Are Home Prices Continuing To Rise?

Are Home Prices Continuing To Rise?

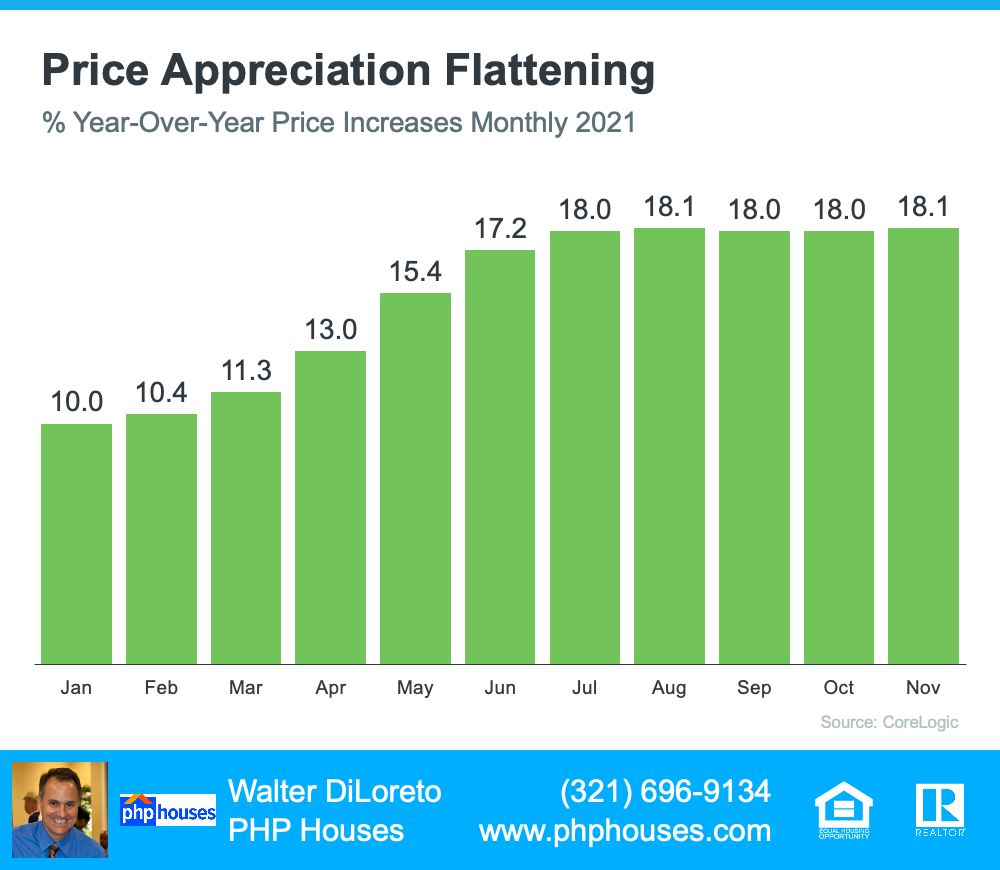

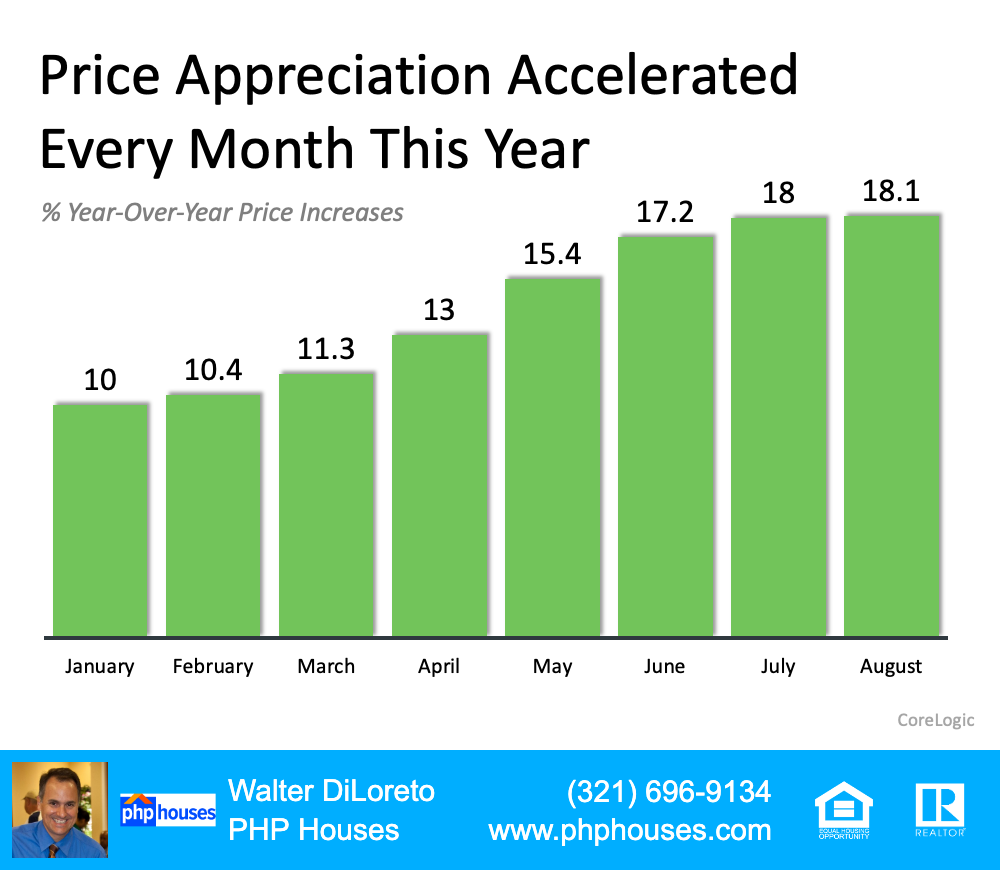

