% will use a down payment assistance program, and 15% believe other family members will help them. One of the highlights of the report mentioned,

“More than half of Gen Zers who think they’ll receive help also think they will need to pay their parents back, compared to 40 percent of millennials.”

Bottom Line

It is never too early to start saving for your own home, whether you are part of Gen Z or a different generation. If you would like to know where to start and how much you need to save to reach your goal of buying a home, let’s get together so you can better understand the process.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

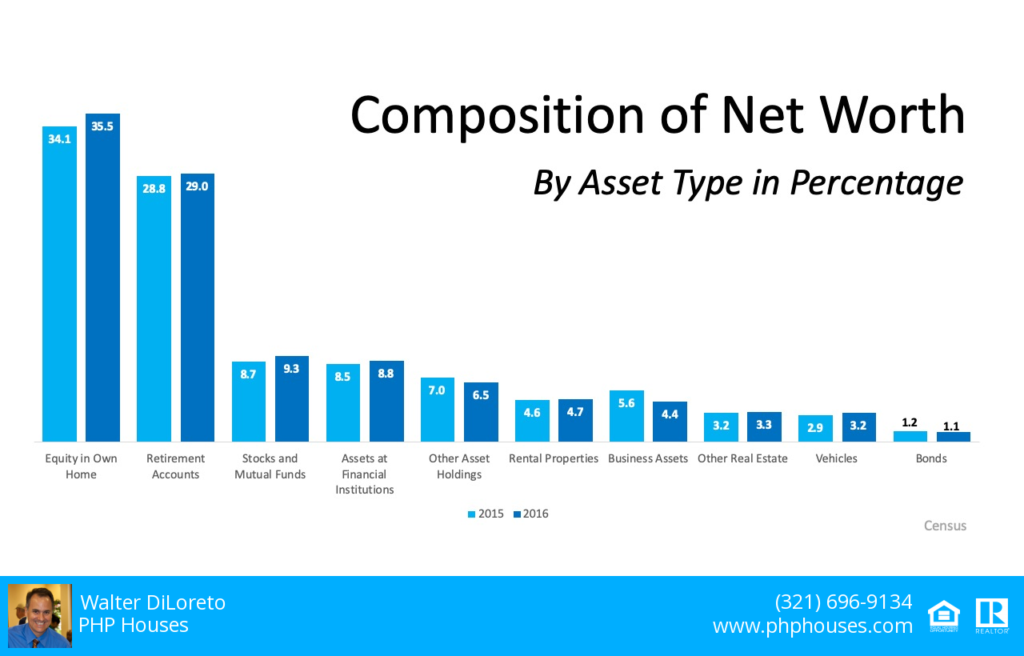

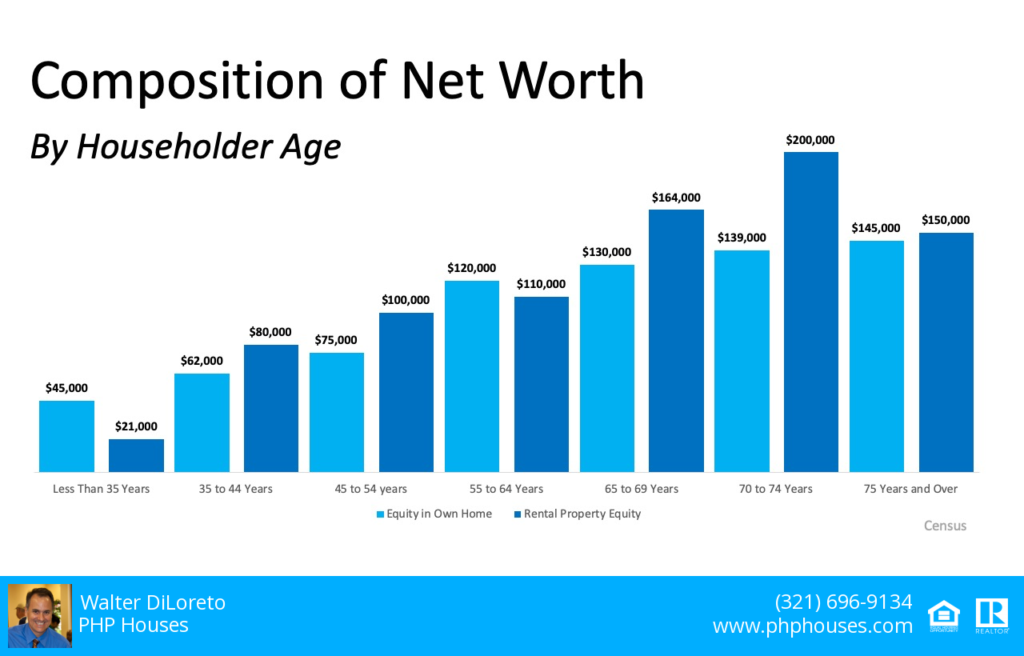

Many people plan to build their net worth by buying CDs or stocks, or just having a savings account. Recently, however, Economist Jonathan Eggleston and Survey Statistician Donald Hays, both of the U.S. Census Bureau,shared the biggest determinants of wealth,

“The biggest determinants of household wealth [are] owning a home and having a retirement account.” (Shown in the graph above).

This does not come as a surprise, as we often mention that homeownership can help you to increase your family’s wealth. This study reinforces that idea,

“Net worth is an important indicator of economic well-being and provides insights into a household’s economic health.”

Having equity in your home can help your family move in that direction, building toward substantial financial growth. According to the report noted above, people are not only creating net worth in the homes they live in, but many are also earning equity in rental property investments too. (See below):

“If you don’t own a home, buy one. If you own one home, buy another one, and if you own two homes buy a third and lend your relatives the money to buy a home.”

Bottom Line

There are financial and non-financial benefits to owning a home. If you would like to increase your net worth, let’s get together so you can learn all the benefits of becoming a homeowner.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

When people talk about homeownership and the American Dream, much of the conversation revolves around the financial benefits of owning a home. However, two recent studies show that the non-financial benefits might be even more valuable.

In a recent survey, Bank of America asked homeowners: “Does owning a home make you happier than renting?” 93% of the respondents answered yes, while only 7% said no. The survey also revealed:

More than 80% said they wouldn’t go back to renting

88% agreed that buying a home is the “best decision they have ever made”

79% believed owning a home has changed them for the better

Those surveyed talked about the “emotional equity” that is built through homeownership. The study says more than half of current homeowners define a home as a place to make memories, compared to 42% who view a home as a financial investment. Besides building wealth, the survey also showed that homeownership enhances quality of life:

67% of current homeowners believed their relationships with family and loved ones have changed for the better since they bought a home

78% are satisfied with the quality of their social life

82% of homeowners said they were satisfied with the amount of time they spend on their hobbies and passions since purchasing a home

75% of homeowners pursued new hobbies after buying a home

Homeowners seem to be very happy.

Renters Tell a Different Story…

According to the latest Zillow Housing Aspirations Report, 45% of renters regret renting rather than buying — more than five times the share of homeowners (8%) who regret buying instead of renting. Here are the four major reasons people regret renting, according to the report:

52% regret not being able to build equity

52% regret not being able to customize or improve their rentals

50% regret that the rent is so high

49% regret that they lack private outdoor space

These two studies prove that renting is just not the same as owning.

Bottom Line

There are both financial and non-financial benefits to homeownership. As good as the “financial equity” is, it doesn’t compare to the “emotional equity” gained through owning your own home.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, Fl 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

One of the benefits of homeownership is that it is a “forced savings plan.” Here’s how it works: You make a mortgage payment each month. Part of that payment is applied to the principal balance of your mortgage. Each month you owe less on the home. The difference between the value of the home and what you owe is called equity.

If your home has appreciated since the time you purchased it, that increase in value also raises your equity. Over time, the equity in your home could be substantial. Recently, CoreLogicrevealed that the average homeowner gained more than $65,000 in equity over the last 5 years.

