In times of uncertainty, one of the best things we can do to ease our fears is to educate ourselves with research, facts, and data. Digging into past experiences by reviewing historical trends and understanding the peaks and valleys of what’s come before us is one of the many ways we can confidently evaluate any situation. With concerns of a global recession on everyone’s minds today, it’s important to take an objective look at what has transpired over the years and how the housing market has successfully weathered these storms.

1. The Market Today Is Vastly Different from 2008

We all remember 2008. This is not 2008. Today’s market conditions are far from the time when housing was a key factor that triggered a recession. From easy-to-access mortgages to skyrocketing home price appreciation, a surplus of inventory, excessive equity-tapping, and more – we’re not where we were 12 years ago. None of those factors are in play today. Rest assured, housing is not a catalyst that could spiral us back to that time or place.

According to Danielle Hale, Chief Economist at Realtor.com, if there is a recession:

“It will be different than the Great Recession. Things unraveled pretty quickly, and then the recovery was pretty slow. I would expect this to be milder. There’s no dysfunction in the banking system, we don’t have many households who are overleveraged with their mortgage payments and are potentially in trouble.”

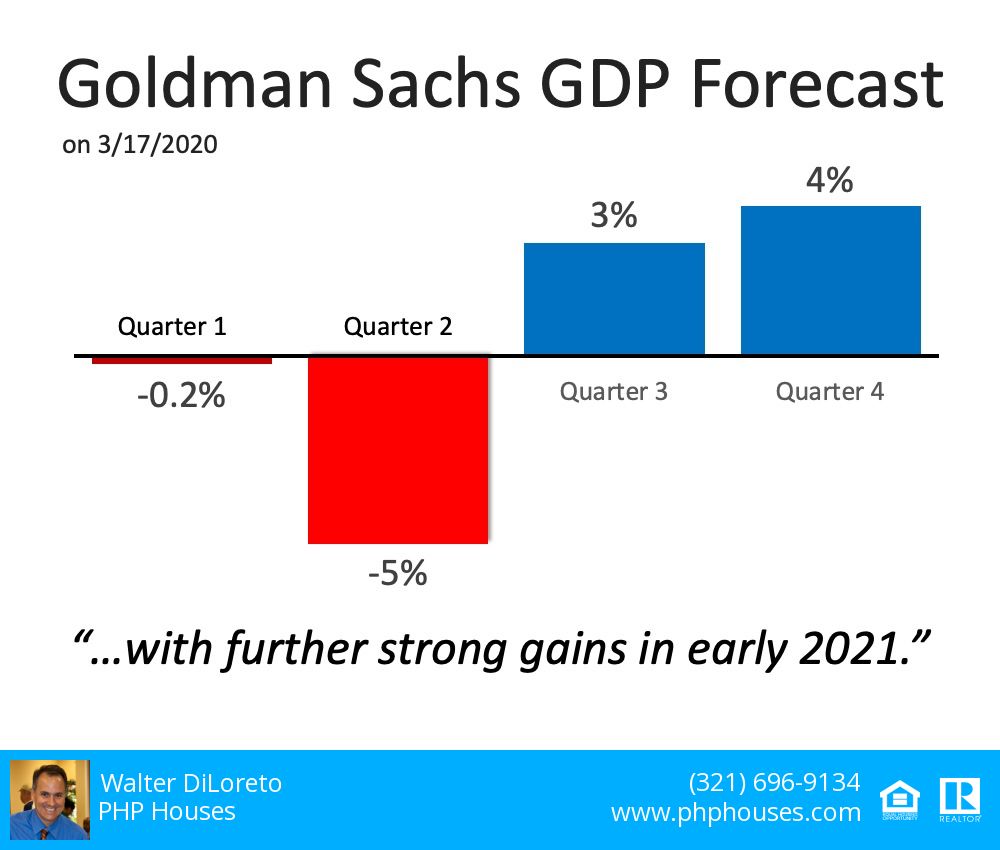

In addition, the Goldman Sachs GDP Forecast released this week indicates that although there is no growth anticipated immediately, gains are forecasted heading into the second half of this year and getting even stronger in early 2021.

Both of these expert sources indicate this is a momentary event in time, not a collapse of the financial industry. It is a drop that will rebound quickly, a stark difference to the crash of 2008 that failed to get back to a sense of normal for almost four years. Although it poses plenty of near-term financial challenges, a potential recession this year is not a repeat of the long-term housing market crash we remember all too well.