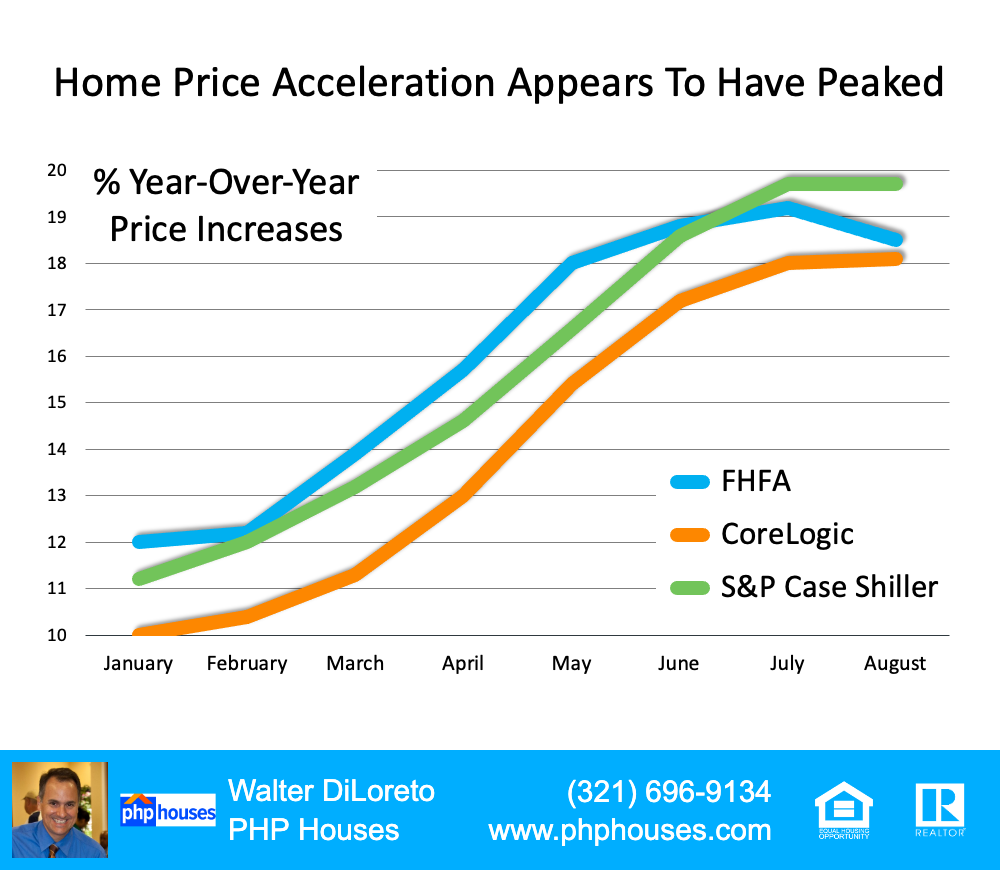

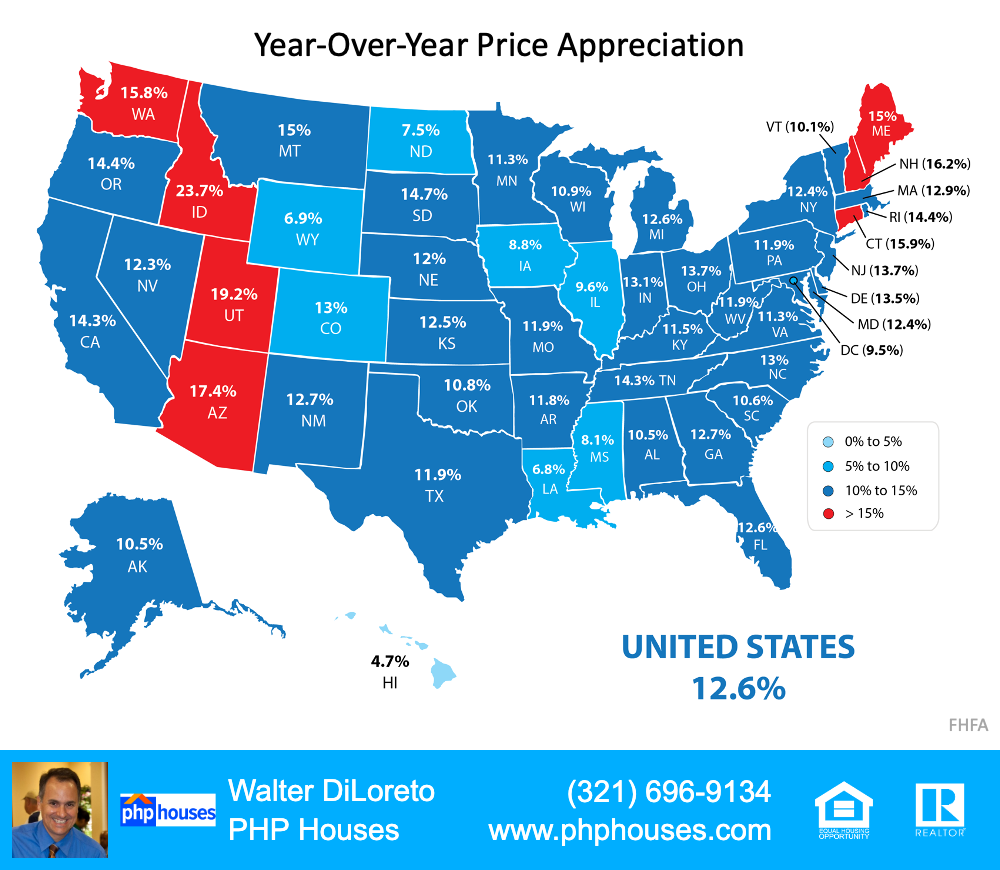

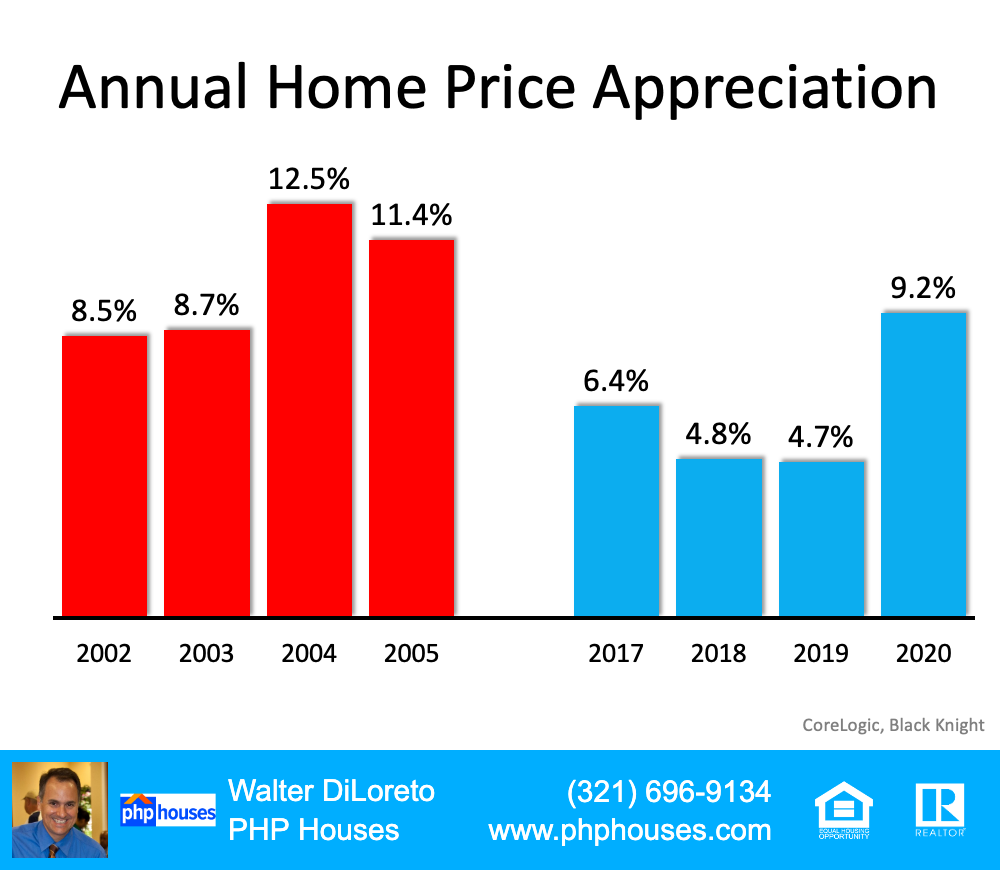

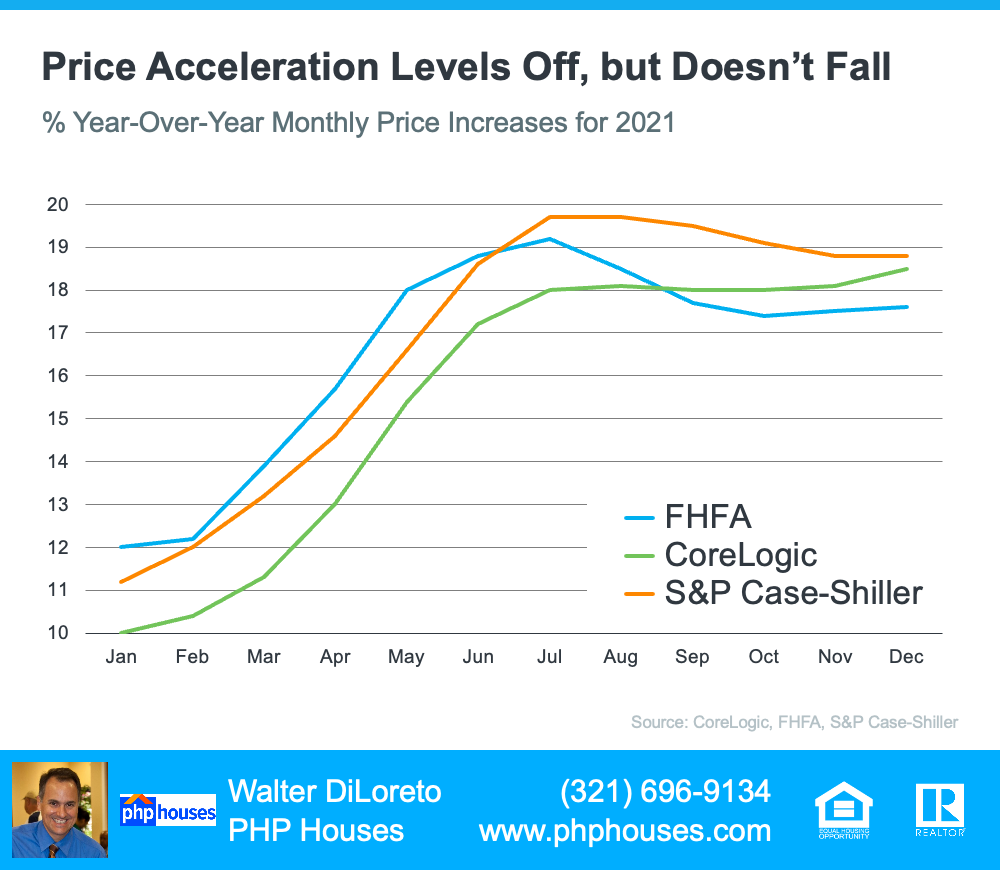

Many analysts projected home price appreciation would slow dramatically in the fall of 2021 and then continue to soften throughout 2022. So far, that hasn’t happened. The major price indices are all revealing ongoing double-digit price appreciation. Here’s a look at their reports on year-over-year price appreciation for December:

