Over the past year, mortgage rates have fallen more than a full percentage point, hitting a new historic low 15 times. This is a great driver for homeownership, as today’s low rates provide consumers with some significant benefits. Here’s a look at three of them.

1. Move-up or Downsize: One option is to consider moving into a new home, putting the equity you’ve likely gained in your current house toward a down payment on a new one that better meets your needs – something that’s truly a perfect fit, especially if your lifestyle has changed this year.

2. Become a First-Time Homebuyer: There are many financial and non-financial benefits to owning a home, and the most important thing is to first decide when the time is right for you. You have to determine that on your own, but know that now is a great time to buy if you’re considering it. Just take a look at the cost of renting vs. buying.

3. Refinance: If you already own a home, you may decide you’re going to refinance. It’s one way to lock in a lower monthly payment and save more over time. However, it also means paying upfront closing costs, too. If you want to take this route, you have to answer the question: Should I refinance my home?

Why 2020 Was a Great Year for Homeownership

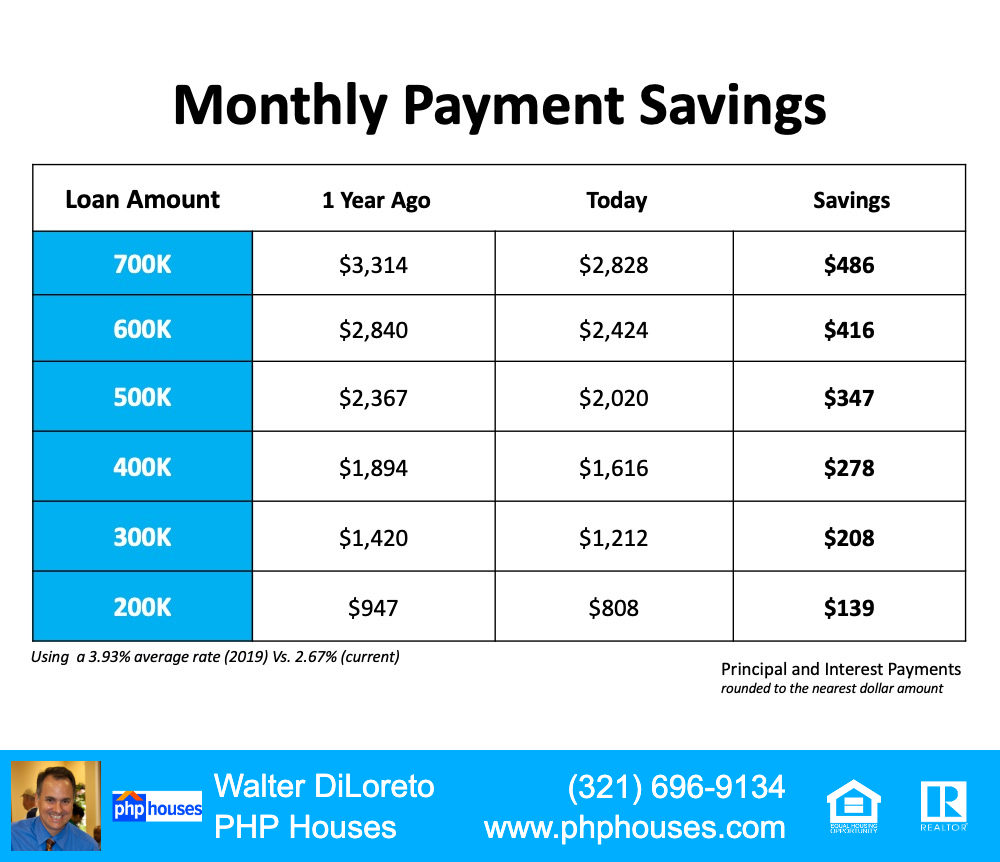

Last year, the average mortgage rate was 3.93% (substantially higher than it is today). If you waited for a better time to make a move, market conditions have improved significantly. Today’s low mortgage rates are a huge perk for buyers, so it’s a great time to get more for your money and consider a new home.

