Is Homeownership Still the American Dream?

Is Homeownership Still the American Dream?

Defining the American dream is personal, and no one individual will have the same definition as another. But the feelings it brings about – success, freedom, and a sense of prosperity – are universal. That’s why, for many people, homeownership remains a key part of the American dream. Your home is your stake in the community, a strong financial investment, and an achievement to be proud of.

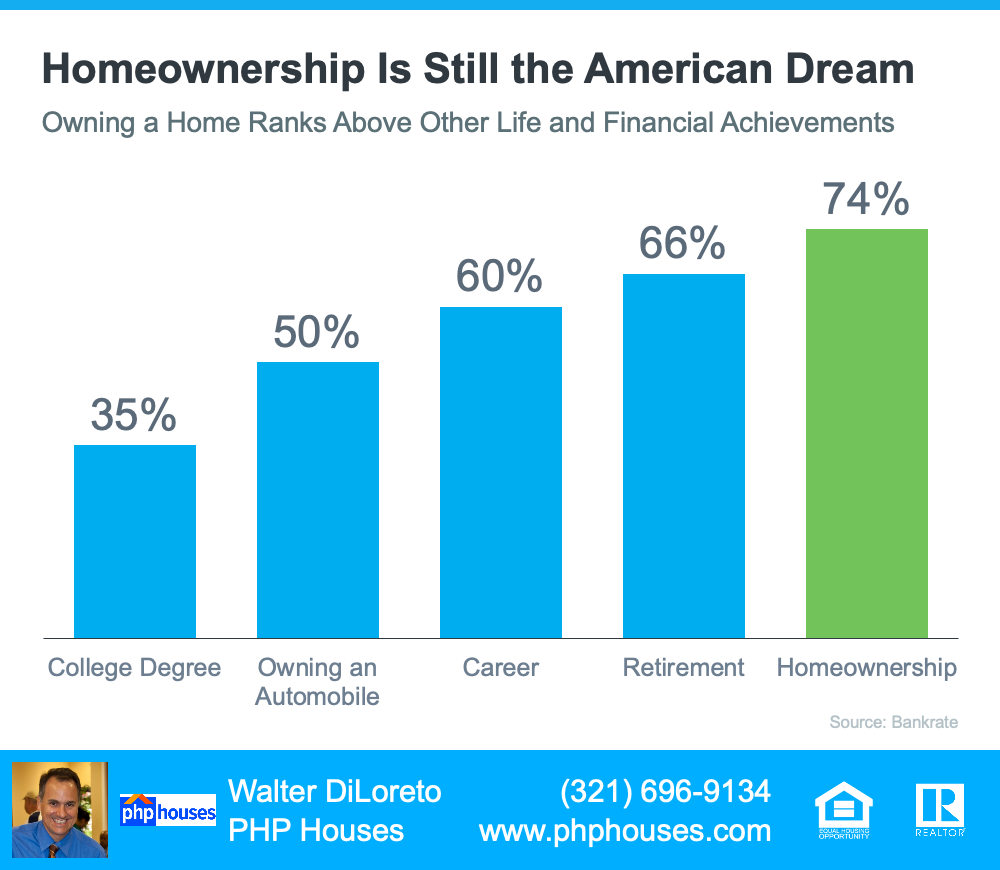

A recent survey from Bankrate asked respondents to rank achievements as indicators of financial success, and the responses prove that owning a home is still important to so many Americans today (see graph below):

Homeownership Is Still the American Dream

As the graph shows, homeownership ranks above other significant milestones, including retirement, having a successful career, and earning a college degree.

That could be because owning a home is a significant wealth-building tool and provides meaningful financial stability. The National Association of Realtors (NAR) explains:

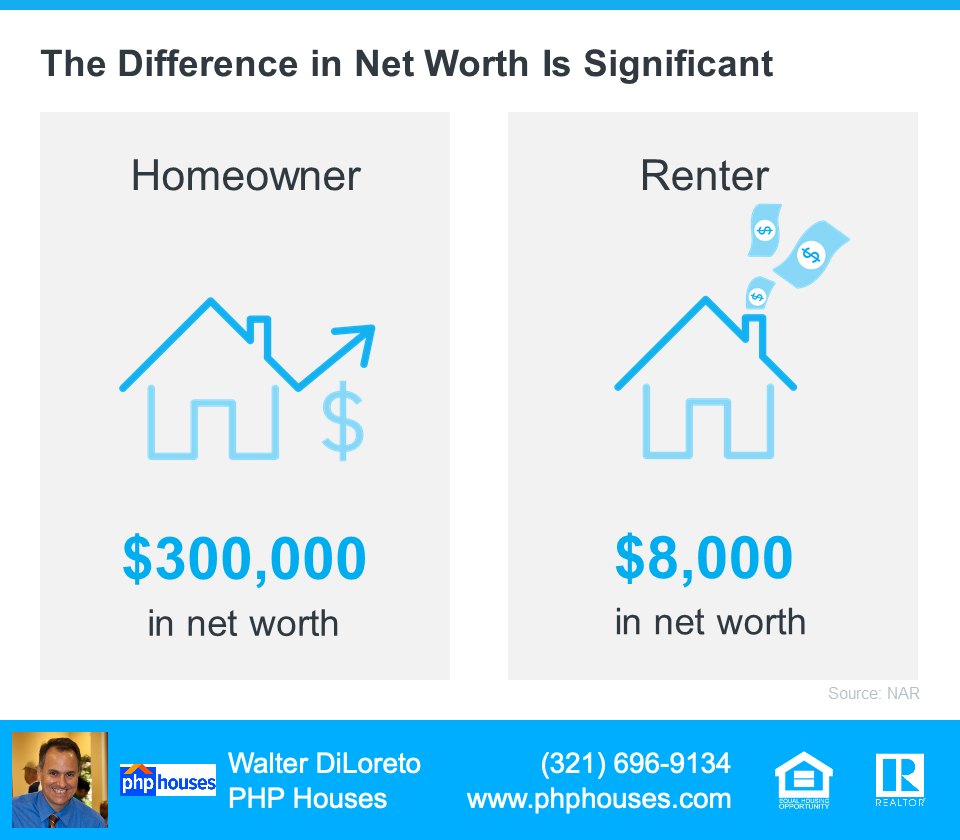

“Homeownership builds financial security. With 65.5% of Americans owning homes, the net worth of a typical homeowner is nearly 40 times the net worth of a non-owner.”

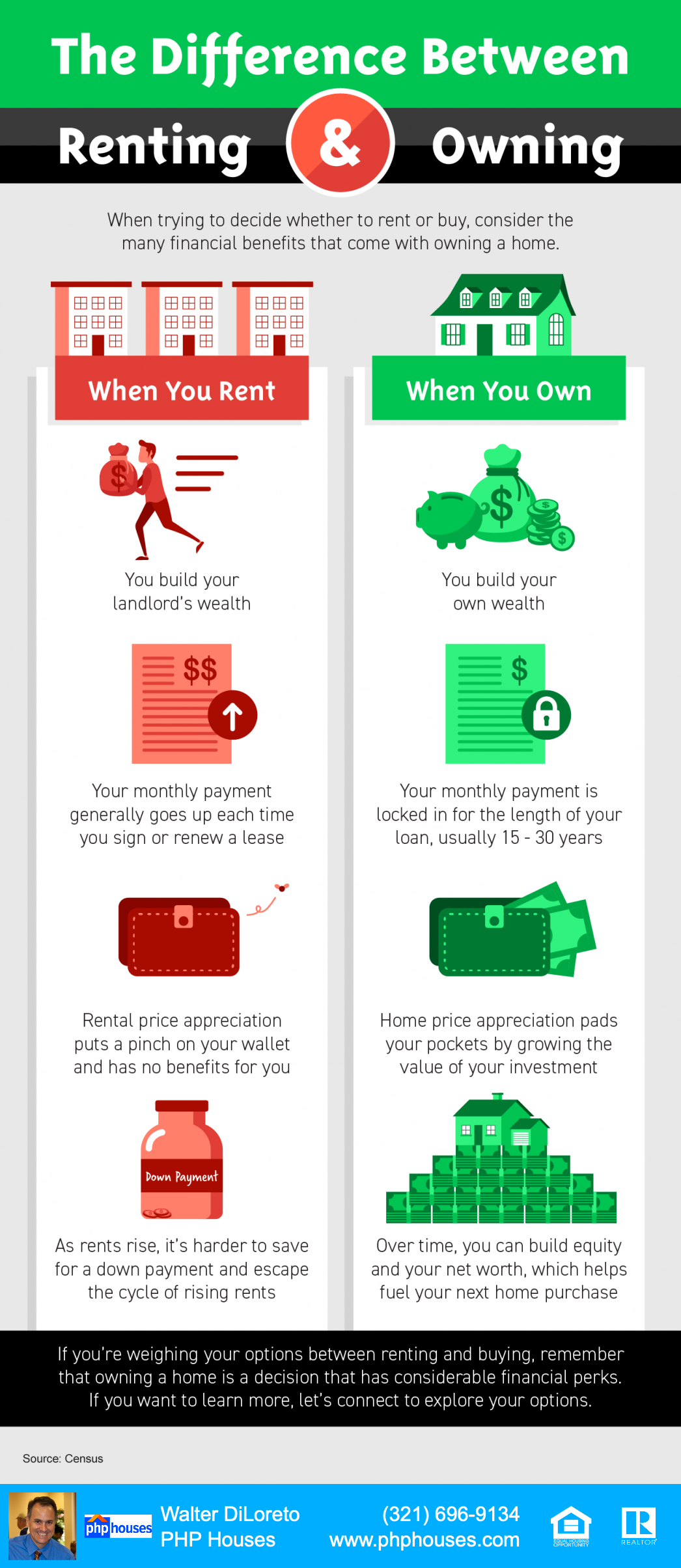

There are other ways your home acts as more than just a roof over your head, too. The Mortgage Reports highlights a few of the many benefits homeowners enjoy, including:

- Your equity (and wealth) grows through home price appreciation.

- Your housing costs are fixed – and that can help combat rising costs from inflation.

- You’ll have greater privacy and the opportunity to customize your living space.

Plus, homeowners tend to be more active in their community. Like NAR says:

“Living in one place for a longer amount of time creates and [sic] obvious sense of community pride, which may lead to more investment in said community.”

What Does That Mean for You?

If your definition of the American Dream involves greater freedom and prosperity, then homeownership could play a major role in helping you achieve that dream. When you set out to buy, know there are incredible benefits waiting for you at the end of your journey. You’ll have a place you can call your own, feel most comfortable, and grow your wealth.

First American puts it best, saying:

“Homeownership remains central to the pursuit of the American Dream. It is a critical driver of economic mobility, delivering financial and social advantages. . . .”

Bottom Line

Buying a home is a powerful decision and a key part of the American Dream. And if homeownership is part of your personal dreams this year, let’s connect and start the process today.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. The author does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. The author will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.