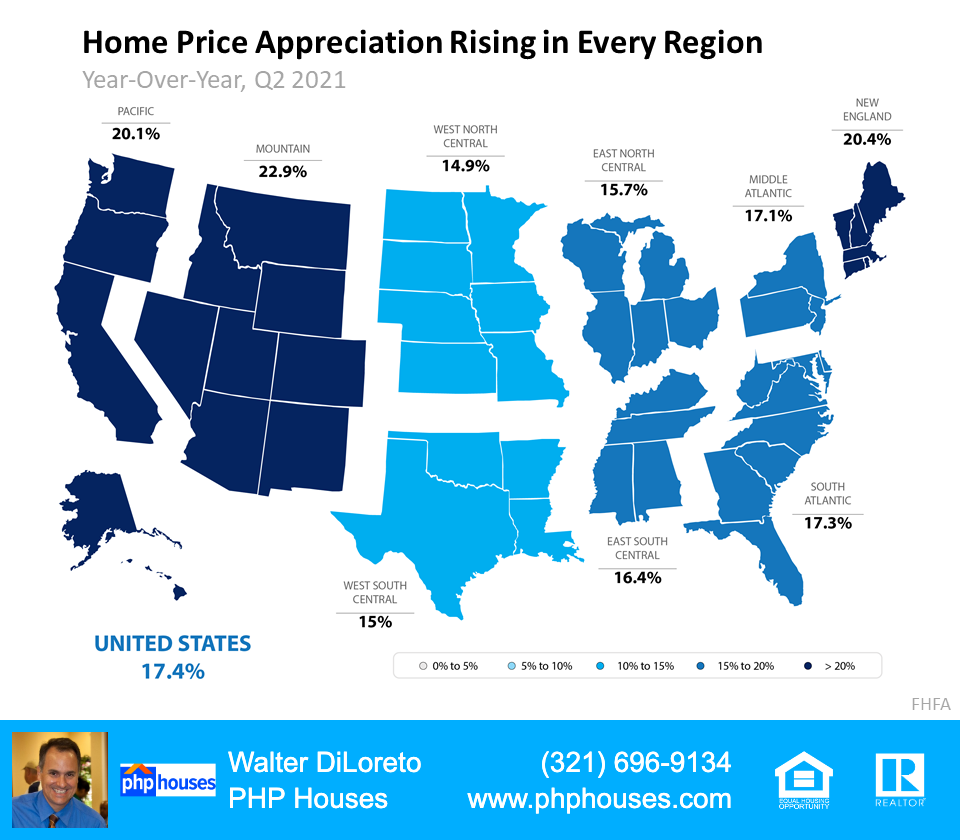

- Federal Housing Finance Agency (FHFA): 17.6%

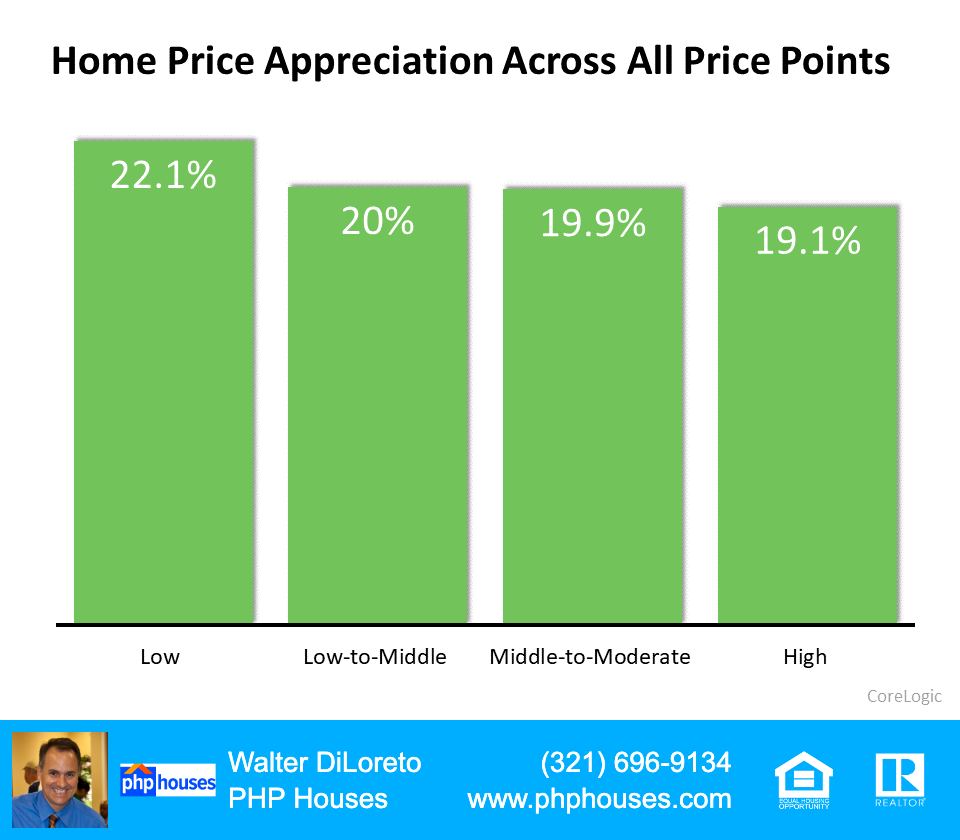

- S&P Case-Shiller: 18.8%

- CoreLogic: 18.5%

To show that they’re not seeing signs of softening, here’s a graph that gives the progression of all three indices for each month of 2021.

Price Acceleration Levels Off, but Doesn’t Fall

As the graph above reveals, last year, home price appreciation accelerated dramatically from January to July according to all three indices. Then, it began to decelerate in August when prices appreciated at a slower pace, but it didn’t decline. Many thought that would be the beginning of a rapid slowdown in the level of home price appreciation, but as the data shows, that wasn’t the case. Instead, prices began to level off for a few months before two of the three indices saw appreciation re-accelerate again in December.