The chart below shows how much you would save per month based on today’s rates compared to what you would have paid if you purchased a home exactly one year ago, depending on how much you finance:

Monthly Payment Savings

Bottom Line

If you’ve been waiting since last year to make your move into homeownership or to find a house that better meets your needs, today’s low mortgage rates may be just what you need to get the process going. Let’s connect today to discuss how you may benefit from the current rates.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Once you’ve found the right home and applied for a mortgage, there are some key things to keep in mind before you close. You’re undoubtedly excited about the opportunity to decorate your new place, but before you make any large purchases, move your money around, or make any major life changes, consult your lender – someone who is qualified to tell you how your financial decisions may impact your home loan.

Below is a list of things you shouldn’t do after applying for a mortgage. They’re all important to know – or simply just good reminders – for the process.

1. Don’t Deposit Cash into Your Bank Accounts Before Speaking with Your Bank or Lender. Lenders need to source your money, and cash is not easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

2. Don’t Make Any Large Purchases Like a New Car or Furniture for Your New Home. New debt comes with new monthly obligations. New obligations create new qualifications. People with new debt have higher debt-to-income ratios. Higher ratios make for riskier loans, and then sometimes qualified borrowers no longer qualify.

3. Don’t Co-Sign Other Loans for Anyone. When you co-sign, you’re obligated. With that obligation comes higher ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

4. Don’t Change Bank Accounts. Remember, lenders need to source and track your assets. That task is significantly easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

5. Don’t Apply for New Credit. It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be impacted. Lower credit scores can determine your interest rate and maybe even your eligibility for approval.

6. Don’t Close Any Credit Accounts. Many buyers believe having less available credit makes them less risky and more likely to be approved. Wrong. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants of your score.

Bottom Line

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. The best plan is to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

Homeowner Equity Increases an Astonishing $1 Trillion

In a year that was financially devastating for many Americans, some good news for most homeowners is the dramatic gain in home equity over the last twelve months. Last week, CoreLogic released its 2020 3rd Quarter Homeowner Equity Insights report, which reveals four major findings:

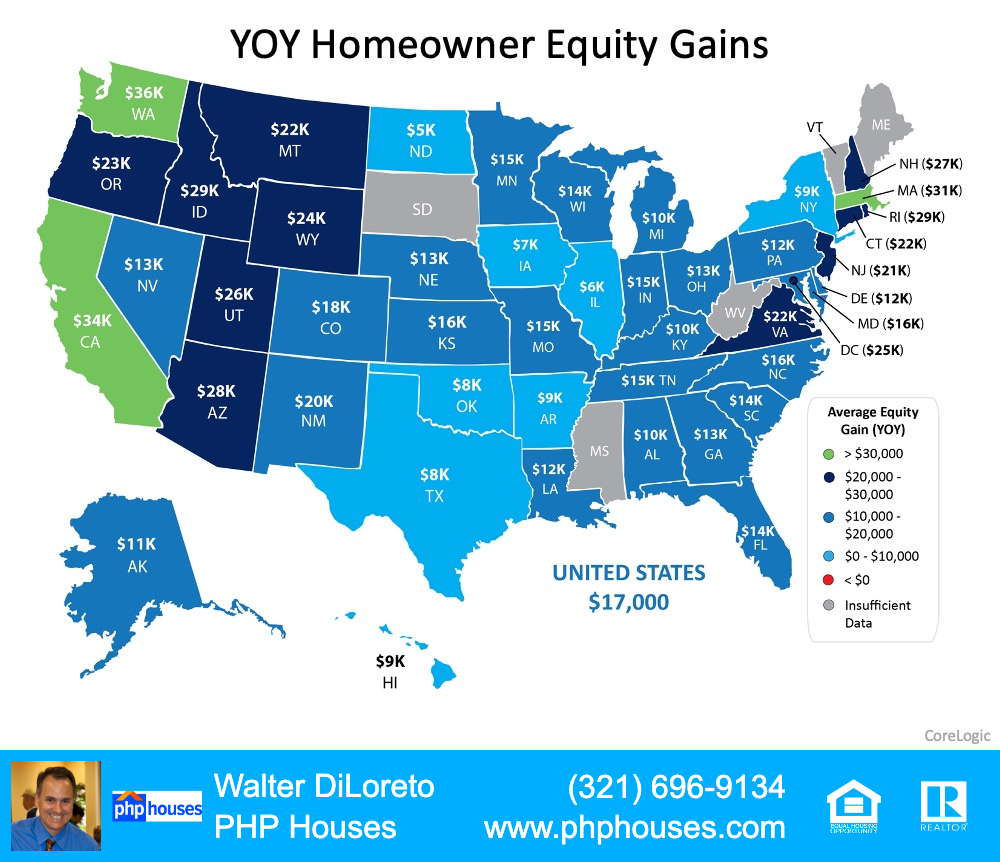

U.S. homeowners with mortgages have seen their equity increase by a total of $1 trillion since the third quarter of 2019.

