Should You Buy a Home with Inflation This High?

Should You Buy a Home with Inflation This High?

While the Federal Reserve is working hard to bring down inflation, the latest data shows the inflation rate is still going up. You no doubt are feeling the pinch on your wallet at the gas pump or the grocery store, but that news may also leave you wondering: should I still buy a home right now?

Greg McBride, Chief Financial Analyst at Bankrate, explains how inflation is affecting the housing market:

“Inflation will have a strong influence on where mortgage rates go in the months ahead. . . . Whenever inflation finally starts to ease, so will mortgage rates — but even then, home prices are still subject to demand and very tight supply.”

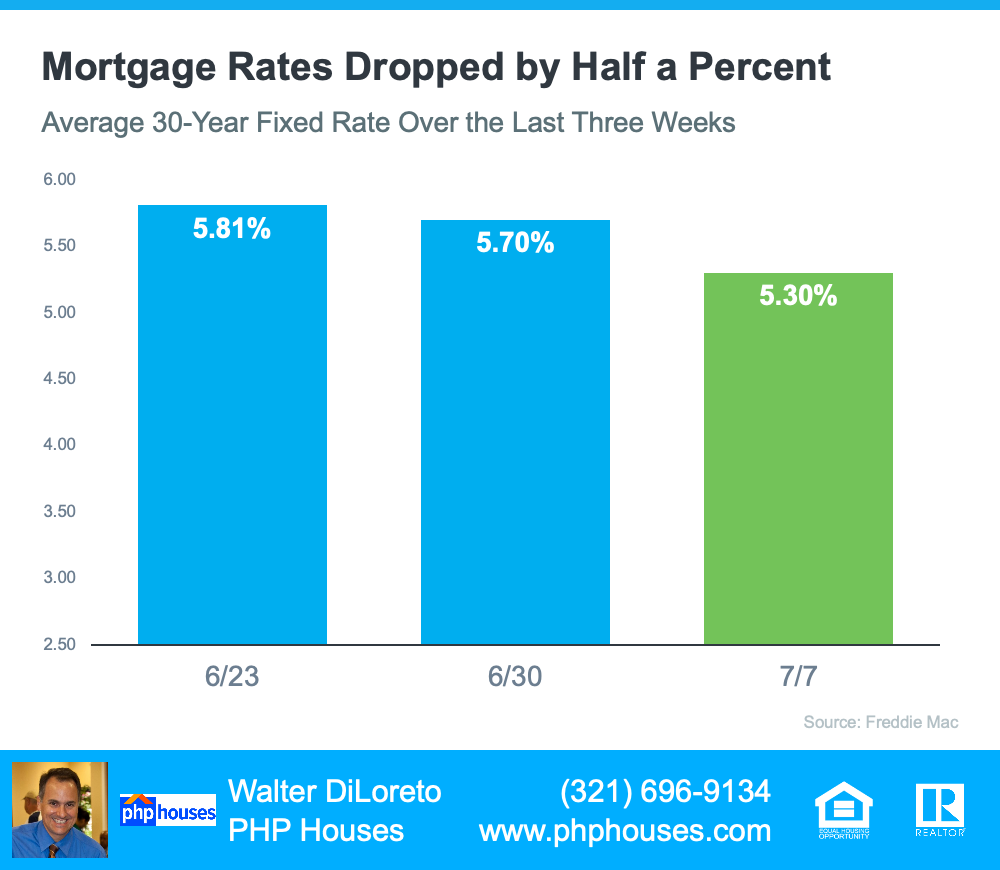

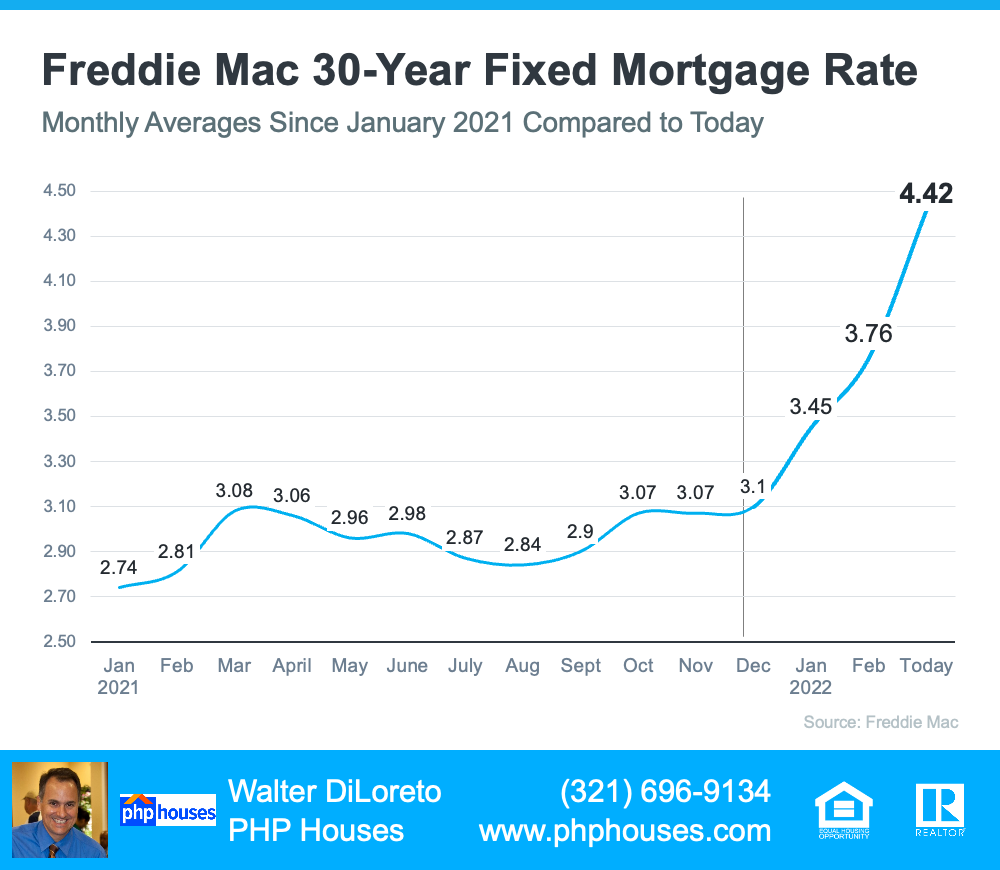

No one knows how long it’ll take to bring down inflation, and that means the future trajectory of mortgage rates is also unclear. While that uncertainty isn’t comfortable, here’s why both inflation and mortgage rates are important for you and your homeownership plans.

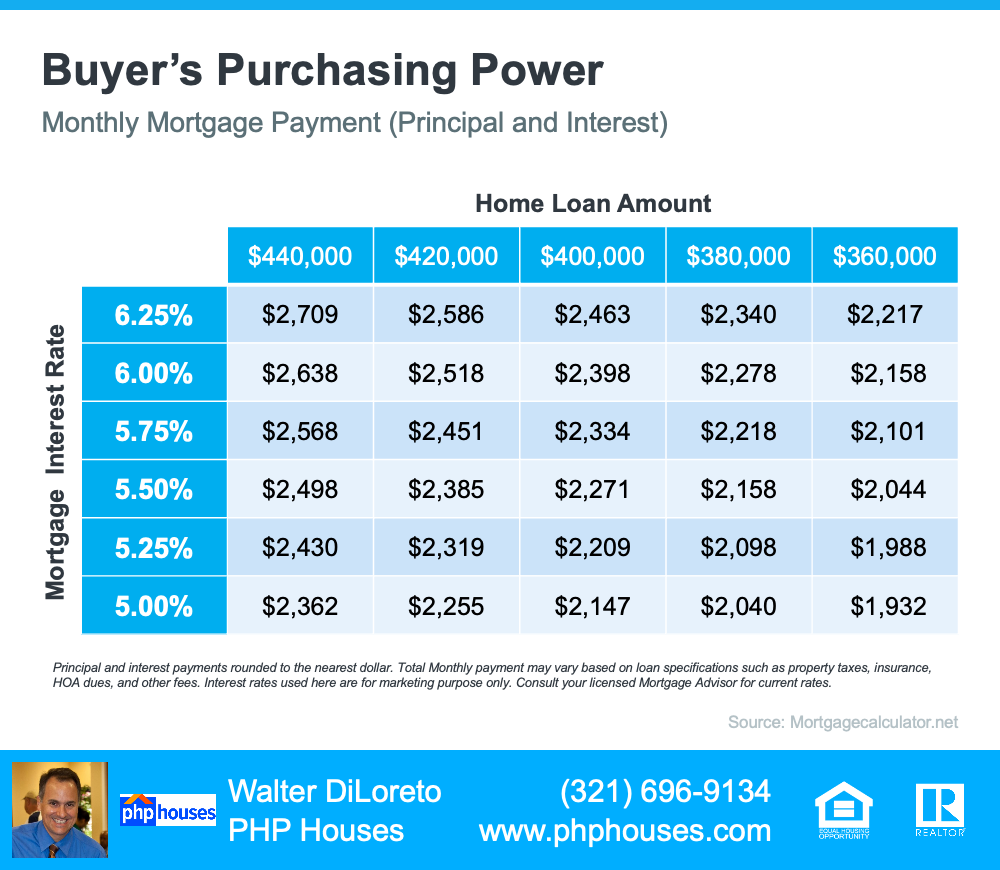

When you buy a home, the mortgage rate and the price of the home matter. Higher mortgage rates impact how much you’ll pay for your monthly mortgage payment – and that directly affects how much you can comfortably afford. And while there’s no denying it’s more expensive to buy and finance a home this year than it was last year, it doesn’t mean you should pause your search. Here’s why.

Homeownership Is Historically a Great Hedge Against Inflation

