Choosing the right real estate professional is one of the most impactful decisions you can make in your home buying or selling process.

A real estate professional can explain current market conditions and break down what they will mean to you and your family.

If you’re considering buying or selling a home in 2020, make sure to work with someone who has the experience to answer all of your questions about pricing, contracts, and negotiations.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

Saving to buy a house or home savings concept with money coin stack growing.Saving money concept.

The gap between the increase in personal income and residential real estate prices has been used to defend the concept that we are experiencing an affordability crisis in housing today.

It is true that home prices and wages are two key elements in any affordability equation. There is, however, an extremely important third component to that equation: mortgage interest rates.

Mortgage interest rates have fallen by more than a full percentage point from this time last year. Today’s rate is 3.75%; it was 4.86% at this time last year. This has dramatically increased a purchaser’s ability to afford a home.

Here are three reports validating that purchasing a home is in fact more affordable today than it was a year ago:

“Falling mortgage rates and slower home-price growth mean that many buyers this year are committing to lower mortgage payments than they would have faced for the same home last year. After rising at a double-digit annual pace in 2018, the principal-and-interest payment on the nation’s median-priced home – what we call the “typical mortgage payment”– fell year-over-year again.”

“At the national level, housing affordability is up from last month and up from a year ago…All four regions saw an increase in affordability from a year ago…Payment as a percentage of income was down from a year ago.”

“In 2019, the dynamic duo of lower mortgage rates and rising incomes overcame the negative impact of rising house price appreciation on affordability. Indeed, affordability reached its highest point since January 2018. Focusing on nominal house price changes alone as an indication of changing affordability, or even the relationship between nominal house price growth and income growth, overlooks what matters more to potential buyers – surging house-buying power driven by the dynamic duo of mortgage rates and income growth. And, we all know from experience, you buy what you can afford to pay per month.”

Bottom Line

Though the price of homes may still be rising, the cost of purchasing a home is actually falling. If you’re thinking of buying your first home or moving up to your dream home, let’s connect so you can better understand the difference between the two.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

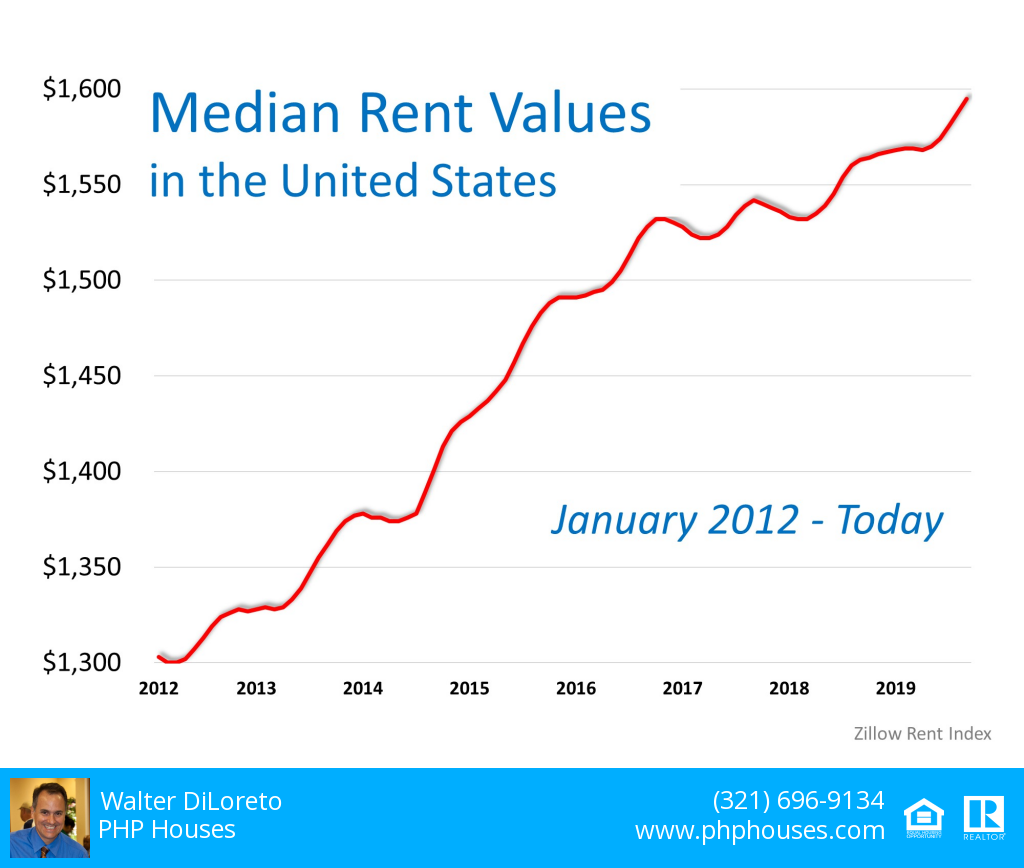

Much has been written about how residential real estate values have increased since the housing market started its recovery in 2012. However, little has been shared about what has taken place with residential rental prices. Let’s shed a little light on this subject.