The average homeowner gained approximately $17,000 in equity over the past year.

This is a 10.8% increase in equity over last year.

The average household with a mortgage now has $194,000 in home equity.

This has given many homeowners the ability to redesign their homes to meet their changing needs. Frank Martell, President and CEO of CoreLogic, explains in the report:

“The housing market has remained a strong pillar in an otherwise tumultuous economic year. A sharp rise in demand, spurred by record-low interest rates, continues to bolster homeowner equity. And with many people now spending more time than ever before at home, some homeowners have tapped into their strengthening equity to fund renovations.”

This build-up in equity also gives more options to homeowners who have been financially impacted by the pandemic. Today, homeowners with substantial equity are in a much better position to work out a deal with their lender if they cannot pay their mortgage. Alternatively, they also have the power to sell and walk away with their equity in the form of cash or as a down payment toward a more affordable house. Frank Nothaft, Chief Economist for CoreLogic, addresses the issue in the report:

“Over the past year, strong home price growth has created a record level of home equity for homeowners…This provides an important buffer to protect families if they experience financial difficulties and is one reason for the generational-low in foreclosure rates reported.”

Here’s a map showing equity gains by state:

YOY Homeowner Equity Gains

This gain in home equity is a blessing for homeowners in these trying times, and it seems that the next two years will continue to reward those who own a home.

Last week, the National Association of Realtors (NAR) held their 2020 Real Estate Forecast Summit. At the summit, they shared the results of a recent survey of 23 economic and housing market experts. The median forecast among the experts called for home values to increase further by 8% in 2021 and 5.5% in 2022.

Bottom Line

In a year that has many of us reevaluating what “home” really means, those who own their homes have been rewarded with a financial windfall that averages $17,000 individually and totals $1 trillion nationally.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

3 Reasons to Be Optimistic about Real Estate in 2021

This year will be remembered for many reasons, and optimism is one thing that’s been in short supply since the spring. We’re experiencing a global pandemic, social unrest, an economic downturn, and natural disasters, just to name a few. The challenges brought on by the health crisis have also forced many homeowners to reevaluate their space and what they need in a home going into 2021. So, experts are forecasting that next year is one in which we can be optimistic about real estate for three key reasons.

1. The Economy Is Expected to Continue Improving

Tim Duy from the University of Oregon puts it this way:

“There is nothing fundamentally ‘broken’ in the economy that needs to heal…there was no obvious financial bubble driving excessive activity in any one economic sector when the pandemic hit…With Covid-19 cases surging again, it is understandably hard to look optimistically to the other side of this winter…Don’t let the near-term challenges distract from the economic stage being set for next four years.”

