THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

Young african woman holding home keys while hugging boyfriend in their new apartment after buying real estate. Lovely girl holding keys from new home and embracing man. Happy couple in their apartment around cardboard boxes.

When the number of buyers in the housing market outnumbers the number of homes for sale, it’s called a “seller’s market.” The advantage tips toward the seller as low inventory heats up the competition among those searching for a place to call their own. This can create multiple offer scenarios and bidding wars, making it tough for buyers to land their dream homes – unless they stand out from the crowd. Here are three reasons why pre-approval should be your first step in the homebuying process.

1. Gain a Competitive Advantage

Low inventory, like we have today, means homebuyers need every advantage they can get to make a strong impression and close the deal. One of the best ways to get one step ahead of other buyers is to get pre-approved for a mortgage before you make an offer. For one, it shows the sellers you’re serious about buying a home, which is always a plus in your corner.

2. Accelerate the Homebuying Process

Pre-approval can also speed up the homebuying process, so you can move faster when you’re ready to make an offer. In a competitive arena like we have today, being ready to put your best foot forward when the time comes may be the leg-up you need to cross the finish line first and land the home of your dreams.

3. Know What You Can Borrow and Afford

Here’s the other thing: if you’re pre-approved, you also have a better sense of your budget, what you can afford, and ultimately how much you’re eligible to borrow for your mortgage. This way, you’re less apt to fall in love with a home that may be out of your reach.

Freddie Mac sets out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”

Local real estate professionals also have relationships with lenders who can help you through this process, so partnering with a trusted advisor will be key for that introduction. Once you select a lender, you’ll need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac also describes the ‘4 Cs’ that help determine the amount you’ll be qualified to borrow:

Capacity: Your current and future ability to make your payments

Capital or Cash Reserves: The money, savings, and investments you have that can be sold quickly for cash

Collateral: The home, or type of home, that you would like to purchase

Credit: Your history of paying bills and other debts on time

While there are still many additional steps you’ll need to take in the homebuying process, it’s clear why pre-approval is always the best place to begin. It’s your chance to gain the competitive edge you may need if you’re serious about owning a home.

Bottom Line

Getting started with pre-approval is a great way to begin the homebuying journey. Let’s get together today to make sure you’re on the fastest path to homeownership.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

“Dark, spooky woods in the night with one solitary flashlight light. Purposefully dark for spooky, mysterious effect. Related:”

A considerable number of potential buyers shy away from the real estate market because they’re uncertain about the buying process – particularly when it comes to qualifying for a mortgage.

For many, the mortgage process can be scary, but it doesn’t have to be!

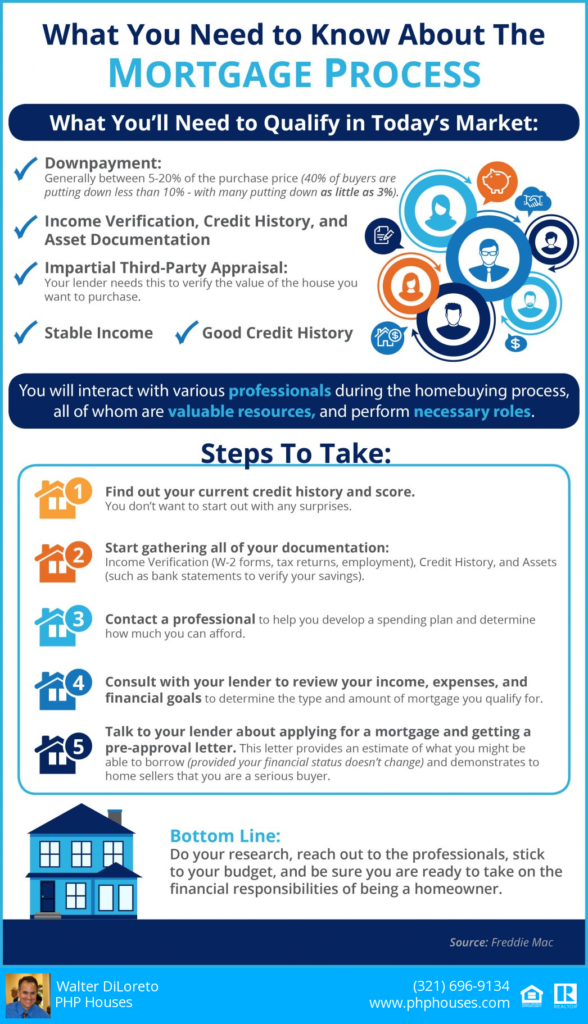

In order to qualify in today’s market, you’ll need a down payment (the average down payment on all loans last year was 5%, with many buyers putting down 3% or less), a stable income, and a good credit history.

Once you’re ready to apply, here are 5 easy steps Freddie Macsuggests to follow:

Find out your current credit history and credit score– Even if you don’t have perfect credit, you may already qualify for a loan. The average FICO Score® for all closed loans in September was 737, according to Ellie Mae.

Start gathering all of your documentation– This includes income verification (such as W-2 forms or tax returns), credit history, and assets (such as bank statements to verify your savings).

Contact a professional– Your real estate agent will be able to recommend a loan officer who can help you develop a spending plan, as well as help you determine how much home you can afford.

Consult with your lender– He or she will review your income, expenses, and financial goals in order to determine the type and amount of mortgage you qualify for.

Talk to your lender about pre-approval– A pre-approval letter provides an estimate of what you might be able to borrow (provided your financial status doesn’t change) and demonstrates to home sellers that you’re serious about buying.

Bottom Line

Do your research, reach out to professionals, stick to your budget, and be sure you’re ready to take on the financial responsibilities of becoming a homeowner.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

Congratulations! You’ve found a home to buy and have applied for a mortgage! You’re undoubtedly excited about the opportunity to decorate your new home, but before you make any large purchases, move your money around, or make any big-time life changes, consult your loan officer – someone who will be able to tell you how your decisions will impact your home loan.

Below is a list of Things You Shouldn’t Do After Applying for a Mortgage. Some may seem obvious, but some may not.

1. Don’t Change Jobs or the Way You Are Paid at Your Job. Your loan officer must be able to track the source and amount of your annual income. If possible, you’ll want to avoid changing from salary to commission or becoming self-employed during this time as well.

2. Don’t Deposit Cash into Your Bank Accounts. Lenders need to source your money, and cash is not really traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

3. Don’t Make Any Large Purchases Like a New Car or Furniture for Your New Home. New debt comes with it, including new monthly obligations. New obligations create new qualifications. People with new debt have higher debt to income ratios…higher ratios make for riskier loans…and sometimes qualified borrowers no longer qualify.

4. Don’t Co-Sign Other Loans for Anyone. When you co-sign, you are obligated. As we mentioned, with that obligation comes higher ratios as well. Even if you swear you will not be the one making the payments, your lender will have to count the payments against you.

5. Don’t Change Bank Accounts. Remember, lenders need to source and track assets. That task is significantly easier when there is consistency among your accounts. Before you even transfer any money, talk to your loan officer.

6. Don’t Apply for New Credit. It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be affected. Lower credit scores can determine your interest rate and maybe even your eligibility for approval.

7. Don’t Close Any Credit Accounts. Many clients erroneously believe that having less available credit makes them less risky and more likely to be approved. Wrong. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants in your score.

Bottom Line

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. The best advice is to fully disclose and discuss your plans with your loan officer before you do anything financial in nature. They are there to guide you through the process.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com