2. A Recession Does Not Equal a Housing Crisis

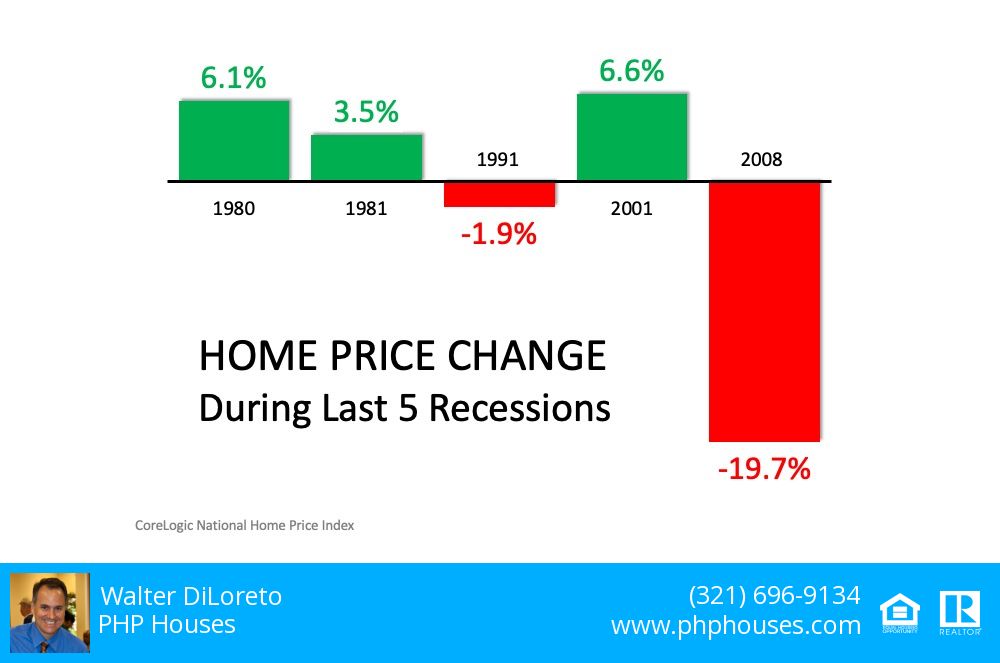

Next, take a look at the past five recessions in U.S. history. Home values actually appreciated in three of them. It is true that they sank by almost 20% during the last recession, but as we’ve identified above, 2008 presented different circumstances. In the four previous recessions, home values depreciated only once (by less than 2%). In the other three, residential real estate values increased by 3.5%, 6.1%, and 6.6% (see below):

3. We Can Be Confident About What We Know

Concerns about the global impact COVID-19 will have on the economy are real. And they’re scary, as the health and wellness of our friends, families, and loved ones are high on everyone’s emotional radar.

According to Bloomberg,

“Several economists made clear that the extent of the economic wreckage will depend on factors such as how long the virus lasts, whether governments will loosen fiscal policy enough and can markets avoid freezing up.”

That said, we can be confident that, while we don’t know the exact impact the virus will have on the housing market, we do know that housing isn’t the driver.

The reasons we move – marriage, children, job changes, retirement, etc. – are steadfast parts of life. As noted in a recent piece in the New York Times, “Everyone needs someplace to live.” That won’t change.

Bottom Line

Concerns about a recession are real, but housing isn’t the driver. If you have questions about what it means for your family’s homebuying or selling plans, let’s connect to discuss your needs.

Contact us:

PHP Houses

142 W Lakeview Ave

Unit 1030

Lake Mary, FL 32746

Ph: (407) 519-0719

Fax: (407) 205-1951

email: info@phphouses.com

Seeking the help of third-parties is another way how to stop foreclosure in FL. Although homeowners have several options when stopping foreclosure, sometimes the process is too much for a single person. Enlisting the expertise of professionals will lessen your stress while providing a multitude of options for keeping your home. One option available to borrowers is contacting a foreclosure avoidance counselor. The

Seeking the help of third-parties is another way how to stop foreclosure in FL. Although homeowners have several options when stopping foreclosure, sometimes the process is too much for a single person. Enlisting the expertise of professionals will lessen your stress while providing a multitude of options for keeping your home. One option available to borrowers is contacting a foreclosure avoidance counselor. The  Many homeowners find themselves at risk for foreclosure after accruing a large amount of debt. They might think filing for bankruptcy is the simplest solution to escape their financial troubles. In some instances and with enormous debts, that can be true. However, if a homeowner isn’t keen on a lengthy litigation process and wants to halt the foreclosure process immediately, filing for bankruptcy might not be the best strategy for how to stop foreclosure in FL. Once an individual files the petition for bankruptcy, federal law prohibits debt collectors from seizing assets to pay off what’s owed. Since foreclosure is considered a collection activity, mortgage lenders must halt the foreclosure process. Once in court though, the bankruptcy trustee’s role is to play mediator between the filer and creditors, not absolve debt. Going through the courts will buy borrowers time to make past mortgage payments, but it won’t stop the foreclosure process completely. Filing for bankruptcy also has

Many homeowners find themselves at risk for foreclosure after accruing a large amount of debt. They might think filing for bankruptcy is the simplest solution to escape their financial troubles. In some instances and with enormous debts, that can be true. However, if a homeowner isn’t keen on a lengthy litigation process and wants to halt the foreclosure process immediately, filing for bankruptcy might not be the best strategy for how to stop foreclosure in FL. Once an individual files the petition for bankruptcy, federal law prohibits debt collectors from seizing assets to pay off what’s owed. Since foreclosure is considered a collection activity, mortgage lenders must halt the foreclosure process. Once in court though, the bankruptcy trustee’s role is to play mediator between the filer and creditors, not absolve debt. Going through the courts will buy borrowers time to make past mortgage payments, but it won’t stop the foreclosure process completely. Filing for bankruptcy also has  Although homeowners have several methods available to saving their property from repossession, some options are better than others.

Although homeowners have several methods available to saving their property from repossession, some options are better than others.