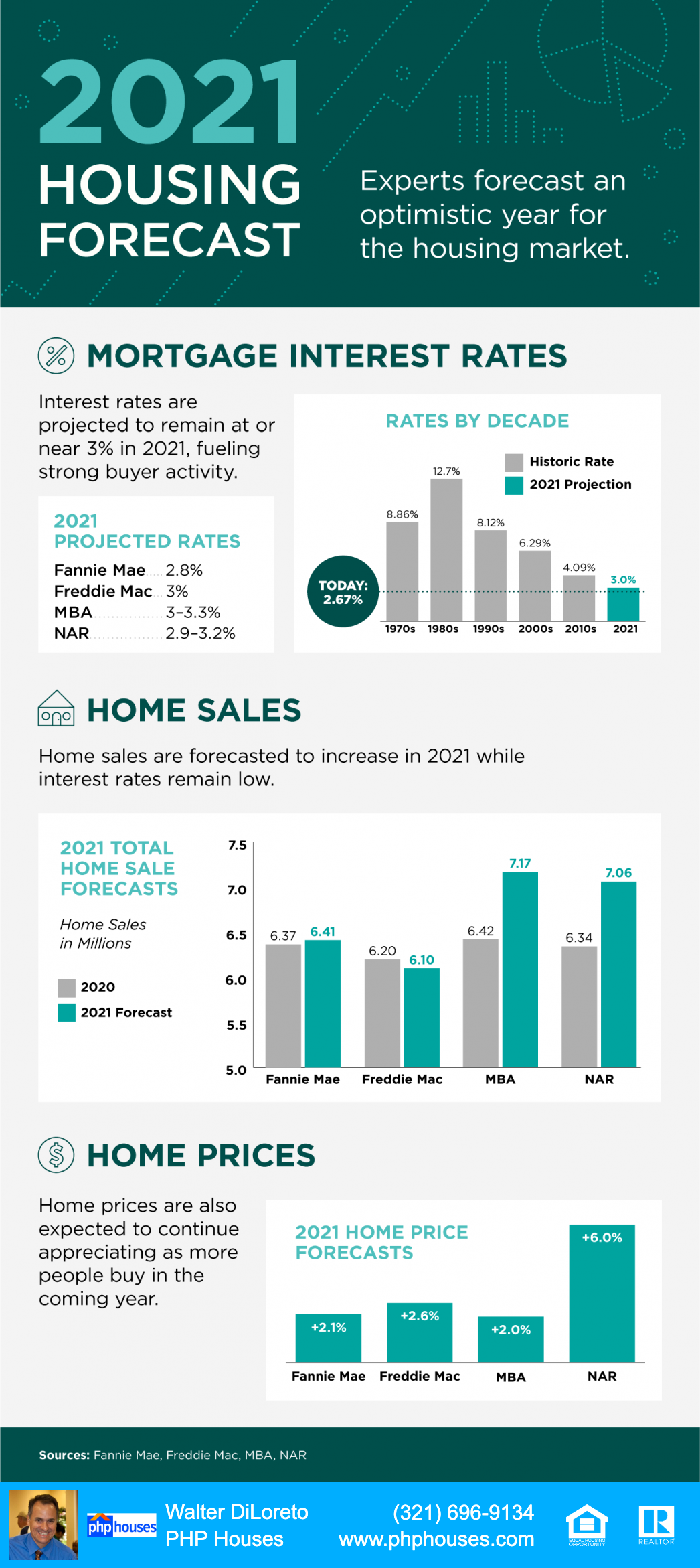

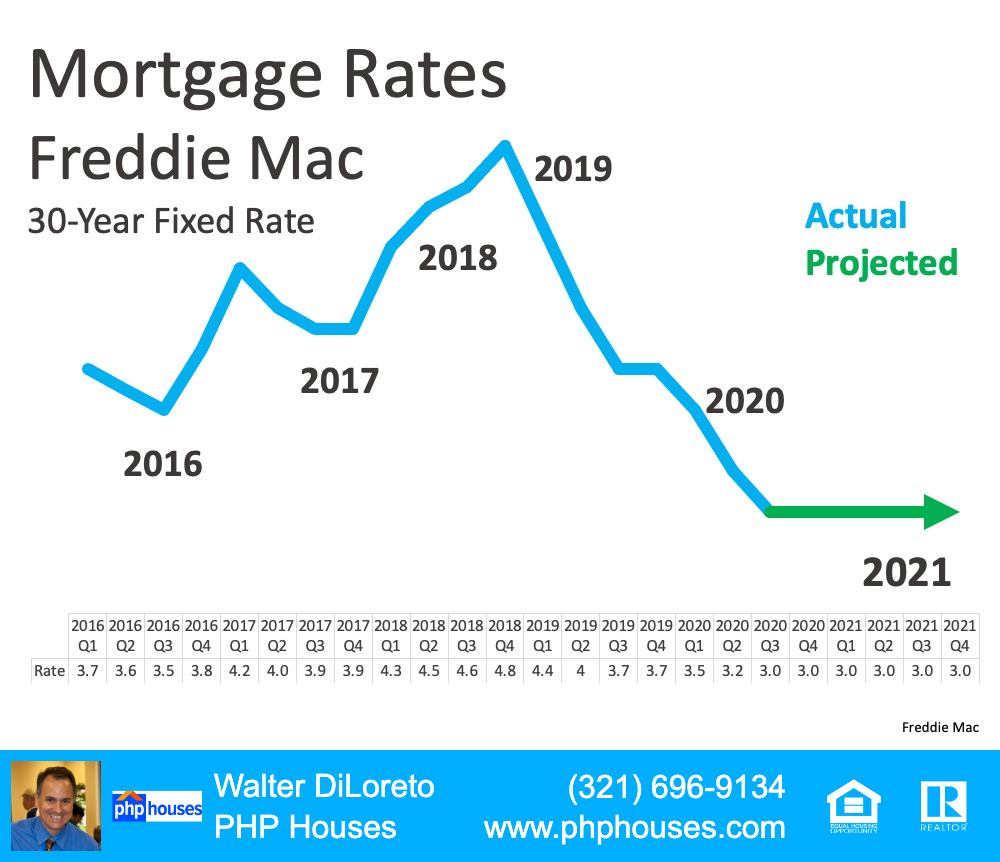

2. Interest Rates Are Projected to Stay Low

In the latest projections from Freddie Mac, interest rates for a 30-year fixed-rate mortgage are expected to remain at or near 3% next year. These low rates will continue to make homes more affordable, driving demand for housing in 2021.

Mortgage Rates Freddie Mac

3. Future Home Sales Are Forecasted to Grow

While the economy improves and interest rates remain low, homes are also expected to continue appreciating as more people buy in the coming year. Danielle Hale, Chief Economist at realtor.com, says:

“We expect home sales in 2021 to come in 7.0% above 2020 levels, following a more normal seasonal trend and building momentum through the spring and sustaining the pace in the second half of the year.”

Bottom Line

Experts forecast that buyers and sellers are going to be active in 2021. If you’ve thought about buying or selling your home this year but have held off, now may be the time to take advantage of this market. Let’s connect to take the first step toward your new home today.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

Black Friday and Cyber Monday are behind us, yet finding the perfect holiday gifts for friends and family is certainly still top of mind for many right now. This year, there’s another type of buyer that’s very active this holiday season – the homebuyer.

Each month, ShowingTime releases their Showing Index which tracks the average number of appointments received on active U.S. house listings. The most recent index notes:

“The Showing Index reported a 60.9 percent jump in nationwide showing traffic year over year in October, the sixth consecutive month to see an increase over last year.”

Here’s the breakdown of the latest activity by region of the country compared to this time last year:

The Northeast increased by 65.5%

The West increased by 64.7%

The Midwest increased by 55.7%

The South increased by 54.7%

Why is the traffic so active?

The health crisis definitely put homebuying plans on pause for many earlier this year. Buyers, however, are in the market and making moves well past the typical busy homebuying seasons of spring and summer.

One of the main reasons buyer traffic has continued to soar in the second half of 2020 is how dramatically mortgage rates have fallen. According to Freddie Mac, the average mortgage rate last December was 3.72%. Today, the rate is a full percentage point lower.

Bottom Line

There are first-time, move-up, and move-down buyers actively looking for the home of their dreams this winter. If you’re thinking of selling your house in 2021, you don’t need to wait until the spring to do it. Your potential buyer is very likely searching for a home in your neighborhood right now.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

If you’re currently feeling the stress of affording your mortgage payment, or if you know someone who is, there’s still time to get help. For homeowners experiencing financial hardship this year, the CARES Act provides mortgage payment deferral options, creating much-needed relief in these challenging times.

It’s important, however, to understand how forbearance works. It’s not automatic. You need to take action now and apply for the program before these options expire.

“Approximately 400,000 homeowners who became delinquent after the pandemic began have forgone forbearance and become delinquent. Theseborrowers may not know they are eligible for forbearance.”

Thankfully, there’s still time to apply for forbearance, even if you’re just learning about it now. Doing so may be the game-changer you need to stay in your home, just when you need it most. Mike Fratantoni, Senior Vice President and Chief Economist at the Mortgage Bankers Association (MBA), explained:

“The increase in new forbearance requests may be the result of additional outreach to homeowners who had previously not taken advantage of forbearance opportunities.”

If you need to apply for forbearance but aren’t sure how to begin the process, the Consumer Financial Protection Bureau (CFPB) published 5 steps to follow when requesting mortgage forbearance:

1. Find the contact information for your servicer

Look at your mortgage statement to find the phone number for your servicer (the company you send your mortgage payment to every month). The Consumer Financial Protection Bureau encourages you to use the number on your statement to avoid scams.

2. Call your servicer

Explain your situation so your servicer can determine your best course of action. Be sure to ask any questions you have about the process.