In the most recent Apartment Rent Report, RentCafe explains how rents have continued to increase over the last twelve months because of a large demand and a limited supply.

“Continued interest in rental apartments and slowing construction keeps the national average rent on a strong upward trend.”

Zillow, in its latest Rent Index, agreed that rents are continuing on an “upward trend” across most of the country, and that the trend is accelerating:

“The median U.S. rent grew 2% year-over-year, to $1,595 per month. National rent growth is faster than a year ago, and while 46 of the 50 largest markets are showing deceleration in annual home value growth, annual rent growth is accelerating in 41 of the largest 50 markets.”

The Zillow report went on to detail rent increases since the beginning of the housing market recovery in 2012. Here is a graph showing the increases:

Bottom Line

It is true that home prices have risen over the past seven years, increasing the cost of owning a home. However, the cost of renting a home has also increased over that same time period.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

No one knows for sure when the next recession will occur. What is known, however, is that the upcoming economic slowdown will not be caused by a housing market crash, as was the case in 2008. There are those who disagree and are comparing today’s real estate market to the market in 2005-2006, which preceded the crash. In many ways, however, the market is very different now. Here are three suppositions being put forward by some, and why they don’t hold up.

SUPPOSITION #1

A critical warning sign last time was the surging gap between the growth in home prices and household income. Today, home values have also outpaced wage gains. As in 2006, a lack of affordability will kill the market.

Counterpoint

The “gap” between wages and home price growth has existed since 2012. If that is a sign of a recession, why didn’t we have one sometime in the last seven years? Also, a buyer’s purchasing power is MUCH GREATER today than it was thirteen years ago. The equation to determine affordability has three elements: home prices, wages, AND MORTGAGE INTEREST RATES. Today, the mortgage rate is about 3.5% versus 6.41% in 2006.

SUPPOSITION #2

In 2018, as in 2005, housing-price growth began slowing, with significant price drops occurring in some major markets. Look at Manhattan where home prices are in a “near free-fall.”

Counterpoint

The only major market showing true depreciation is Seattle, and it looks like home values in that city are about to reverse and start appreciating again. CoreLogic is projecting home price appreciation to reaccelerate across the country over the next twelve months.

Regarding Manhattan, home prices are dropping because the city’s new “mansion tax” is sapping demand. Additionally, the new federal tax code that went into effect last year continues to impact the market, capping deductions for state and local taxes, known as SALT, at $10,000. That had the effect of making it more expensive to own homes in states like New York.

SUPPOSITION#3

Prices will crash because that is what happened during the last recession.

Counterpoint

It is true that home values sank by almost 20% during the 2008 recession. However, it is also true that in the four previous recessions, home values depreciated only once (by less than 2%). In the other three, residential real estate values increased by 3.5%, 6.1%, and 6.6%.

Price is determined by supply and demand. In 2008, there was an overabundance of housing inventory (a 9-month supply). Today, housing inventory is less than half of that (a 4-month supply).

Bottom Line

We need to realize that today’s real estate market is nothing like the 2008 market. Therefore, when a recession occurs, it won’t resemble the last one.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

You’ve likely heard a ton about Millennials, but what about Gen Z? In the next 5 years, this generation will be between the ages of 23 and 28, and they’re eager to become homeowners faster than you may think.

According to realtor.com, “Nearly 80 percent of Generation Z members say they want to own a home before age 30,” and Concentrix Analytics said, “52% of prospective Gen Z buyers are already saving to buy a home.”

Wikipedia defines Generation Z (Gen Z) as “the demographic cohort after the Millennials. Demographers and researchers typically use the mid-1990s to mid-2000s as starting birth years.”

The report from Concentrix goes a little deeper on Gen Z, identifying the main reasons this cohort wants to own homes:

55% want to own a home because they want to start a family

47% want to build wealth over time

33% want to make their family proud

Although they’re eager to buy, this generation also perceives a few challenges ahead:

66% believe saving for a down payment and closing costs will be challenging

58% feel covering the monthly costs of owning may be difficult

52% perceive a lack of knowledge about where to start

It is also interesting to note that 21% of Gen Zers think their parents will provide financial help, 17% will use a down payment assistance program, and 15% believe other family members will help them. One of the highlights of the report mentioned,

“More than half of Gen Zers who think they’ll receive help also think they will need to pay their parents back, compared to 40 percent of millennials.”