Unlike last decade, homeowners are no longer foolishly tapping into that equity. In 2006-2008, many owners used their homes like an ATM by pulling equity out to purchase new cars, jet skis, or lavish vacations. They were pulling out cash (equity) from an appreciating asset, and then spending it on rapidly depreciating items. That is not happening anymore.

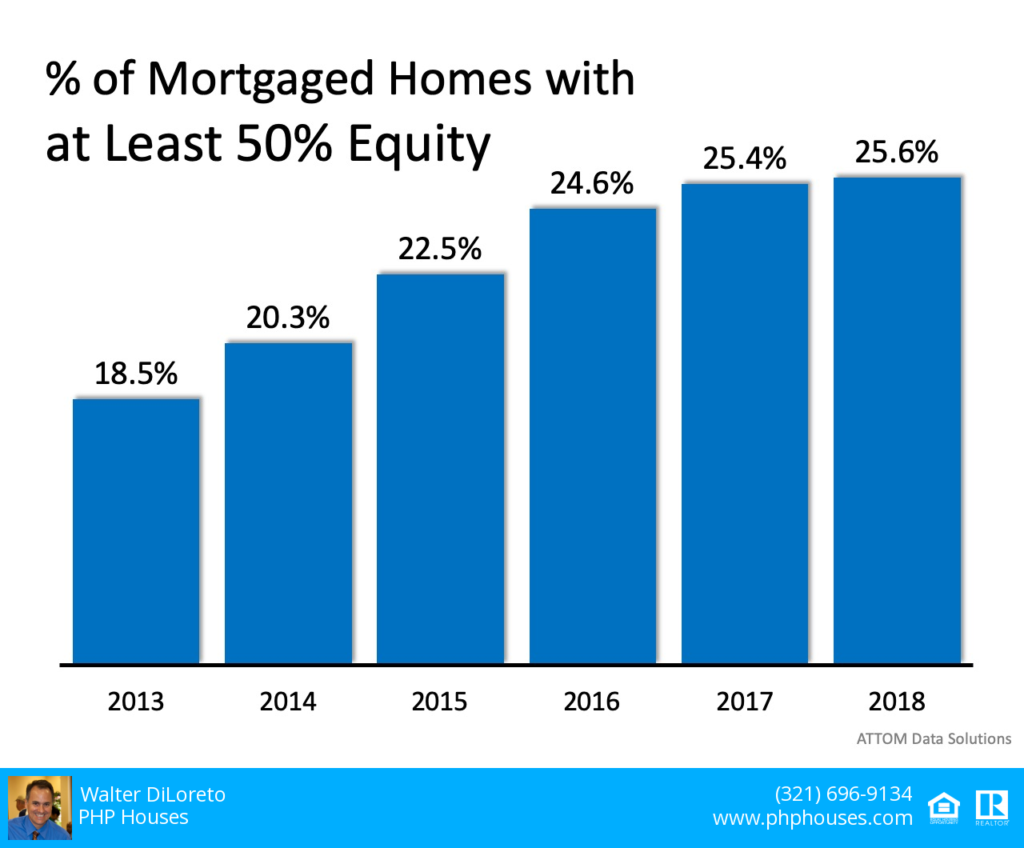

Over 50% of Homes Have at Least 50% Equity

The number of homeowners that currently have at least 50% equity in their home is astonishing. According to the Urban Institute, 37.1% of all homes in the country are mortgage-free. In a home equity study, ATTOM Data Solutions revealed that of the 62.9% of homes with a mortgage, 25.6% have at least 50% equity. That number has been increasing over the last five years.

By doing a little math, we can see that 53.2% of all homes in this country have at least 50% equity right now. Of all homes, 37.1% are mortgage-free and an additional 16.1% with a mortgage have at least 50% equity.

Bottom Line

Homeownership is different than renting. When you own, your housing expense (the mortgage payment) comes back to you in the form of equity in your home. That doesn’t happen with your rent payment. Your rent helps build your landlord’s equity instead.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com