To clarify, deceleration is not the same as depreciation. Acceleration means prices rise at a greater year-over-year pace than the previous month. Deceleration means home values continue to rise but at a slower pace of year-over-year appreciation. Depreciation means prices drop below current values. No one is forecasting that to happen.

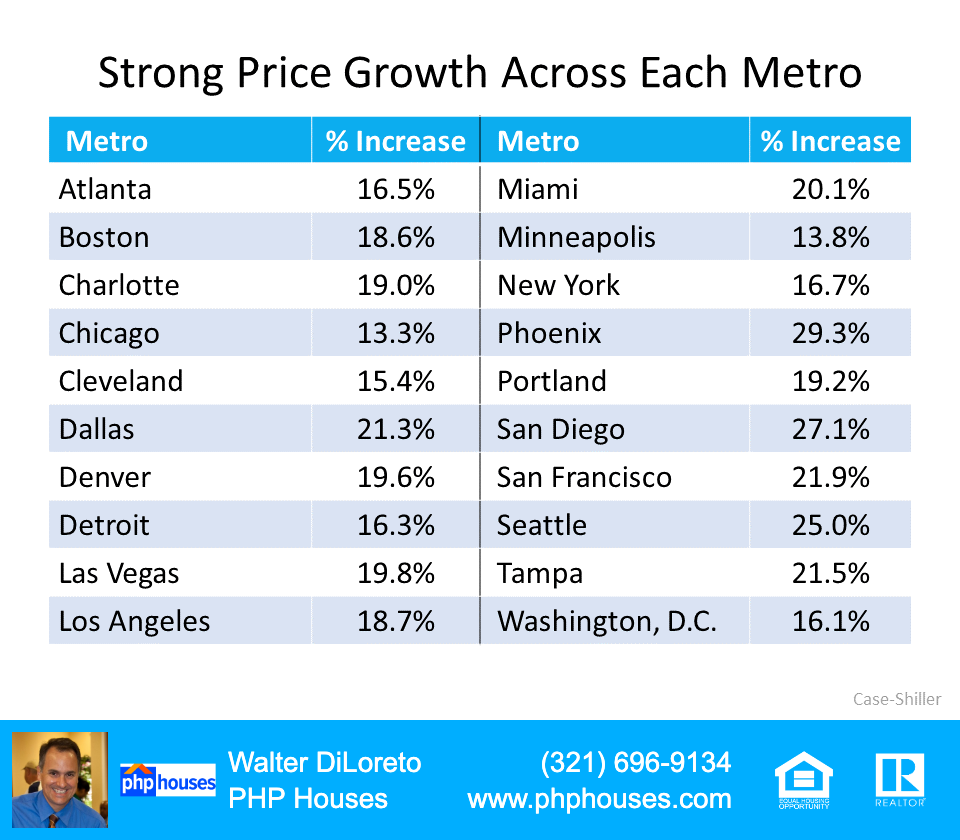

In fact, the FHFA revealed that price appreciation accelerated in December in six of the nine regions it tracks. Case Shillershowed that appreciation accelerated in 15 of the 20 metros they report on. As Selma Hepp, Deputy Chief Economist at CoreLogic, explains:

“After some signs of slowing home price growth . . . monthly price growth re-accelerated again, indicating home buyers have not yet thrown in the towel.”

What Does This Mean for You?

Whether you’re a first-time purchaser or someone looking to sell your current house and buy a home that better fits your needs, waiting to decide what to do will cost you in two ways:

- Mortgage rates are forecast to rise this year.

- Home prices should continue to appreciate at double-digit levels for some time.

If you wait, rising mortgage rates and high home price appreciation will have a dramatic impact on your monthly mortgage payment.

Bottom Line

Maybe the best thing to do is listen to the advice of Len Kiefer, Deputy Chief Economist at Freddie Mac:

“If you’re thinking about waiting until next year and that maybe rates are higher, but you’ll get a deal on prices – well that’s risky. It may be more advantageous to purchase this year relative to waiting until 2023 at this time.”

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. The author does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. The author will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.