3. Ask if you’re eligible for protection under the CARES Act

The CARES Act protects homeowners with federally backed loans (FHA, VA, USDA, Fannie Mae, and Freddie Mac). In addition, some private servicers are also providing forbearance programs.

4. Ask what happens when your forbearance period ends

Depending on the plan available to you, there are different options you may be able to consider. Your servicer will help you get a better understanding of what’s available.

The CFPB also recommends asking questions like:

What happens to the payments I miss?

What are my repayment options?

When will repayment be due?

Are there any fees?

5. Ask your servicer to provide the agreement in writing

A written agreement allows you to see exactly what type of program you’re agreeing to. It also helps you make sure it matches what you discuss with your provider over the phone.

Bottom Line

Help is out there for homeowners in need, but it’s important to apply now while this benefit is still available. The Consumer Financial Protection Bureau says: don’t wait, forbearance is not automatic. It must be requested. Reach out to your mortgage provider today so you can get the assistance you need to protect the hard-earned investment you’ve made in your home.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

Why It Makes Sense to Sell Your House This Holiday Season

If you’re one of the many homeowners thinking about taking your house off the market for the holidays, hang on. You definitely don’t want to miss the great selling opportunity you have right now. Here’s why this month is the optimal time to make sure your house is available for holiday buyers.

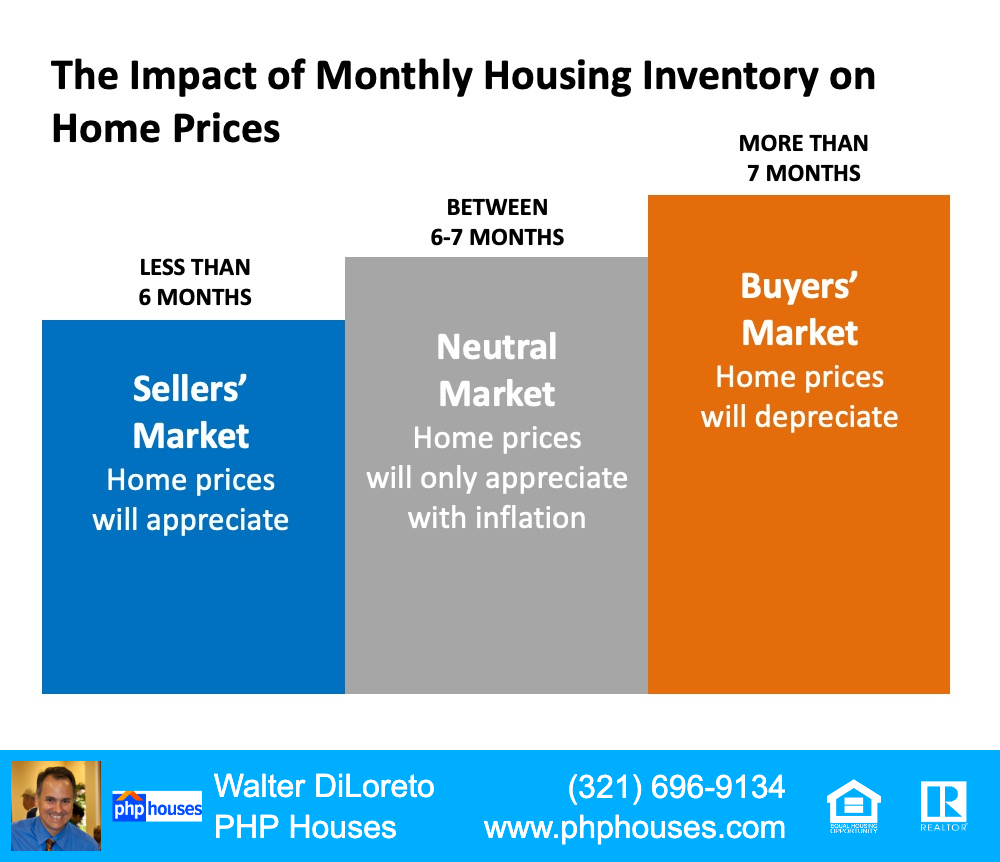

The latest Existing Home Sales Report from The National Association of Realtors (NAR) shows the inventory of houses for sale has dropped to an astonishing all-time low. It now sits at a 2.5-month supply at the current sales pace.