In an inflationary economy, prices rise across the board. Historically, homeownership is a great hedge against those rising costs because you can lock in what’s likely your largest monthly payment (your mortgage) for the duration of your loan. That helps stabilize some of your monthly expenses. Not to mention, as home pricescontinue to appreciate, your home’s value will too. That’s why Mark Cussen, Financial Writer at Investopedia, says:

“Real estate is one of the time-honored inflation hedges. It’s a tangible asset, and those tend to hold their value when inflation reigns, unlike paper assets. More specifically, as prices rise, so do property values.”

Also, no one is calling for homes to lose value. As Selma Hepp, Deputy Chief Economist at CoreLogic, says:

“The current home price growth rate is unsustainable, and higher mortgage rates coupled with more inventory will lead to slower home price growth but unlikely declines in home prices.”

In a nutshell, your home search doesn’t have to go on hold because of rising inflation or higher mortgage rates. There’s more to consider when it comes to why you want to buy a home. In addition to shielding yourself from the impact of inflation and growing your wealth through ongoing price appreciation, there are other reasons to buy a home right now like addressing your changing needs and so much more.

Bottom Line

Homeownership is one of the best decisions you can make in an inflationary economy. You get the benefit of the added security of owning your home in a time when experts are forecasting prices to continue to rise.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Let’s Connect:

Facebook

Linkedin

Twitter

Instagram

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. The author does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. The author will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.