Bottom Line

It is never too early to start saving for your own home, whether you are part of Gen Z or a different generation. If you would like to know where to start and how much you need to save to reach your goal of buying a home, let’s get together so you can better understand the process.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

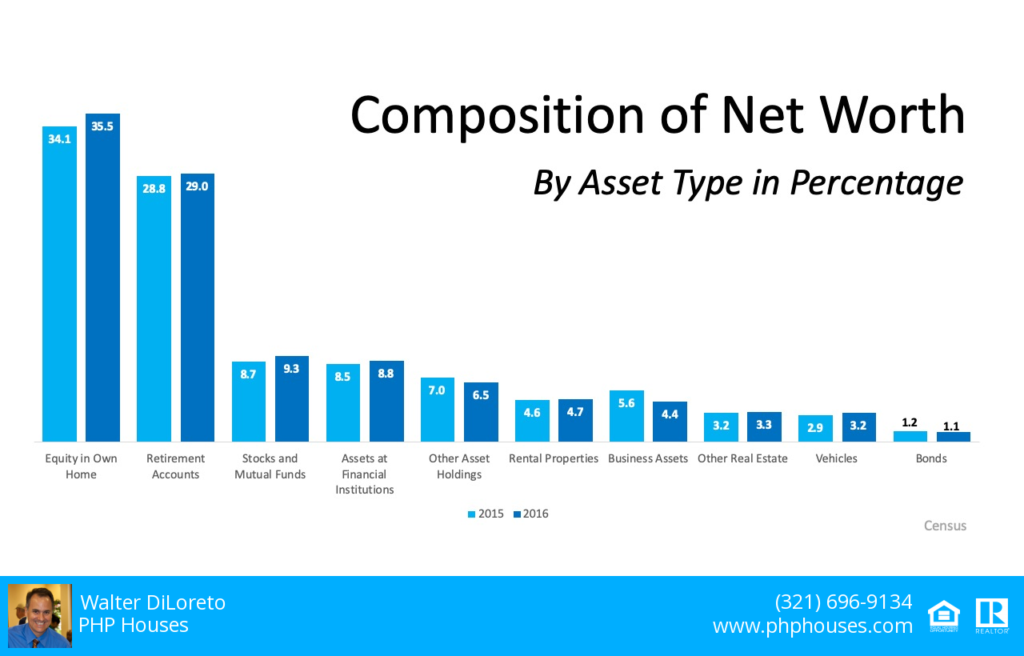

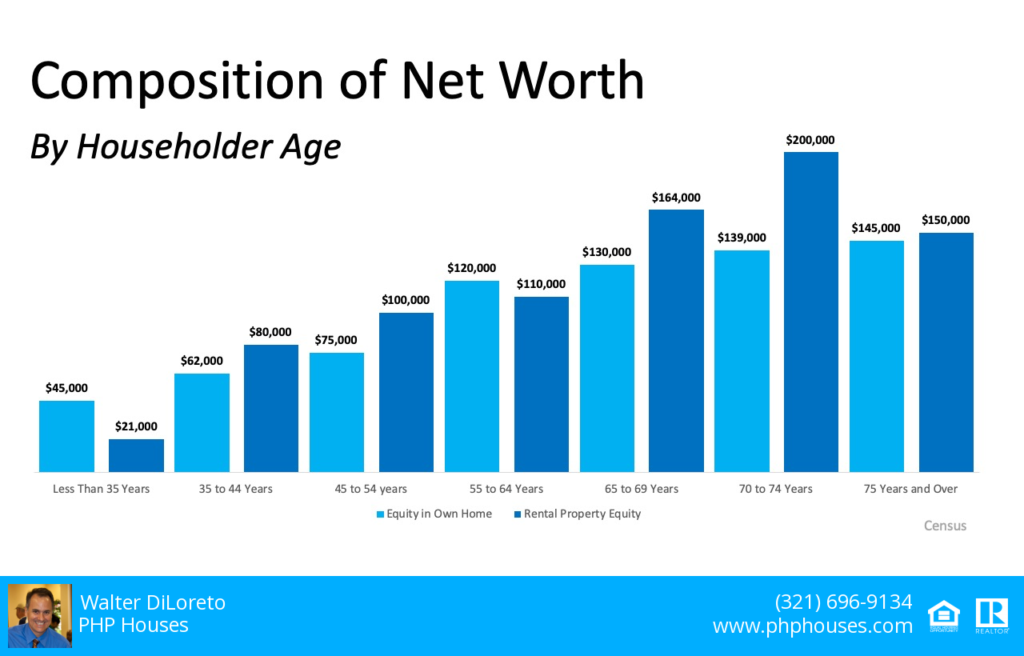

Many people plan to build their net worth by buying CDs or stocks, or just having a savings account. Recently, however, Economist Jonathan Eggleston and Survey Statistician Donald Hays, both of the U.S. Census Bureau,shared the biggest determinants of wealth,

“The biggest determinants of household wealth [are] owning a home and having a retirement account.” (Shown in the graph above).

This does not come as a surprise, as we often mention that homeownership can help you to increase your family’s wealth. This study reinforces that idea,

“Net worth is an important indicator of economic well-being and provides insights into a household’s economic health.”

Having equity in your home can help your family move in that direction, building toward substantial financial growth. According to the report noted above, people are not only creating net worth in the homes they live in, but many are also earning equity in rental property investments too. (See below):

“If you don’t own a home, buy one. If you own one home, buy another one, and if you own two homes buy a third and lend your relatives the money to buy a home.”

Bottom Line

There are financial and non-financial benefits to owning a home. If you would like to increase your net worth, let’s get together so you can learn all the benefits of becoming a homeowner.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com

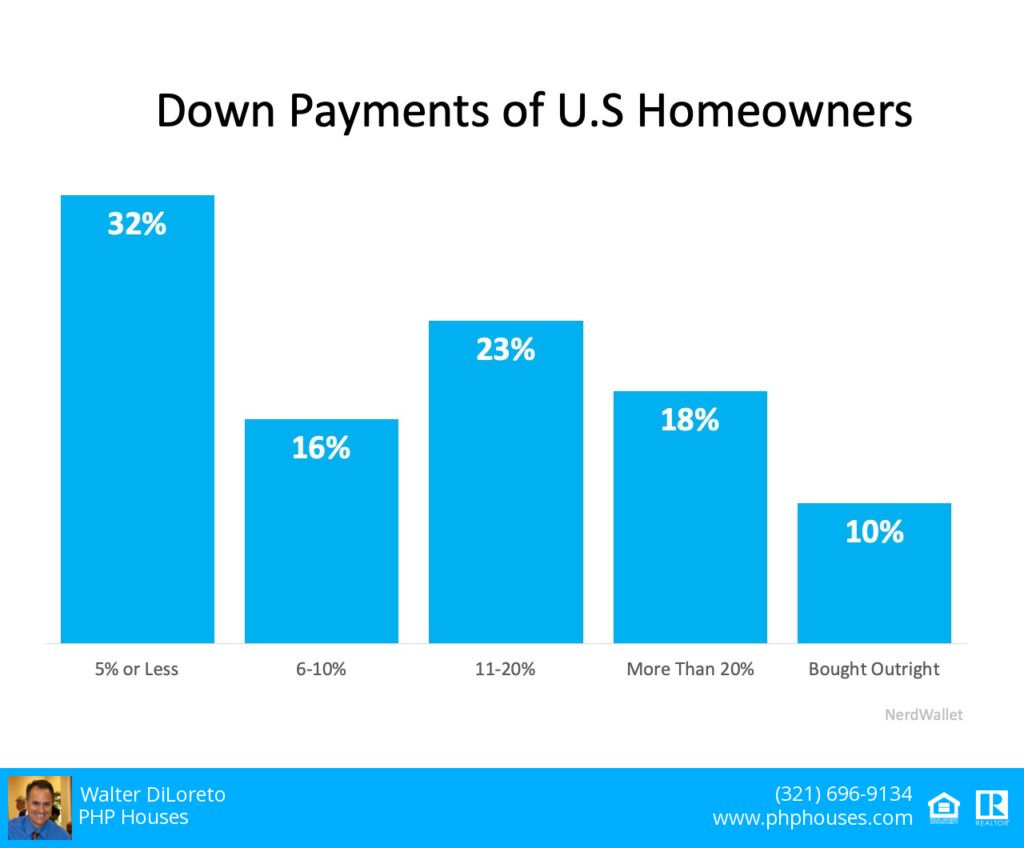

According to the ‘2019 Home Buyer Report’ conducted by Nerdwallet, many first-time buyers still believe they need a 20% down payment to buy a home in today’s market:

“More than 6 in 10 (62%) Americans believe you must put at least 20% down in order to purchase a home.”

When potential homebuyers think they need a 20% down payment to enter the market, they also tend to think they’ll have to wait several years (in some markets) to come up with the necessary funds to buy their dream homes. The report continues to say,

“The truth: 32% of current U.S. homeowners put 5% or less down on their home, according to census data.” (as shown above).

The lack of knowledge about the home-buying process is unfortunately keeping many motivated buyers on the sidelines.

Bottom Line

Don’t let a lack of understanding keep you and your family out of the housing market. Let’s get together to discuss your options today.

Contact us: PHP Houses 142 W Lakeview Ave Unit 1030 Lake Mary, FL 32746 Ph: (407) 519-0719 Fax: (407) 205-1951 email: info@phphouses.com