Historically, a 6-month supply is necessary for a ‘normal’ or ‘neutral’ market, in which there are enough homes available for active buyers (See graph below):

The Impact of Monthly Housing Inventory on Home Prices

When the supply of houses for sale is as low as it is today, it’s much harder for buyers to find homes to purchase. This means competition among purchasers rises and more bidding wars take place, making it essential for buyers to submit very attractive offers.

As this happens, prices rise and sellers are in the best position to negotiate deals that meet their ideal terms. So, if your neighbors decide to remove their listings this season, your house may quickly rise to the top of a holiday buyer’s wish list if you stay on the market.

Today, there are many buyers who are ready, willing, and able to purchase. Record-low mortgage rates and a year filled with unique changes have prompted buyers to think differently about where they live and to take action. The supply of homes for sale is not keeping up with this high demand, making now the optimal time to sell your house.

Bottom Line

Home prices are appreciating in today’s sellers’ market. Making your home available over the next few weeks will give you the most exposure to buyers who will be actively competing against each other to purchase

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.

Talk of a housing bubble is beginning to crop up as home prices have appreciated at a rapid pace this year. This is understandable since the appreciation of residential real estate is well above historic annual averages. According to the Federal Housing Finance Agency (FHFA), annual appreciation since 1991 has averaged 3.8%. Here are the latest 2020 appreciation numbers from three reliable sources:

It’s easy to jump to the conclusion that house appreciation is out of control in today’s market. However, we need to put these numbers into context first.

Inflation and the Comeback from the Housing Crash

Following the housing crash, home values depreciated dramatically from 2007-2011. Values are still recovering from that unusually long period of falling prices. We must also realize that normal inflation has had an impact.

Bill McBride, the founder of the well-respected Calculated Risk blog, recently summed it up this way:

“It has been over fourteen years since the bubble peak. In the Case-Shiller release today, the seasonally adjusted National Index, was reported as being 22.2% above the previous bubble peak. However, in real terms (adjusted for inflation), the National index is still about 2% below the bubble peak…As an example, if a house price was $200,000 in January 2000, the price would be close to $291,000 today adjusted for inflation.”

The COVID Impact on Home Prices

The pandemic caused many households to reconsider whether their current home still fulfills their lifestyle. Many homeowners now want larger yards that are both separate and private.

Their needs on the inside of the home have changed too. People now want home offices, gyms, and living rooms well-suited for video conferencing. Barbara Ballinger, a freelance writer and the author of several books on real estate, recently wrote:

“While homeowners continue to want their outdoor spaces that offer a safe retreat, that appeal has shifted into other parts of the home, coupling comfort with function. In other words, homeowners want amenities for work and leisure, and they plan to enjoy them long after the pandemic.”

At the same time, concerns about the pandemic have caused many homeowners to put their plans to sell on hold. Realtor.com just released their November Monthly Housing Market Trends Report. It explains:

“Nationally, the inventory of homes for sale decreased 39.2% over the past year in November…This amounted to 490,000 fewer homes for sale compared to November of last year.”

More people buying and fewer people selling has caused home prices to escalate. However, with a vaccine on the horizon, more homeowners will be putting their houses on the market. This will better balance supply with demand and slow down the rapid appreciation.

That’s why major organizations in the housing industry are calling for much more moderate home appreciation next year. Here are the most recent forecasts for 2021:

Finally, let’s put to rest some of the concerns that today’s scenario is anything like what led up to the last housing crash. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why this is nothing like 2006:

“Such a frenzy of activity, reminiscent of 2006, raises questions about a bubble and the potential for a painful crash. The answer: There’s no comparison. Back in 2006, dubious adjustable-rate mortgages taxed many buyers’ budgets. Some loans didn’t even require income documentation. Today, buyers are taking out 30-year fixed-rate mortgages. Fourteen years ago, there were 3.8 million homes listed for sale, and home builders were putting up about 2 million new units. Now, inventory is only about 1.5 million homes, and home builders are underproducing relative to historical averages.”

Bottom Line

Most aspects of life have been anything but normal in 2020. That includes buying and selling real estate. High demand coupled with restricted supply has caused home prices to appreciate above historic levels. With the end of the health crisis in sight, we will see price appreciation return to more normal levels next year.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

THE INFORMATION PRESENTED IN THIS ARTICLE IS FOR EDUCATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED LEGAL, FINANCIAL, OR AS ANY OTHER TYPE OF ADVICE.