What Record-Low Housing Inventory Means for You

What Record-Low Housing Inventory Means for You

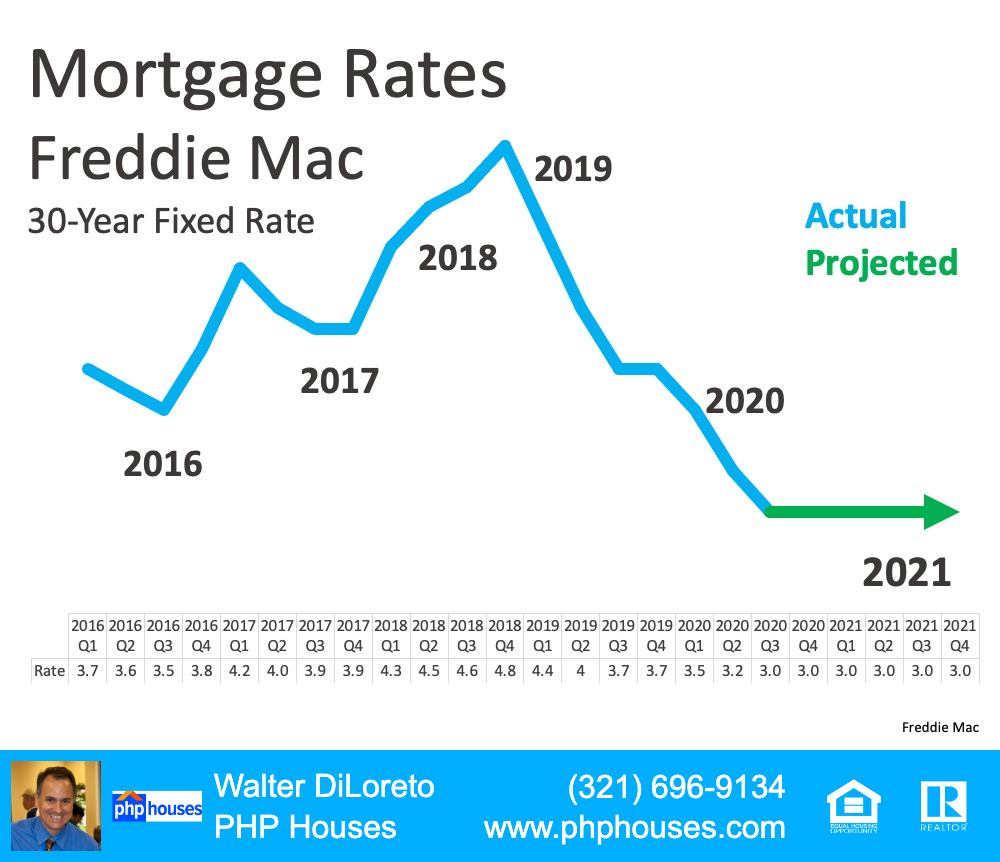

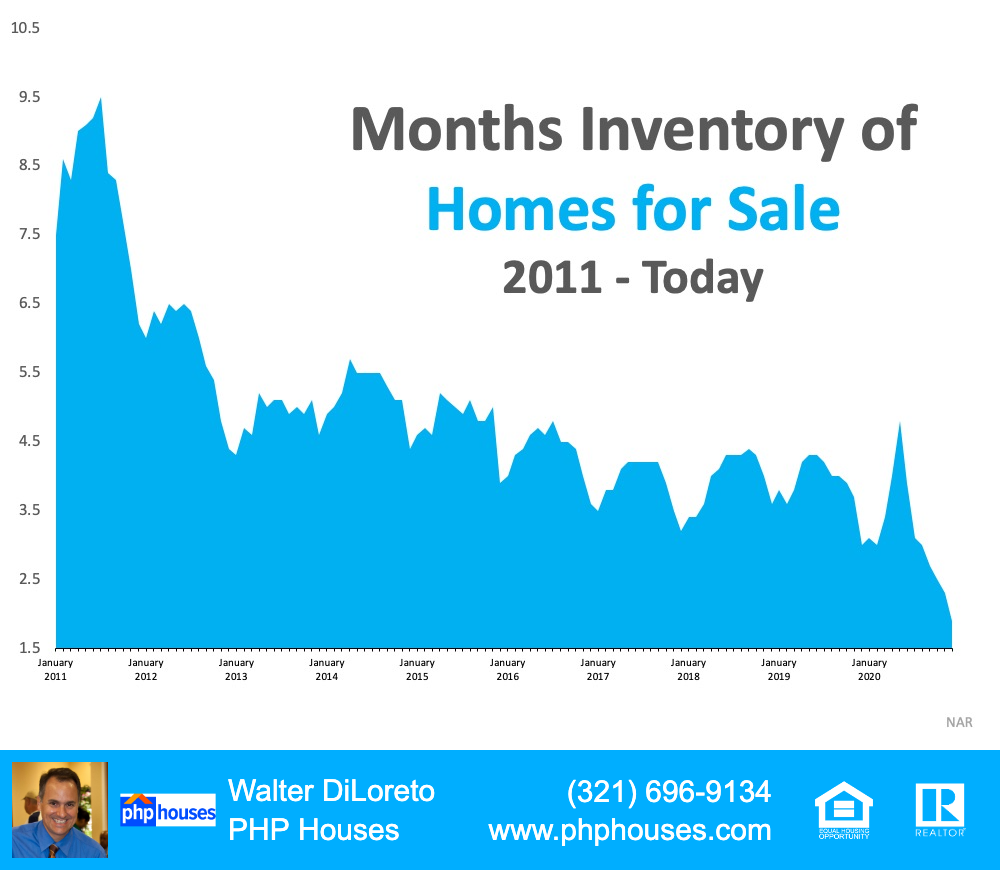

The real estate market is expected to do very well in 2021, with mortgage rates that are hovering at historic lows and forecasted by experts to remain favorable throughout the year. One challenge to the housing industry, however, is the lack of homes available for sale today. Last week, the National Association of Realtors (NAR) released their Existing Home Sales Report, which shows that the inventory of homes for sale is currently at an all-time low. The report explains:

“Total housing inventory at the end of December totaled 1.07 million units, down 16.4% from November and down 23% from one year ago (1.39 million). Unsold inventory sits at an all-time low 1.9-month supply at the current sales pace, down from 2.3 months in November and down from the 3.0-month figure recorded in December 2019. NAR first began tracking the single-family home supply in 1982.”

(See graph below):

Months Inventory of Homes for Sale

What Does This Mean for You?

If You’re a Buyer:

Be patient during your home search. It may take time to find a home you love. Once you do, however, be ready to move forward quickly. Get pre-approved for a mortgage, be prepared to make a competitive offer from the start, and know that a shortage in inventory could mean you’ll enter a bidding war. Calculate just how far you’re willing to go to secure a home and lean on your real estate professional as an expert guide along the way. The good news is, more inventory is likely headed to the market soon, Lawrence Yun, Chief Economist at NAR, notes:

“To their credit, homebuilders and construction companies have increased efforts to build, with housing starts hitting an annual rate of near 1.7 million in December, with more focus on single-family homes…However, it will take vigorous new home construction in 2021 and in 2022 to adequately furnish the market to properly meet the demand.”

If You’re a Seller:

Realize that, in some ways, you’re in the driver’s seat. When there’s a shortage of an item at the same time there’s a strong demand for it, the seller is in a good position to negotiate the best possible terms. Whether it’s the price, moving date, possible repairs, or anything else, you’ll be able to request more from a potential purchaser at a time like this – especially if you have multiple interested buyers. Don’t be unreasonable, but understand you probably have the upper hand.

Bottom Line

The housing market will remain strong throughout 2021. Know what that means for you, whether you’re buying, selling, or doing both.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram